Product liability insurance covers your legal costs and compensation when a product you manufacture, import or supply causes personal injury or property damage. Under the Consumer Protection Act 1987, UK producers are strictly liable for defective products — a claimant does not need to prove you were negligent, only that your product was defective and caused the harm. Any business that places products into the UK market — including ecommerce sellers importing from abroad — needs product liability insurance. Without it, a single serious claim can exceed £500,000 and falls entirely on the business or its owner.

Product liability insurance is a UK third-party liability policy that indemnifies a business against claims for personal injury or property damage caused by a defect in any product the business has supplied, manufactured, imported, repaired or sold under its own brand — including legal defence costs and compensation awarded to the claimant.

The Strict Liability Rule — Why Product Liability Is Fundamentally Different

In most UK civil liability, the claimant must prove negligence — that the defendant failed to take reasonable care and that failure caused the harm. Product liability under the Consumer Protection Act 1987 (CPA 1987) is different. It imposes strict liability on producers.

Under CPA 1987, a producer is liable for damage caused by a defective product if two things are shown:

- The product was defective — meaning it did not provide the safety that persons generally are entitled to expect (s.3 CPA 1987)

- The damage — personal injury or property damage — was caused by the defect

The claimant does not need to prove you were careless. They do not need to prove you knew about the defect. They do not need to prove you could have discovered it with reasonable diligence. If your product was defective and it caused harm, you are liable. This is the most important legal principle governing product liability in the UK and the reason why product liability insurance is not optional for any business that places products into the market.

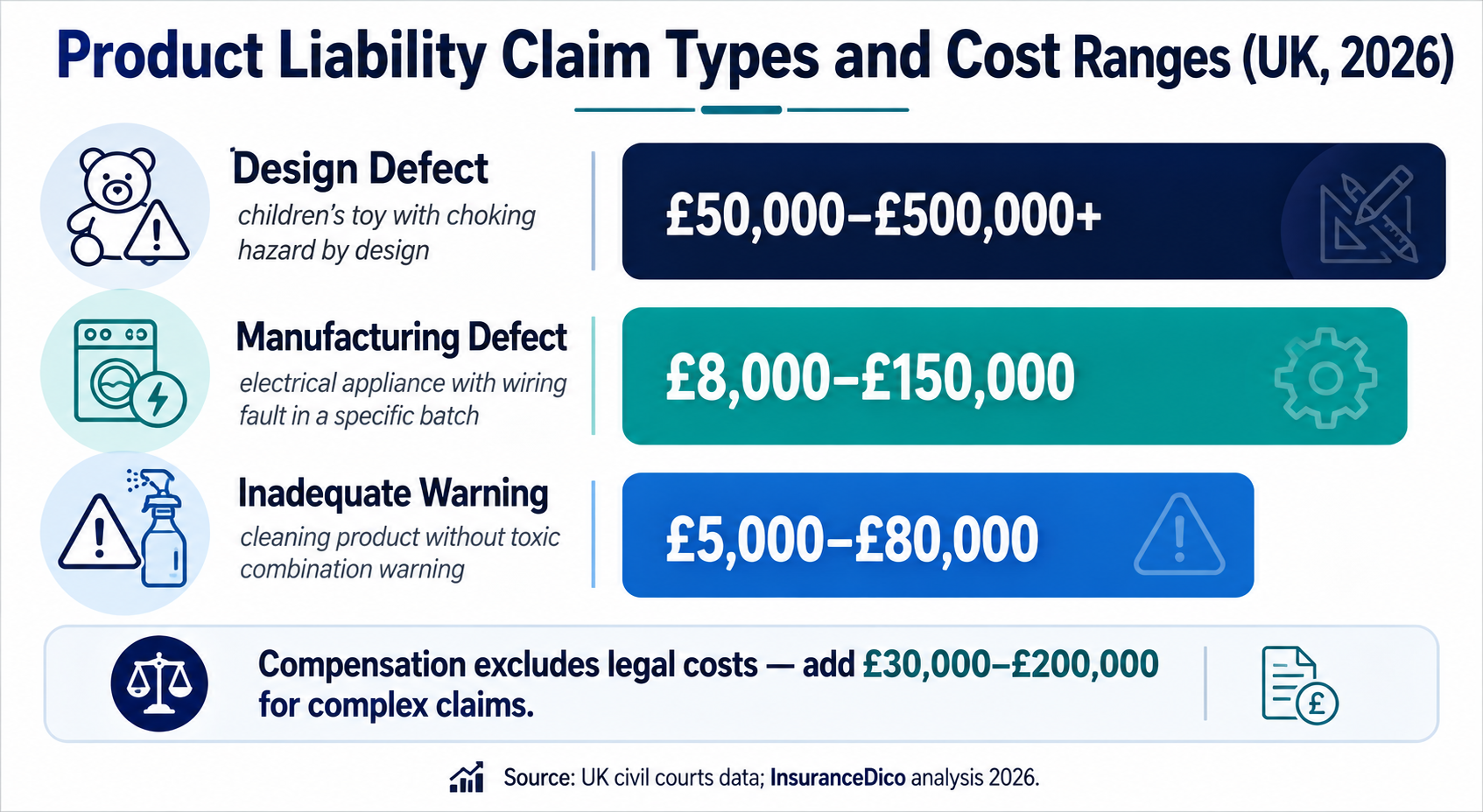

The Three Types of Product Defect Under CPA 1987

Design defect: the product was inherently unsafe as designed. Every unit manufactured to this design is defective. Example: a children's toy designed with parts small enough to be swallowed but not flagged as a choking hazard.

Manufacturing defect: the design was safe but a flaw in production made a specific unit or batch defective. Example: a batch of electrical appliances with a wiring fault caused by a manufacturing error.

Inadequate warnings or instructions: the product was not inherently unsafe but failed to warn users of a foreseeable risk associated with its use. Example: a cleaning product that does not warn against mixing with other household chemicals that together produce toxic fumes.

Who Is a 'Producer' Under the Consumer Protection Act 1987

The definition of who bears strict liability under CPA 1987 is broader than most businesses expect. The following categories are all producers under the Act:

- Manufacturers — any business that manufactures a finished product, including contract manufacturers producing under another brand's specification

- Component manufacturers — the maker of any component incorporated into the finished product (a faulty battery cell in a power tool: the battery maker and the tool brand are both liable)

- Importers into the UK — any business that imports a product into the UK from outside the UK (including from the EU, post-Brexit) is a producer for that product. Importing makes you the producer even if you did not design or manufacture it

- Own-brand suppliers — any business that puts its name, trade mark or distinguishing mark on a product is treated as a producer regardless of who actually manufactured the goods

- Retailers and distributors who cannot identify the manufacturer or importer — where a supplier cannot, on written request, identify their immediate supplier within a reasonable time (s.2(3) CPA 1987), they become the default producer

What Product Liability Insurance Covers

- Legal defence costs — solicitor and expert witness fees, product testing evidence and court attendance. Complex product liability litigation involving expert evidence regularly costs £40,000–£200,000 in defence fees before any compensation is assessed

- Compensation awards — damages ordered by a court or agreed in settlement, including personal injury, medical costs, loss of earnings, care costs for serious injuries and third-party property damage

- Fatal accident claims brought by dependants under the Fatal Accidents Act 1976

- Costs awarded against the insured in litigation

- Investigation and reasonable settlement costs with insurer consent

- Product recall costs — only where a specific recall extension has been added. Standalone recall expense is excluded under the base wording (see below)

What Product Liability Insurance Does NOT Cover

- The cost of the defective product itself — replacing, repairing or refunding the product is a commercial/warranty loss, not a liability claim

- Pure financial loss with no underlying injury or property damage — covered by Professional Indemnity, not product liability

- Product recall costs as standard — withdrawing, retrieving, transporting and destroying the defective batch requires a separate Product Recall extension or policy

- Damage to the insured's own property — covered by commercial property insurance

- Contractual warranties given to commercial customers that go beyond your legal obligations

- Deliberately defective products — no insurance covers a product knowingly made or supplied defective

- Punitive or exemplary damages in jurisdictions that award them (notably US claims)

- Asbestos, nuclear materials, tobacco and certain pharmaceuticals — standard market exclusions

- Products supplied for use in aircraft, space vehicles or certain medical implants — require specialist cover

Who Needs Product Liability Insurance

Manufacturers and Fabricators

The most obvious category. Any business that manufactures physical products for sale — from food and drink to industrial machinery — is both legally liable as a producer and potentially exposed to claims from every unit ever sold. Product liability insurance is standard practice and, in most supply chains, contractually required by buyers.

Importers — Including Small Ecommerce Businesses

Importing makes you the producer. Any UK business importing products from outside the UK for resale — regardless of the products' brand, origin, or whether you manufactured them — needs product liability insurance as the producer under CPA 1987.

The Amazon seller exposure: Amazon's Marketplace policies require sellers with more than £8,500 in sales per month to hold product liability insurance at a minimum of £1m, with Amazon named as additional insured. Even below this threshold, CPA 1987 strict liability applies regardless of Amazon's commercial policy.

Food and Drink Businesses

Food businesses carry product liability risk that is unique in both frequency and severity: allergic reactions (potentially fatal), microbial contamination, foreign-object injury and illness from improper preparation or preservation. Food product liability insurance is standard for any food business from artisan producers to restaurant chains.

Retailers of Third-Party Products

Retailers who can identify the manufacturer and UK importer for all products are not the producer under CPA 1987 — but they still face common-law negligence claims if they had reason to know a product was defective and continued to sell it. Retailers should also verify they can identify manufacturers and importers for every line they stock — where they cannot, they become the default producer.

Companies That Supply and Install

Businesses that supply and install products — HVAC contractors, solar panel installers, kitchen suppliers who also fit — face both Public Liability claims (for physical damage during installation) and product liability claims (if the installed product is defective and causes harm after handover).

2026 Product Liability Insurance Premiums

Product liability insurance is usually sold as part of a combined business package — bundled with Public Liability — rather than as a standalone product. The table below shows indicative premiums for the combined PL and product liability coverage.

| Business type | Products turnover | £1m cover | £2m cover | £5m cover |

|---|---|---|---|---|

| Food producer / artisan | Under £100k | £180–£320 | £235–£420 | £318–£570 |

| Consumer goods manufacturer | Under £500k | £220–£395 | £288–£518 | £388–£700 |

| Ecommerce seller (importing) | Under £250k | £165–£298 | £216–£390 | £292–£528 |

| Ecommerce seller (importing) | £250k–£1m | £285–£512 | £372–£672 | £503–£908 |

| Industrial/commercial manufacturer | Under £1m | £350–£628 | £458–£822 | £618–£1,112 |

| Retailer (own-brand products) | Under £500k | £195–£352 | £255–£462 | £345–£624 |

Factors That Significantly Increase Premiums

- Food and drink products — allergen contamination and illness risk produce material loadings, typically 30–60% above non-food equivalents at the same turnover

- Products for children — toys and nursery goods carry elevated liability risk and premium loadings of 20–50%

- Electrical and electronic products — fire risk from electrical faults adds 25–45%

- Products containing chemicals — toxicity and environmental contamination risk add 30–80%

- Export to the USA — US product liability litigation costs are an order of magnitude higher than UK. North American sales require either a US policy or a UK policy with explicit US/Canada extension, with substantial premium loading

Product Liability vs Product Recall — Two Different Policies

Product Liability responds when a defective product has already caused harm — someone is injured, property is damaged, a claim is made. The policy pays the third party. It does not pay the cost of recalling the rest of the batch.

Product Recall responds when a defect is identified and the business needs to withdraw the affected product from the market before further harm occurs. It pays for the logistics: customer notification, retrieval, transport, storage, destruction, replacement manufacture, PR/crisis communications, and additional staff time managing the recall.

Public Liability vs Product Liability — the Overlap

Public Liability (PL) responds when something the business does — or fails to do — on its premises or while carrying out work causes third-party injury or damage. Product Liability responds when something the business has supplied causes the harm, regardless of where the injury happens. The two are commonly written as a single Combined Liability policy with a shared limit, but the triggers are distinct: PL is about activity; Product Liability is about product.

Example: a customer slips on a wet floor in your shop and sustains a head injury — Public Liability. The same customer takes home a faulty kettle they bought from you that explodes and injures them — Product Liability. Same shop, same customer, two different triggers, two different parts of the same Combined Liability policy.