Directors and Officers (D&O) insurance pays the legal costs and any compensation when a director or senior officer is personally sued for a wrongful act in their management role — a decision, omission, or statement that causes financial harm to shareholders, employees, creditors or regulators. The company's professional indemnity insurance covers the business entity; D&O covers the individuals running it. Without D&O, a director facing a claim funds their legal defence personally — from savings, home equity and future earnings. Premiums start at £500 a year for small limited companies.

Directors and officers insurance is a UK liability policy that funds defence costs, settlements and judgments arising from claims alleging wrongful acts by individual directors, officers or senior managers acting in their corporate capacity — protecting personal assets when company indemnification is unavailable, prohibited or insufficient.

What D&O Insurance Covers — and Why It Differs From Every Other Business Insurance Policy

Every other business insurance product covers the company — its property, its liability to third parties, its professional outputs, its trading income. D&O insurance covers the individuals leading the company — the directors, officers and senior managers whose personal assets are exposed when decisions made in their official capacity are challenged by those who suffered financially.

The Legal Basis for Personal Director Liability

Directors of UK limited companies are not automatically protected from personal liability by the corporate structure. The limited liability framework protects shareholders from company debts; it does not protect directors from claims arising from their own conduct. Under the Companies Act 2006, directors owe specific legal duties: to act within their powers, to promote the success of the company, to exercise reasonable care and skill, to avoid conflicts of interest, and to declare interests in transactions. Section 214 of the Insolvency Act 1986 adds personal liability for wrongful trading.

Breach of any of these duties — even an honest mistake made under pressure — can trigger a personal claim against the director regardless of the company's own financial position.

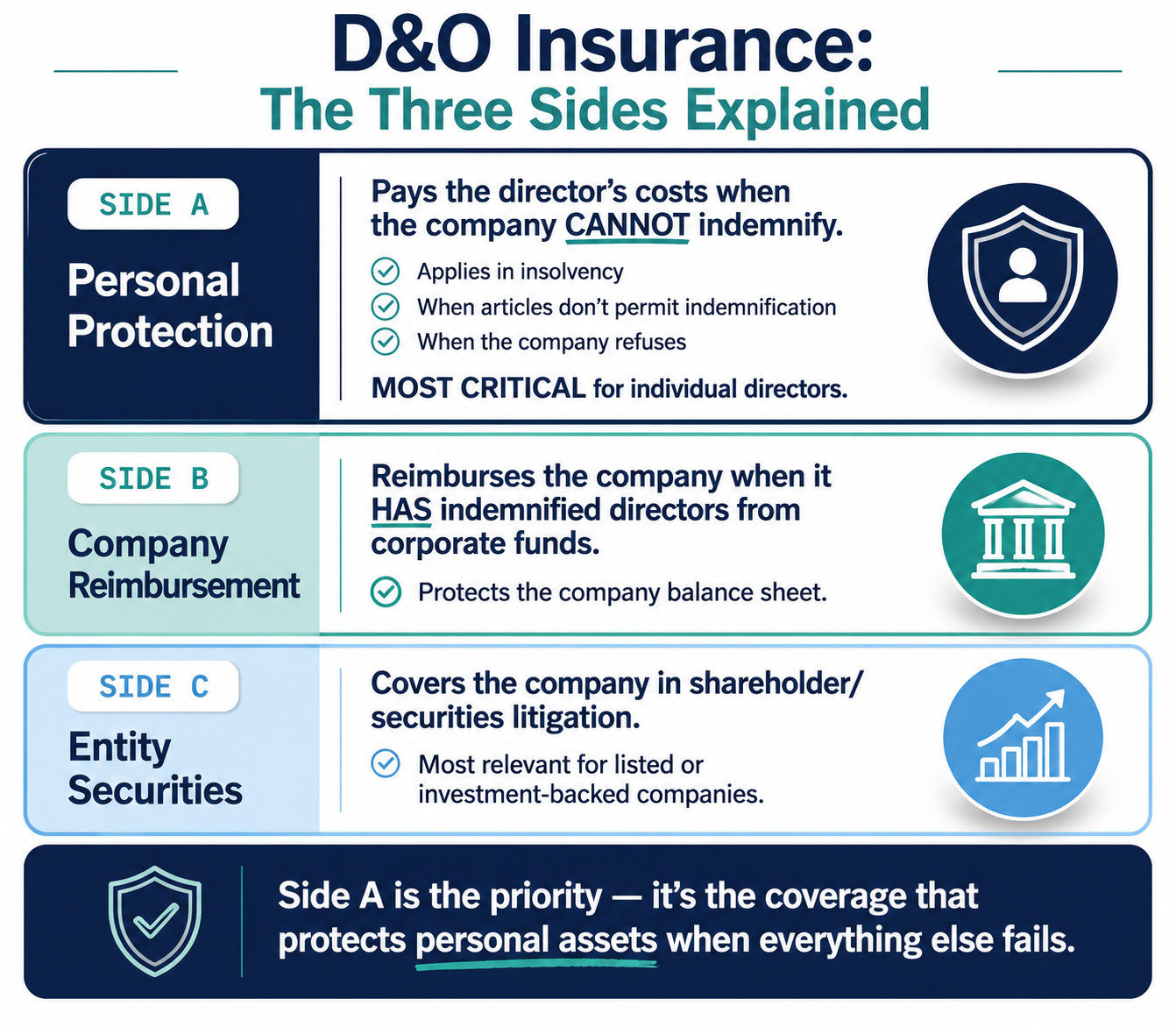

Side A — Direct Personal Protection

The most critical element. Pays the director's legal defence costs and any compensation or settlement from the director's own policy when the company cannot or will not indemnify them. This applies in insolvency, when the articles of association do not provide for indemnification, or where the claim specifically requires personal payment (notably derivative actions and regulatory penalties).

Side B — Corporate Reimbursement

Where the company has indemnified the director from corporate funds, Side B reimburses the company for those costs. This protects the company's balance sheet from the cost of defending its directors.

Side C — Entity Securities Coverage

Covers the company itself in securities litigation — claims by shareholders alleging misleading statements that affected the share price. Most relevant for listed companies and those seeking investment. UK SMEs without securities exposure typically buy Sides A and B only.

Who Makes Claims Against Directors — the Specific Claimant Categories

D&O claims come from a wider range of sources than most directors anticipate. Understanding who can claim and why informs both the coverage decision and the risk management approach.

Shareholders and Investors

Shareholders can claim against directors for breaches of fiduciary duty — decisions that harmed the company's value or that were made in the directors' own interests rather than the company's. In smaller companies, minority shareholders who feel their interests were not fairly considered can bring unfair prejudice petitions under Section 994 of the Companies Act 2006. VC- and PE-backed companies face higher D&O claim frequency from sophisticated investors with specialist legal resources.

Employees

Employees can bring D&O claims for decisions that affected their employment — mass redundancies handled incorrectly, discrimination or harassment that directors failed to prevent, or pension scheme management failures that damaged employee retirement benefits. Employment tribunal awards against the employer go through the company's employers' liability cover; a director personally named for discriminatory conduct or as a trustee of an underperforming pension scheme faces a personal claim that responds under D&O.

Creditors and Liquidators

When a company becomes insolvent, creditors who did not recover their debts may pursue directors personally for wrongful trading (continuing to trade when directors knew insolvency was inevitable), fraudulent trading, and misfeasance (misapplication of company assets before insolvency). Liquidators have a specific duty to investigate director conduct in the run-up to insolvency. Post-COVID, the volume of liquidator claims against directors increased significantly as pandemic-era companies failed with unpaid HMRC debt.

Regulators

The Senior Managers and Certification Regime (SMCR) holds senior managers in financial services personally accountable for areas within their responsibility. FCA enforcement actions increasingly include parallel personal action against the named senior manager. Beyond the FCA, HMRC investigations, HSE prosecutions following workplace fatalities, CMA inquiries and ICO enforcement can all result in personal regulatory action against named directors. D&O cannot insure the fine, but it pays the substantial legal costs of responding.

When D&O Insurance Is Non-Negotiable

VC- and PE-Backed Companies

Venture capital and private equity investors almost universally require D&O insurance as a condition of investment. Most term sheets include a representation that the company will maintain D&O at a specified coverage level throughout the investment period. Companies that do not have cover in place at closing are in breach of their investment representations from day one.

Companies with Regulatory Obligations

Any company operating in a regulated sector where directors carry personal compliance obligations — financial services (FCA/SMCR), healthcare (CQC), legal services (SRA), food and drink (FSA) — faces elevated personal regulatory risk. The cost of responding to a regulatory investigation without D&O insurance is entirely personal.

Companies with Employee Headcount Above About 25

As companies grow, the complexity of employment decisions increases — redundancies, restructurings, performance management, senior executive changes. Each creates potential personal claims against the directors who made or approved them. At this scale a D&O policy is cost-effective protection against the growing personal liability that comes with size.

Startups and Companies in Their First Three Years

The first three years of a company's life carry statistically elevated insolvency risk. If the company fails, directors' conduct in the run-up is routinely scrutinised by liquidators. D&O insurance that covers this period — including defence against wrongful trading allegations — is the most important personal financial protection a startup founder can hold.

2026 D&O Insurance Cost — Premium Data by Company Type

D&O premiums are determined by company revenue, structure (listed vs private), industry sector, number of directors, jurisdictions of operation, claims history and the coverage limit selected.

| Company revenue | Coverage limit | Indicative annual premium |

|---|---|---|

| Under £500k | £500k–£1m | £500–£850 |

| £500k–£2m | £1m–£2m | £750–£1,400 |

| £2m–£10m | £2m–£5m | £1,200–£2,800 |

| £10m–£50m | £5m–£10m | £2,800–£6,500 |

| £50m–£200m | £10m–£25m | £6,500–£18,000 |

Sector Loadings That Significantly Increase Premiums

- Financial services: FCA regulatory risk and SMCR personal accountability load D&O premiums by 30–80% above standard.

- Healthcare and care sector: CQC registration and the elevated personal liability attached to care quality decisions add 25–60%.

- Construction: HSE personal prosecution risk and contractor liability exposure add 20–45%.

- Technology / SaaS with data handling: ICO and GDPR enforcement risk adds 15–35%.

What D&O Insurance Does Not Cover

Fraud and dishonest acts. No D&O policy covers claims arising from deliberate fraud, knowing dishonesty or criminal acts by the director. Where fraud is alleged, the policy funds the defence until fraud is proven by a final, non-appealable judgment — at which point coverage typically ceases and previously paid defence costs may be recoverable from the director.

Personal enrichment. Benefits a director deliberately took at the company's expense — conflicts of interest exploited for personal gain — are excluded. A director who awarded contracts to their own company without board approval faces an excluded claim.

Employment-related claims made by the director themselves. A director who is also an employee claiming constructive dismissal or unpaid wages as an employee is making an employment claim, not a D&O claim. These fall to the company's employers' liability cover.

Bodily injury and property damage. These are public liability claims against the company, not D&O claims against the individual.

Fines and penalties from regulators. D&O covers the legal costs of responding to regulatory investigations and enforcement. It does not cover the fines themselves — regulatory fines are uninsurable under UK public policy.

D&O vs Professional Indemnity — the Overlap for FCA-Regulated Firms

For FCA-authorised firms — advisers, brokers, fund managers, accountants in regulated practice — the line between a D&O claim and a Professional Indemnity (PI) claim is the most frequently litigated coverage question. The shorthand: PI covers claims arising from the firm's services to clients; D&O covers claims arising from the directors' management of the firm itself.

An FCA enforcement action against the firm and its senior management function holders typically triggers both policies: PI for the regulatory consequences attached to client work, D&O for the personal liability of the SMF holder under SMCR. Both should be reviewed together; gaps and overlaps are common, and dual-tower programmes are standard for firms with material regulatory exposure.

Which UK Companies Should Carry D&O

- Any company with external shareholders or investors (VCs, angels, EIS/SEIS investors) — a condition of nearly every UK investment term sheet

- Any FCA-authorised firm — SMCR personal accountability makes individual D&O essentially mandatory

- Any company with employees — employment practices claims (discrimination, unfair dismissal, whistleblowing) are the most common trigger for SME D&O claims

- Any company subject to specific regulatory oversight (HSE-regulated industries, ICO data controllers, Pensions Regulator-supervised schemes)

- Any company contemplating insolvency, restructuring or a transaction — wrongful trading exposure for directors is at its peak in distressed scenarios

- Charities and not-for-profits — trustees of UK charities have personal liability for breach of trust under the Charities Act 2011; D&O for charities is sometimes branded as Trustee Indemnity Insurance