What is business insurance — and why can't you ignore it?

The reason it matters is not abstract. According to the Association of British Insurers (ABI), over one in five UK SMEs has faced a liability claim. The average cost of defending a commercial liability claim — before any compensation is paid — exceeded £13,500 in 2023. For a business with fewer than ten employees, that figure alone can represent a meaningful proportion of annual profit.

The critical point most guidance misses: underinsurance is as dangerous as no insurance. Research published by Zurich Insurance found that 86% of UK SMEs carry insufficient insurance for their actual risk exposure. A policy that caps out before covering your full liability leaves the remainder as a personal debt.

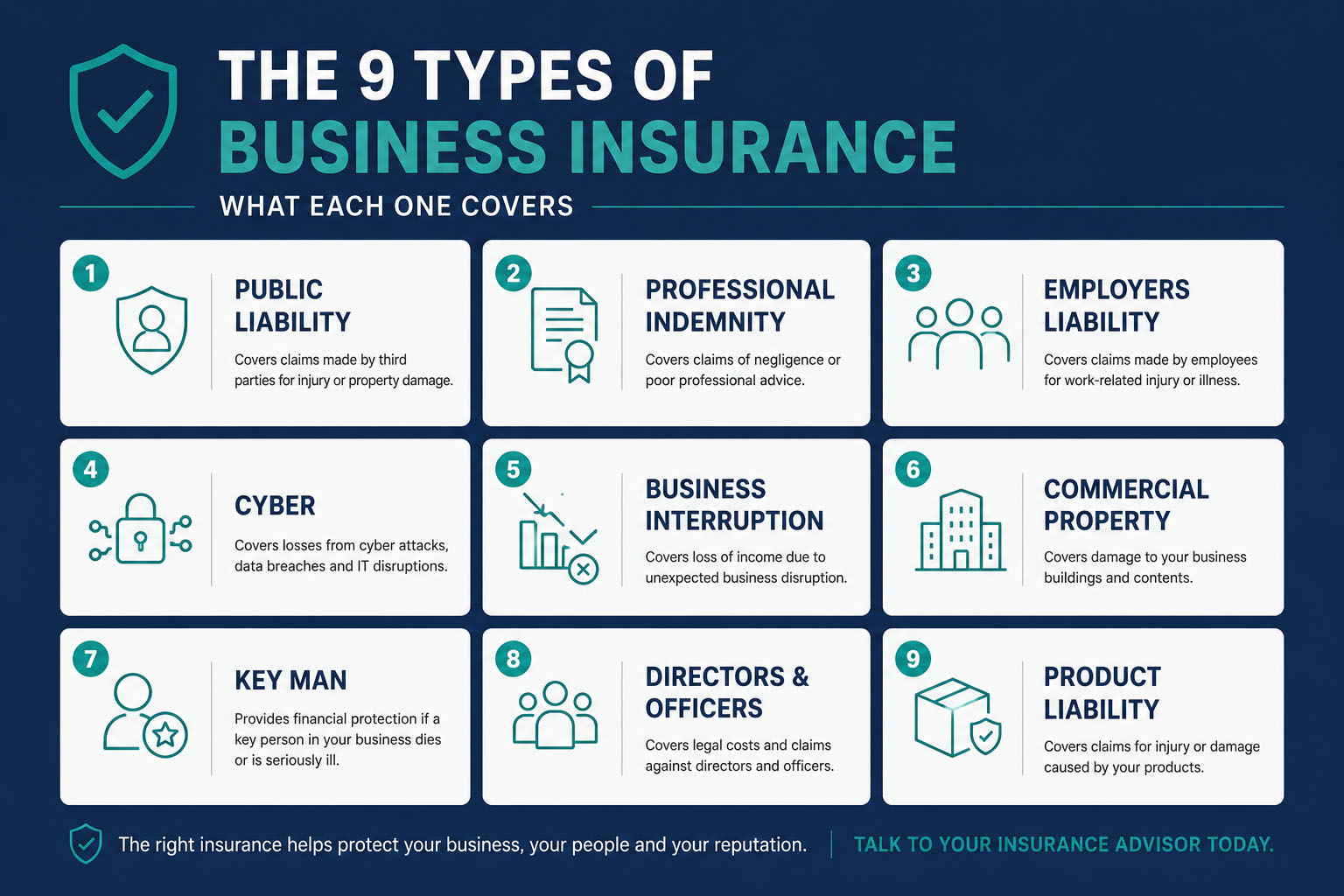

The 9 types of business insurance — what each one covers

Not every business needs every type of cover. The infographic below maps the nine core types of business insurance to the specific risk each one addresses.

Public Liability Insurance

Public liability insurance covers claims made against your business by third parties — customers, clients, members of the public, or anyone your business interacts with — who suffer injury or property damage because of your activities.

What it does not cover: claims by your own employees (that is employers liability), damage to your own property, or professional negligence claims (that is professional indemnity). It covers physical harm and property damage caused to others.

Typical cost: £60–£600 per year for most small businesses. Sole traders in professional services typically pay £60–£120. Higher-risk businesses — tradespeople, event companies, businesses with physical premises — pay £150–£600.

Professional Indemnity Insurance

Professional indemnity insurance protects you against claims that your advice, service, or work caused a client financial loss. It covers the legal costs of defending the claim and any compensation awarded — even if the claim against you is unfounded.

Why this matters for service businesses: Even a claim you win costs money to defend. A groundless claim against a consultant can cost £15,000–£40,000 in legal fees before it is dismissed. Without PI insurance, those costs come directly from your business.

Key distinction: Professional indemnity covers financial loss from your professional services. Public liability covers physical harm or property damage. A business that provides professional services and also visits client premises needs both.

Required by regulation for: solicitors (SRA), financial advisers (FCA), architects (ARB), chartered accountants (ICAEW/ACCA). Required by contract for most government and NHS work.

Employers Liability Insurance — the one that is legally mandatory

Employers liability insurance is the only business insurance that UK law requires by default. The Employers Liability (Compulsory Insurance) Act 1969 mandates that every business with one or more employees must hold a minimum of £5m of employers liability insurance.

The penalty for non-compliance is £2,500 per day while you operate without valid cover. The Health and Safety Executive (HSE) can issue this fine without a claim ever being made — simply for failing to hold the required policy.

Who is exempt: Businesses with no employees at all (sole traders with no staff), and companies where all shares are owned by one person who is also the only employee. Family businesses where all employees are close relatives of the owner may also be exempt — but verify this with your insurer.

Cyber Insurance

Cyber insurance covers the financial consequences of a cyberattack, data breach, or IT system failure. According to Hiscox's Cyber Readiness Report 2024, the average cost of a cyber incident for a UK SME was £8,460 — and that figure excludes the reputational damage and lost business that follows a publicised breach.

What cyber insurance covers:

- Incident response costs: forensic investigation, notification of affected customers (legally required under UK GDPR within 72 hours of a qualifying breach)

- Legal costs associated with regulatory action from the ICO

- Business interruption losses while systems are restored

- Ransom payment costs in ransomware attacks (subject to sub-limits — see below)

Business Interruption Insurance

Business interruption insurance covers the revenue your business loses when it cannot trade — and the fixed costs (rent, salaries, loan repayments) that continue even when trading stops.

The trigger for most business interruption policies is physical damage to your premises — a fire, flood, or structural damage that closes the business. Standard policies do not cover loss of income from a pandemic, loss of a key client, or supply chain failure unless these are explicitly included.

The post-COVID lesson: During 2020–2021, many businesses discovered that their business interruption policies excluded pandemic-related closure. The FCA's test case ruling in January 2021 found in favour of policyholders on several policy wordings — but the outcome varied by insurer and policy wording. Always read the specific trigger conditions in your policy document.

What to check: Does your policy require physical damage to your premises as a trigger, or does it include non-damage triggers (disease, denial of access, loss of utilities)? Non-damage BI cover costs more but provides meaningfully broader protection.

Which business insurance is legally required in the UK?

Only one type of business insurance is universally legally required in the UK: employers liability insurance, under the Employers Liability (Compulsory Insurance) Act 1969.

Beyond that, specific industries and regulated professions have their own mandatory requirements:

| Profession / Sector | Required Insurance | Regulator |

|---|---|---|

| Solicitors | Professional Indemnity | Solicitors Regulation Authority (SRA) |

| Financial Advisers | Professional Indemnity | Financial Conduct Authority (FCA) |

| Architects | Professional Indemnity | Architects Registration Board (ARB) |

| Chartered Accountants | Professional Indemnity | ICAEW / ACCA / ICAS |

| Motor trade businesses | Motor trade liability | Road Traffic Act 1988 |

| Aviation businesses | Aviation liability | Civil Aviation Authority |

| Taxi and private hire | Motor insurance | Local authority / DVLA |

Contractually required vs legally required: Even when not mandated by law, many types of business insurance are functionally required because they are demanded by:

- Government contracts: Typically require £5–10m public liability and professional indemnity appropriate to the contract value

- NHS and public sector contracts: Typically require £5m public liability

- Commercial tenancy agreements: Landlords commonly require buildings insurance and public liability as lease conditions

- Industry body membership: Many trade associations (e.g. CHAS, SafeContractor, Constructionline) require current insurance certificates as membership conditions

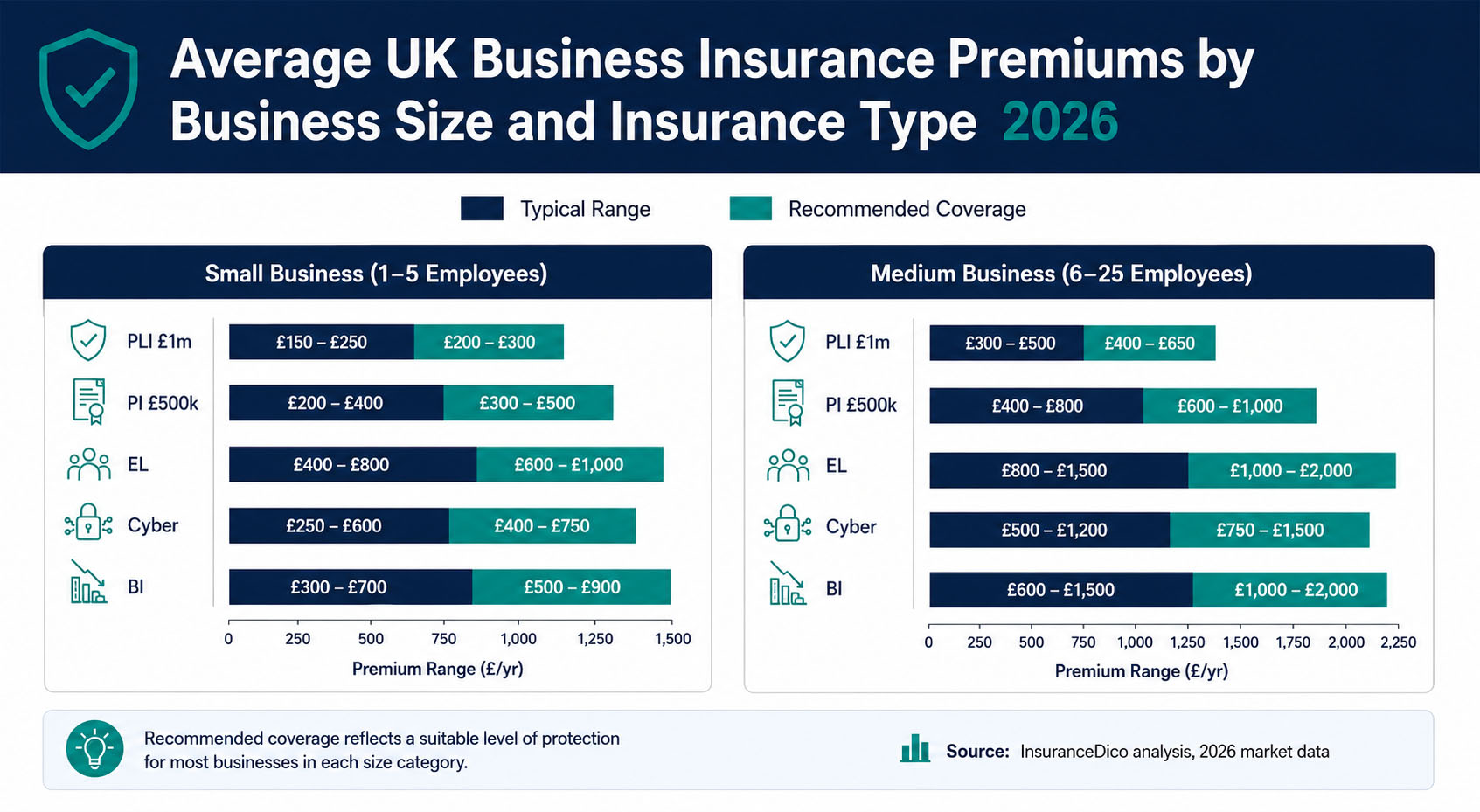

How much does business insurance cost? (2026 data)

Business insurance premiums depend on your business type, turnover, claims history, number of employees, and the specific coverage limits you select. The infographic below shows typical 2026 UK market ranges for the most common policy types, by business size.

How to reduce your business insurance cost

- Bundle policies. Combining public liability, professional indemnity, and employers liability in a single package policy typically saves 15–25% versus purchasing separately. Most major UK business insurers offer combined SME packages.

- Increase your voluntary excess. Raising your excess from £500 to £1,000 typically reduces premiums by 10–20%. Only increase your excess to a level your business can realistically absorb from cash flow.

- Review your declared turnover annually. Premiums are partly turnover-based. If your business is in a lower-revenue phase, ensure your declared turnover reflects the current position — not a previous high.

- Maintain a claims-free record. A 5-year claims-free history earns no-claims discounts at most insurers. Avoid making small claims that erode this record.

- Improve your security and risk management posture. For cyber insurance, documented use of multi-factor authentication, employee security training, and regular backups can reduce premiums by 10–30%.

The most costly business insurance mistakes — with the data to back them up

Mistake 1: Buying the cheapest public liability policy available

The cheapest public liability policies in the UK market — often priced below £50 per year — routinely carry exclusions that make them unable to pay the claims most businesses actually face. Common exclusions in budget PLI policies include: work at heights above three metres, claims involving subcontractors not named on the policy, water or flood damage caused during your work, and electrical installation work.

A policy that excludes the activities your business regularly undertakes provides no meaningful protection. The correct approach is to match the policy to your actual activities, then compare prices within that specification.

Mistake 2: Failing to update your policy as your business grows

An employer with 2 staff who grows to 12 staff is 600% more exposed on their employers liability — but many businesses forget to notify their insurer of headcount changes until renewal. Significant changes that must be notified to your insurer mid-policy include: material increase in employee numbers, expansion into new business activities not covered by your original policy wording, movement into new premises, and any personal injury claim or incident that could give rise to a claim.

Failure to notify material changes can allow an insurer to void a policy or reduce a claim settlement at the point of claim.

Mistake 3: Conflating public liability with employers liability

These are distinct policies covering different risks. Public liability covers claims from people outside your business. Employers liability covers claims from your own employees. Having one does not provide the other. The legal requirement (employers liability for any business with staff) is frequently confused with the contractually required product (public liability). Both are needed.

Mistake 4: Underinsuring professional indemnity

Many professionals set their professional indemnity limit based on what they can afford rather than what their clients are exposed to. The correct measure is the maximum financial loss your work could cause a client. A management consultant working on a £2m transformation project who holds only £250k of PI cover has created a personal financial liability gap of £1.75m in a worst-case scenario.

How to choose the right business insurance: a practical framework

Choosing business insurance is a risk identification exercise before it is a purchasing exercise. Before approaching any insurer or broker:

Step 1 — Identify your legal obligations. Start with what is compulsory: employers liability if you have staff, and any sector-specific mandatory requirements (see table above).

Step 2 — Map your contractual requirements. Review your current client contracts and any frameworks you want to work on. List the insurance types and minimum coverage limits each requires.

Step 3 — Assess your third-party liability exposure. Consider: do you or your staff visit client premises? Do clients visit yours? Do you give advice or provide professional services? Do you manufacture, import, or sell physical products? Each "yes" points to a specific coverage need.

Step 4 — Assess your own asset and income exposure. What business assets would be costly to replace? (Commercial property.) How long could your business survive without trading revenue? (Business interruption.) Who in the business is irreplaceable? (Key man insurance.)

Step 5 — Use a broker for complex needs. Comparison aggregators work well for straightforward public liability and package policies. For professional indemnity, cyber, D&O, or any policy where your business activities are atypical, a specialist commercial insurance broker (BIBA member) will access markets that aggregators do not reach and negotiate policy wording appropriate to your risk.