Trade credit insurance protects businesses against the risk of customers failing to pay their invoices. It covers two scenarios: buyer insolvency (formal insolvency proceedings during the credit period) and protracted default (non-payment within a defined extended period — typically six months after the invoice due date). The three global market leaders are Allianz Trade (formerly Euler Hermes), Atradius, and Coface. Premiums typically run at 0.1%–0.5% of insured turnover. Beyond indemnity, trade credit insurers actively monitor buyer creditworthiness and provide early warning of customers showing financial stress.

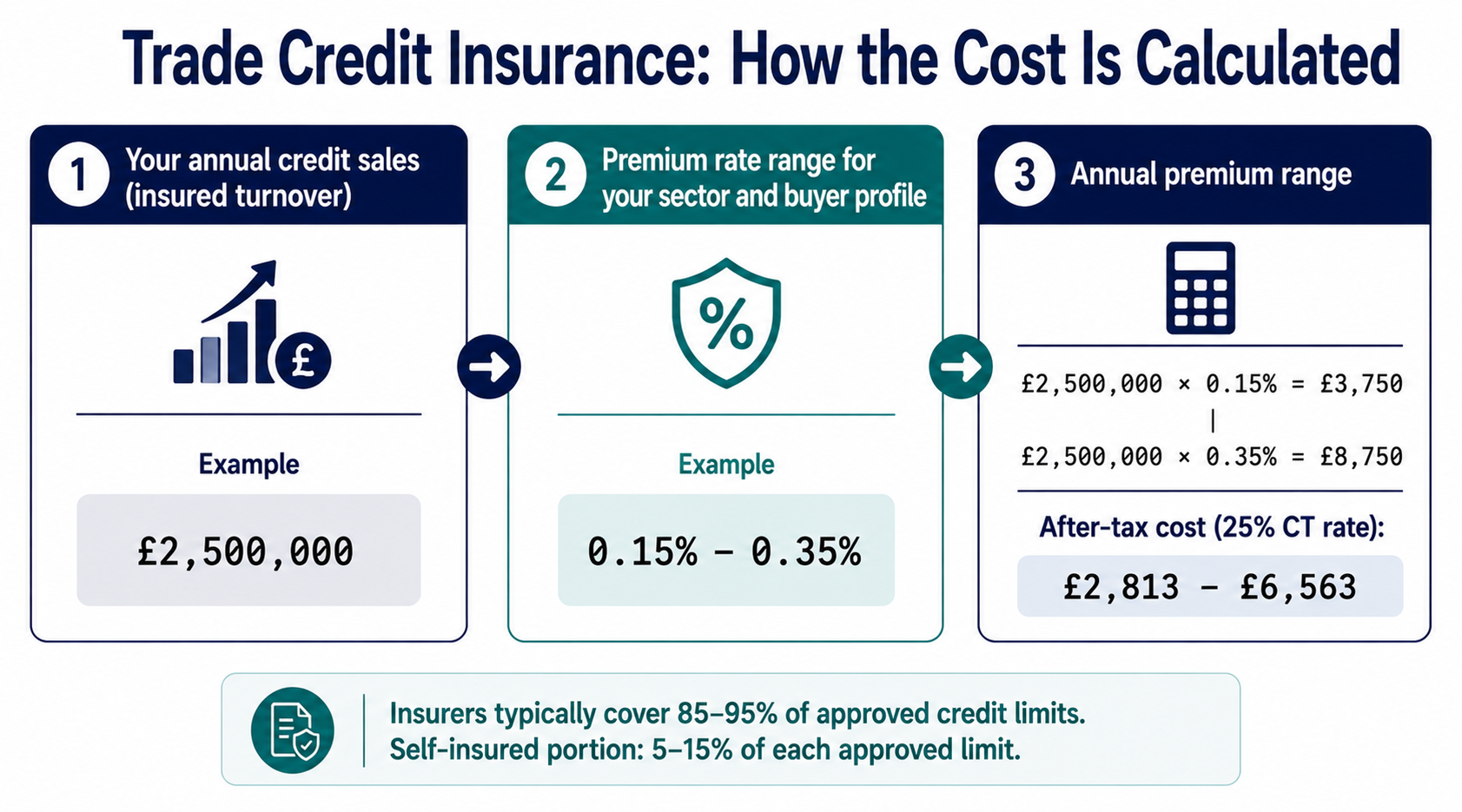

Trade credit insurance is a UK business protection product that indemnifies a seller for the value of unpaid trade receivables when an approved buyer becomes insolvent or fails to pay within a defined protracted default period, paying typically 85–95% of the approved credit limit for that buyer.

The Bad Debt Problem — Why Trade Credit Insurance Exists

UK businesses write off an estimated £1.8bn in bad debts annually according to the Credit Management Research Centre. The average SME carries trade receivables representing 45–60 days of turnover — for a business with £2m annual revenue, that is £240,000–£330,000 of outstanding invoices at any given moment. If a significant customer fails, the impact falls directly on the creditor's balance sheet.

The financial consequences of an uninsured bad debt loss are asymmetric and severe. Consider a business operating at a 10% net profit margin that writes off £50,000 in bad debt from a customer insolvency. To recover that loss through additional sales, the business must generate £500,000 of new turnover at the same margin — the bad debt wipes out the equivalent of five months of profit contribution. For businesses with thinner margins, the ratio is worse.

Trade credit insurance does not eliminate bad debt risk — buyers still fail, and invoices still go unpaid. What it does is transfer the financial consequence of those failures from the creditor's income statement to the insurer.

What Trade Credit Insurance Covers

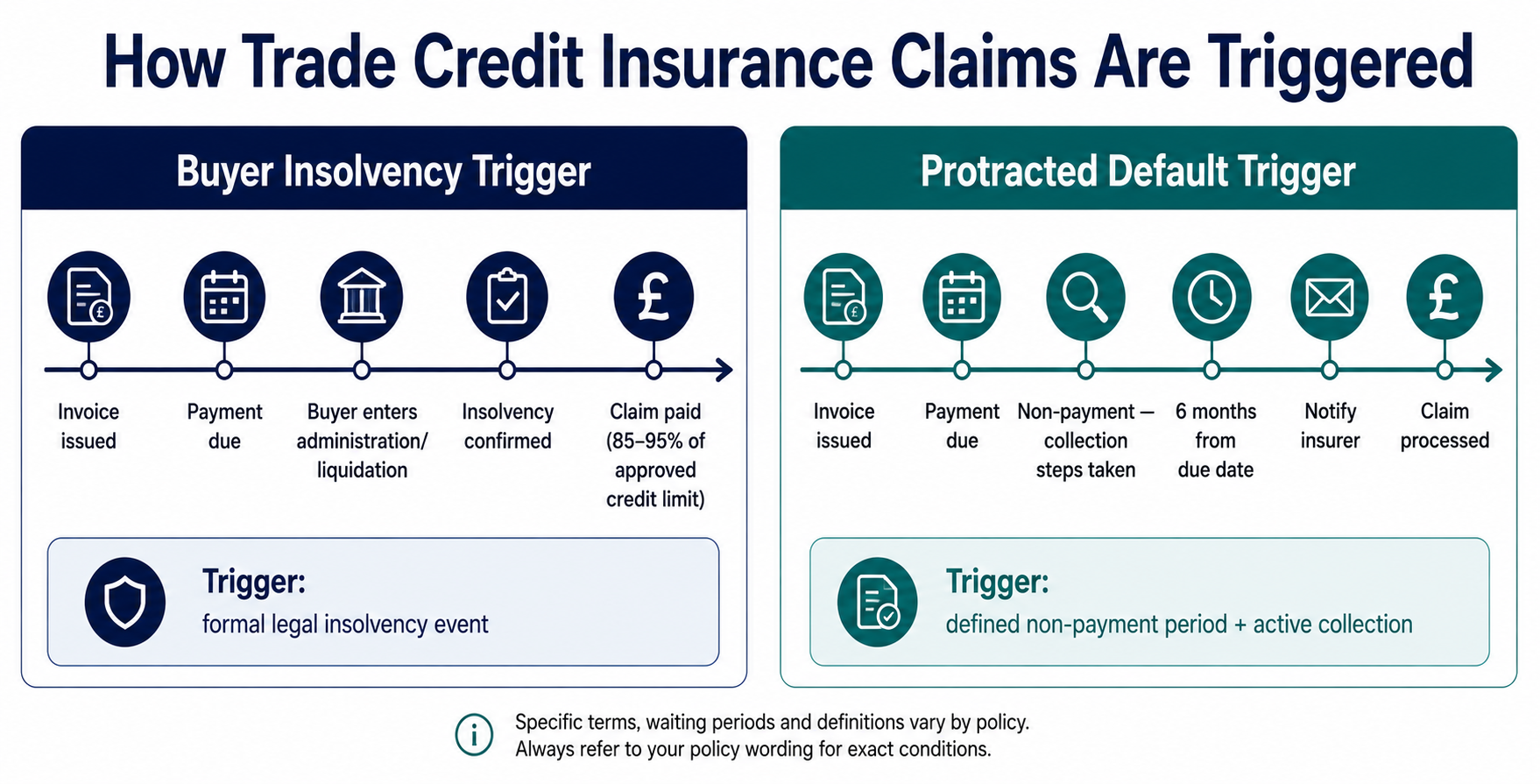

Buyer Insolvency

The primary and most commonly claimed trigger. A buyer enters formal insolvency proceedings — administration, liquidation, receivership, or equivalent in overseas jurisdictions — during the credit period or within a defined post-due-date window (typically 30–90 days after the invoice payment date).

The insurer pays the insured percentage of the outstanding invoice value (typically 85–95% of the approved credit limit for that buyer) once the formal insolvency event is confirmed.

What counts as insolvency: Administration, creditors' voluntary liquidation, compulsory winding up, appointment of a receiver, equivalent proceedings under foreign law for overseas buyers. Each of these triggers is precisely defined in the policy wording — confirming insolvency is a legal determination, not a commercial judgment.

Protracted Default

Protracted default covers non-payment that persists for an extended period beyond the invoice due date without formal insolvency proceedings — a buyer who simply stops paying. The waiting period before the insurer can be notified is typically six months from the contractual payment date (ITAR — insured trade account receivable — basis) or from the due date.

The practical difference from insolvency: Insolvency triggers are clear and confirmable. Protracted default triggers require the policyholder to have taken reasonable collection steps and to wait the defined period before notification. Passive acceptance of non-payment without active collection activity weakens the claim.

Political Risk (Export Credit)

For businesses trading internationally, trade credit insurance can extend to cover political risks — government actions in a buyer's country that prevent payment even where the buyer is willing. Political risk events include: import/export licence cancellation, currency inconvertibility (the buyer cannot convert local currency to pay in the contract currency), war and civil disturbance, and expropriation of assets.

Political risk coverage is most relevant for exporters to emerging market destinations and is typically purchased alongside commercial risk coverage as part of an export credit policy.

What Trade Credit Insurance Does NOT Cover

Understanding the exclusions prevents claim disputes and sets realistic expectations for what the product delivers.

Disputed invoices: If a buyer disputes the invoice — claiming the goods were not delivered, were defective, or that the specification was not met — the dispute must be resolved before the insurer will process a claim. A disputed invoice is not a credit insurance claim; it is a commercial dispute.

Invoices above the approved credit limit: Trade credit insurers set individual credit limits for each of your buyers. They will not pay a claim for an amount that exceeds the approved limit for that buyer, even if you extended more credit. If you supply beyond the insurer's approved limit, the excess is at your risk.

Late notification: Most trade credit policies require you to notify the insurer within a defined period of becoming aware that a buyer is in difficulty — often 30 days of learning of insolvency or 30 days after the protracted default period expires. Late notification can result in a claim being declined entirely.

Pre-existing disputes or known financial difficulty: Any buyer already known to be in financial difficulty at the time you seek coverage for them will not be included. Insurers decline credit limits for buyers they have assessed as high risk. You cannot insure a known bad debt retrospectively.

Cash sales and advance payments: Trade credit insurance covers credit sales — invoices issued on payment terms. Cash-on-delivery or advance-payment sales generate no credit exposure and are not insurable under trade credit policies.

The Three Policy Types — Choosing the Right Structure

Whole Turnover Policy

The standard and most commonly purchased structure. Covers all of your eligible trade debtors under a single policy. Each buyer is given an individual credit limit by the insurer — you can supply on credit up to that limit.

Benefits: Comprehensive protection across the debtor book, insurer monitoring of all buyers (providing early warning on any buyer showing stress), and a simpler administrative framework than managing individual buyer policies.

Limitations: You cannot cherry-pick only your riskiest buyers — the insurer requires the whole eligible debtor book to be covered to prevent adverse selection (only insuring buyers the seller already suspects are risky).

Most appropriate for: Businesses with diversified customer bases of five or more significant debtors, particularly in manufacturing, wholesale, and professional services.

Key Buyer or Specific Account Policy

Covers a small number of named, specific buyers rather than the whole debtor book. Appropriate where a business has one or two dominant customers representing a disproportionate share of receivables — a concentration risk that whole turnover policies do not isolate economically.

Most appropriate for: Businesses where one or two customers represent more than 40% of turnover, and the financial exposure to those specific buyers justifies dedicated coverage.

Single Invoice or Selective Credit Insurance

Selective cover allows the policyholder to choose which specific invoices or transactions to insure, on a deal-by-deal basis, rather than covering the entire debtor book or specific named accounts permanently.

Most appropriate for: Businesses with one-off large transactions with unfamiliar buyers, businesses exploring new markets or new customer types, or businesses where the debtor base is too small or concentrated for a whole turnover policy.

The adverse selection problem: Insurers who offer selective cover price it to reflect the fact that sellers will tend to insure their riskiest transactions. Selective cover premiums are higher per transaction than whole turnover rates, and not all insurers offer it.

How Trade Credit Insurance Is Priced

Trade credit insurance premiums are calculated as a percentage of insured turnover — the total eligible credit sales covered by the policy.

Standard premium range: 0.1%–0.5% of insured turnover. For a business with £3m of insured annual credit sales, the premium range is £3,000 per year at the low end (low-risk buyers, strong diversification) and £15,000 per year at the high end (higher-risk sectors, concentrated buyer base).

What Affects Your Premium Rate

- Buyer quality: Customer bases in distressed sectors (retail, construction, hospitality) are priced higher than financially robust sectors.

- Buyer concentration: A debtor book where one customer represents more than 30% of insured turnover creates concentration risk that insurers price as a specific loading.

- Credit management practices: Insurers review your credit vetting procedures, terms of sale, collection protocols, and debtor ageing profile. Documented processes and disciplined collection attract lower rates.

- Claims history: Prior trade credit claims signal debtor book quality. One or two prior claims is priced differently to a consistent loss history.

- Sector of operation: Recruitment, staffing, food distribution, and import/export are priced at different base rates reflecting historical claims frequency.

| Insured Turnover | Low-Risk Profile (0.10–0.15%) | Mid-Risk Profile (0.20–0.30%) | High-Risk Profile (0.35–0.50%) |

|---|---|---|---|

| £1,000,000 | £1,000–£1,500 | £2,000–£3,000 | £3,500–£5,000 |

| £2,500,000 | £2,500–£3,750 | £5,000–£7,500 | £8,750–£12,500 |

| £5,000,000 | £5,000–£7,500 | £10,000–£15,000 | £17,500–£25,000 |

| £10,000,000 | £10,000–£15,000 | £20,000–£30,000 | £35,000–£50,000 |

The Added Value Beyond the Policy — Why Credit Intelligence Matters

Trade credit insurance is one of the few insurance products that delivers measurable value before any claim is ever made.

Buyer credit monitoring: Your insurer continuously monitors the financial health of your insured buyers — tracking company accounts filings, County Court Judgments (CCJs), late payment data from credit bureaux, and intelligence from their own claims network. When a buyer shows early signs of financial stress, the insurer typically reduces or cancels the credit limit for that buyer — giving you early warning that you would not receive as an uninsured creditor.

The early warning value in practice: A wholesale distributor with £800,000 of receivables from a single retailer receives a notice from their trade credit insurer that the retailer's credit limit is being reduced from £200,000 to £50,000. This signals a specific financial concern about the retailer that the distributor's own credit team has not detected. The distributor reduces their exposure, tightens payment terms, and prepares for the retailer's possible failure — rather than continuing to build receivables that would be lost in a subsequent insolvency.

The discipline imposed on credit decisions: Businesses with trade credit insurance cannot exceed the insurer's approved credit limits without accepting the self-insured excess risk explicitly. This constraint imposes discipline on credit decisions — you cannot slip into giving excessive credit to a favoured customer without a deliberate and documented decision to go beyond the limit.

Who Should Consider Trade Credit Insurance

Strong case for trade credit insurance:

- Any B2B business where the top five customers account for more than 50% of turnover (concentration risk is the primary threat the policy mitigates)

- Manufacturers and wholesalers with long payment terms (45–90 days) and high outstanding receivables relative to turnover

- Exporters dealing with buyers in markets where insolvency risk or political risk is elevated

- Businesses seeking to access invoice financing or receivables-backed lending — many lenders require insured receivables as collateral

Weaker case for trade credit insurance:

- Businesses trading primarily with large, financially robust organisations (FTSE 350 companies, government departments, major NHS trusts) where insolvency risk is genuinely minimal

- Cash-based businesses or those trading predominantly on advance payment terms

- Businesses with highly diversified customer bases where no single customer exceeds 5% of turnover and the loss of any one would be commercially inconvenient but not financially material