Life insurance pays a cash lump sum or regular income to your chosen beneficiaries if you die during the policy term. The most common type — term life insurance — covers a fixed period (10–40 years) and costs £8–£16 per month for a healthy 30-year-old non-smoker with £200,000 of cover. The right amount of cover depends on your outstanding mortgage, your dependants' income needs, and your existing financial assets. The ABI reported a 98.2% life insurance claims payout rate in 2023.

Why Most UK Families Are Underprotected — and What the Data Shows

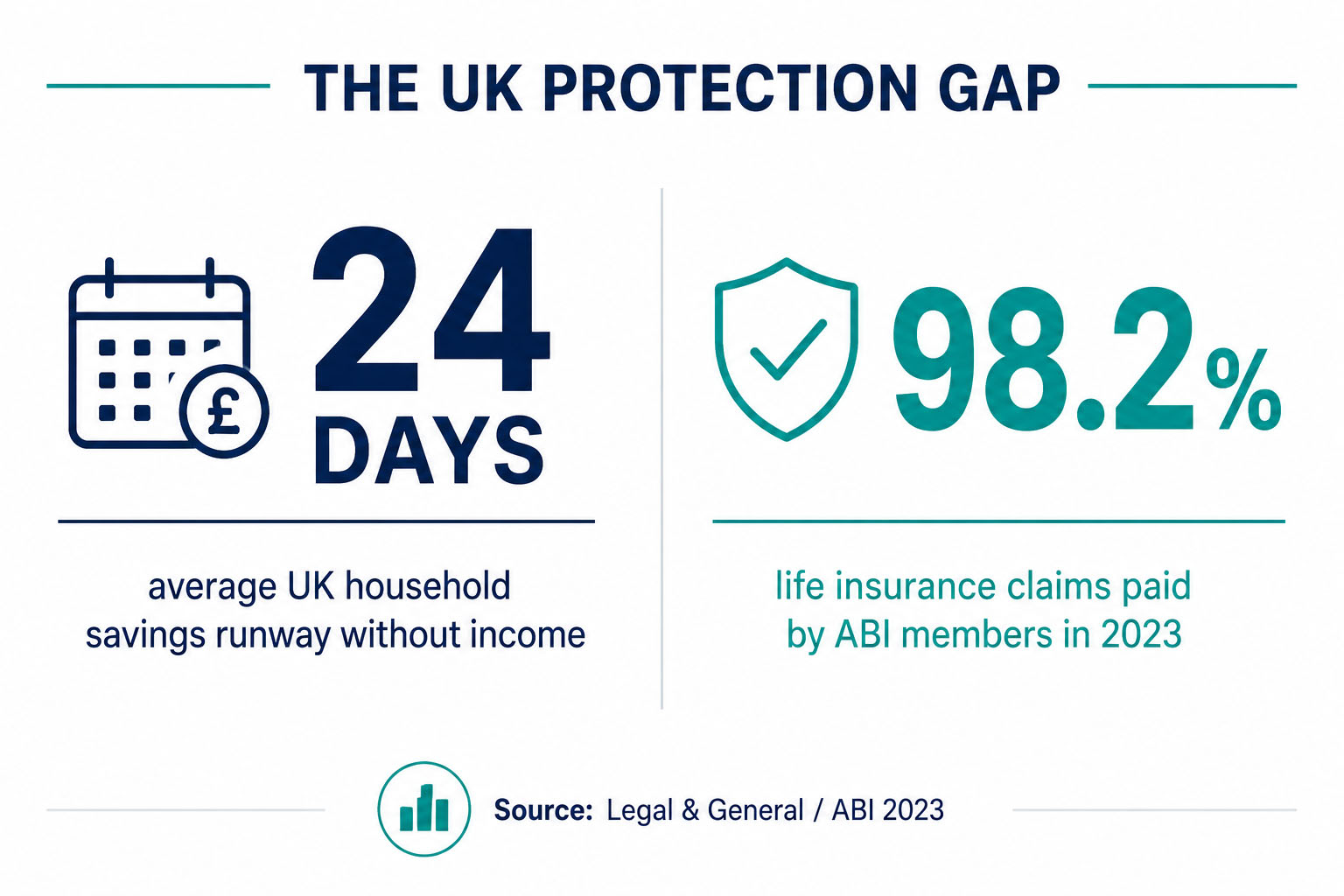

The UK has a significant protection gap. According to Legal & General's Deadline to Breadline report, the average UK household would exhaust its savings in just 24 days if the main earner lost their income without warning. Research from Swiss Re estimates the UK's mortality protection gap — the difference between existing life insurance coverage and what households actually need — at £2.4 trillion.

The reasons people underinsure are consistent across studies: cost (usually overestimated by a factor of three to five), complexity (most people do not know how much cover they need), and inertia (it is easy to defer). The actual cost of term life insurance is lower than most people believe: a healthy non-smoking 30-year-old can cover £200,000 for 25 years for approximately £9–£14 per month.

This guide gives you the framework to calculate what you need and understand what you are buying — without a sales agenda.

Why the gap exists in the regulated UK market. The Financial Conduct Authority's 2024 Financial Lives survey found that 41% of UK adults aged 25–54 have no life insurance at all, and a further 23% hold cover that has not been reviewed for more than five years. Life events that should trigger a coverage review — moving house, having a child, taking on additional debt, starting a business — frequently do not. The result is a population in which the people most exposed to financial loss (recent first-time buyers with young children) are also the least likely to hold cover proportionate to that exposure.

The cost of underinsuring vs the cost of insuring. A £200,000 policy at £12 per month costs £3,600 across a 25-year term. The cost of a surviving partner being unable to repay a £200,000 mortgage on a single income is the difference between keeping the family home and selling it under duress. The asymmetry is not subtle, yet it is consistently underweighted in household financial decisions.

The remainder of this guide breaks the market into six product types, walks through the calculation that determines how much cover you actually need, presents indicative 2026 premium data by age and coverage band, and explains how pre-existing medical conditions interact with underwriting. Each section links to deeper cluster guides for readers who want a single-product deep-dive.

The 6 Types of Life Insurance — Which One You Actually Need

Life insurance is not one product. These six types cover fundamentally different needs at different price points.

1. Term Life Insurance — the Right Choice for Most People

Term life insurance pays a lump sum if you die within a fixed term — typically 10 to 40 years. Premiums are fixed for the full term and are set at the start based on your age, health, smoking status, and coverage amount.

Two variants:

- Level term: The payout amount stays the same throughout the policy. Suited to income replacement for dependants and debts that do not reduce over time.

- Decreasing term: The payout reduces over time, usually aligned to an outstanding mortgage balance. Costs 20–30% less than level term for the same starting coverage amount. Suited specifically to mortgage protection.

Who it's for: Anyone with a mortgage, dependants relying on their income, or both. The most cost-effective way to provide financial protection for a defined period.

Who it's not for: People who want guaranteed payout regardless of when they die (that requires whole of life), or people seeking a policy that builds cash value.

A practical pairing. A common structure for a homeowner with dependants is a decreasing term policy aligned to the mortgage (cheap, reduces in step with the outstanding balance) paired with a separate level term policy for income replacement (constant payout for the dependency period). The two policies together cost less than a single large level term policy and map more accurately to how the underlying liability actually behaves over time.

2. Whole of Life Insurance — Guaranteed Payout, Higher Premium

Whole of life insurance pays a guaranteed lump sum whenever you die — there is no term limit. Because the payout is certain (barring fraud or non-disclosure), premiums are significantly higher than term life for the same coverage amount.

When it makes financial sense: Whole of life is most commonly used for inheritance tax planning. Policies written in an appropriate trust can pay outside of your estate, providing your beneficiaries with funds to pay an inheritance tax bill without liquidating other assets. For this specific purpose, the guaranteed payout justifies the premium.

When it does not make financial sense: If your goal is to provide income replacement or mortgage protection for dependants for a defined period, term life delivers more coverage per pound of premium. Paying for a guaranteed payout that you may not need until you are 85 is expensive protection.

3. Critical Illness Cover — a Lump Sum on Diagnosis, Not Death

Critical illness cover pays a tax-free lump sum if you are diagnosed with one of the specified serious illnesses listed in your policy — whether or not you die. Covered conditions typically include: cancer (most types), heart attack, stroke, multiple sclerosis, and major organ failure.

The ABI model definition sets a baseline. All ABI member insurers must cover a core list of conditions using standardised definitions. 'Enhanced' definitions — covering more conditions or less severe presentations — are available at higher premiums and vary by insurer.

ABI 2023 data: Critical illness insurers paid 91.2% of claims in 2023. The most common claim triggers were cancer (61% of all CI claims), heart attacks (13%), and strokes (7%). The average claim payout was £69,300.

Critical illness vs life insurance: They serve different purposes. Life insurance protects your family if you die. Critical illness cover protects your financial position if you survive a serious illness but cannot work or face significant treatment costs. Both are often needed — they are not substitutes.

Combined vs standalone policies. Many insurers sell a combined life and critical illness policy that pays out on the first event — death or a covered diagnosis — and then terminates. This is cheaper than two separate policies but means a critical illness payout extinguishes the death-benefit cover for any surviving dependants. Standalone policies, written either as separate contracts or as 'additional benefit' (so each peril has its own sum insured), are materially more expensive but produce the financial result most families need: a cover that survives a serious illness and still pays on subsequent death.

Children's critical illness cover. Most adult CI policies include a small amount (typically £25,000) of free children's cover that pays on diagnosis of a serious childhood condition. The list of covered conditions is narrower than the adult schedule and the cover usually ends at age 18 or 21. It is a useful by-product of an adult policy, not a substitute for considering standalone protection where dependants are particularly exposed.

4. Income Protection Insurance — the One Most People Forget

Income protection insurance pays a monthly income — typically 50–70% of your gross salary — if you are unable to work due to illness or injury. Unlike critical illness, which pays a lump sum on diagnosis of a specific condition, income protection covers any illness or injury that prevents you from doing your job.

Why it matters: The UK's statutory sick pay is £116.75 per week (2026 rate) for a maximum of 28 weeks. If you earn £2,800 per month and fall ill for a year, statutory sick pay covers approximately £6,000 of your £33,600 annual income. The gap is real, significant, and largely unplanned for.

What to check: The 'definition of incapacity' in your policy — whether it pays when you cannot do your own occupation or only when you cannot do any occupation. Own-occupation cover is more expensive but pays in more circumstances.

Deferred period: The waiting period before your policy pays (typically 4, 13, 26, or 52 weeks). Choose the deferred period that matches your emergency fund runway — a longer deferred period significantly reduces your premium.

5. Over-50s Life Insurance — Guaranteed Acceptance, Defined Terms

Over-50s life insurance accepts applicants aged 50–85 without medical questions or underwriting. A fixed premium buys a fixed payout — typically £5,000–£25,000 — paid on death.

The critical limitation most buyers miss: Most over-50s plans have a waiting period (usually 12–24 months) during which the full payout is not available. If you die in this period, premiums are refunded rather than the full sum insured being paid.

The financial reality: Calculate the breakeven point before purchasing. If you pay £30 per month for a £15,000 payout, you need to live 41.7 months (3.5 years) after the waiting period ends to have paid in less than the payout. If you live 20 years after taking out the policy, you will have paid in £7,200 to receive £15,000 — a reasonable return. If you live 10 years after the waiting period, you will pay in £3,600 for a £15,000 payout — a better return. The longer you live, the less value the policy provides relative to its cost.

6. Business Life Insurance — Protecting the Business, Not Just the Individual

Key man insurance and relevant life policies are life insurance products specifically structured for business use. They protect the business from financial loss caused by the death of an essential employee or director.

A relevant life policy is a single-person death-in-service scheme arranged by the employer. The premium is typically corporation-tax deductible and does not count as a P11D benefit — making it significantly more tax-efficient than personal life insurance for company directors.

Key person insurance is owned and paid for by the company on the life of a director, founder, or other employee whose death would materially damage the business — typically through loss of specialist knowledge, key client relationships, or the ability to service a loan personally guaranteed by that individual. The sum insured is sized to the financial impact on the business (lost revenue while a replacement is recruited, repayment of guaranteed debt, or buy-out of the deceased's shareholding under a cross-option agreement).

Shareholder protection. A separate but related arrangement, shareholder protection insurance funds a cross-option agreement so that surviving shareholders can buy out the deceased's stake from their estate at a pre-agreed valuation. Without it, founders' families can end up holding shares they cannot easily sell and the surviving business is left with a passive shareholder it did not choose. This is one of the most under-implemented protections in UK SMEs and is straightforward to set up at incorporation.

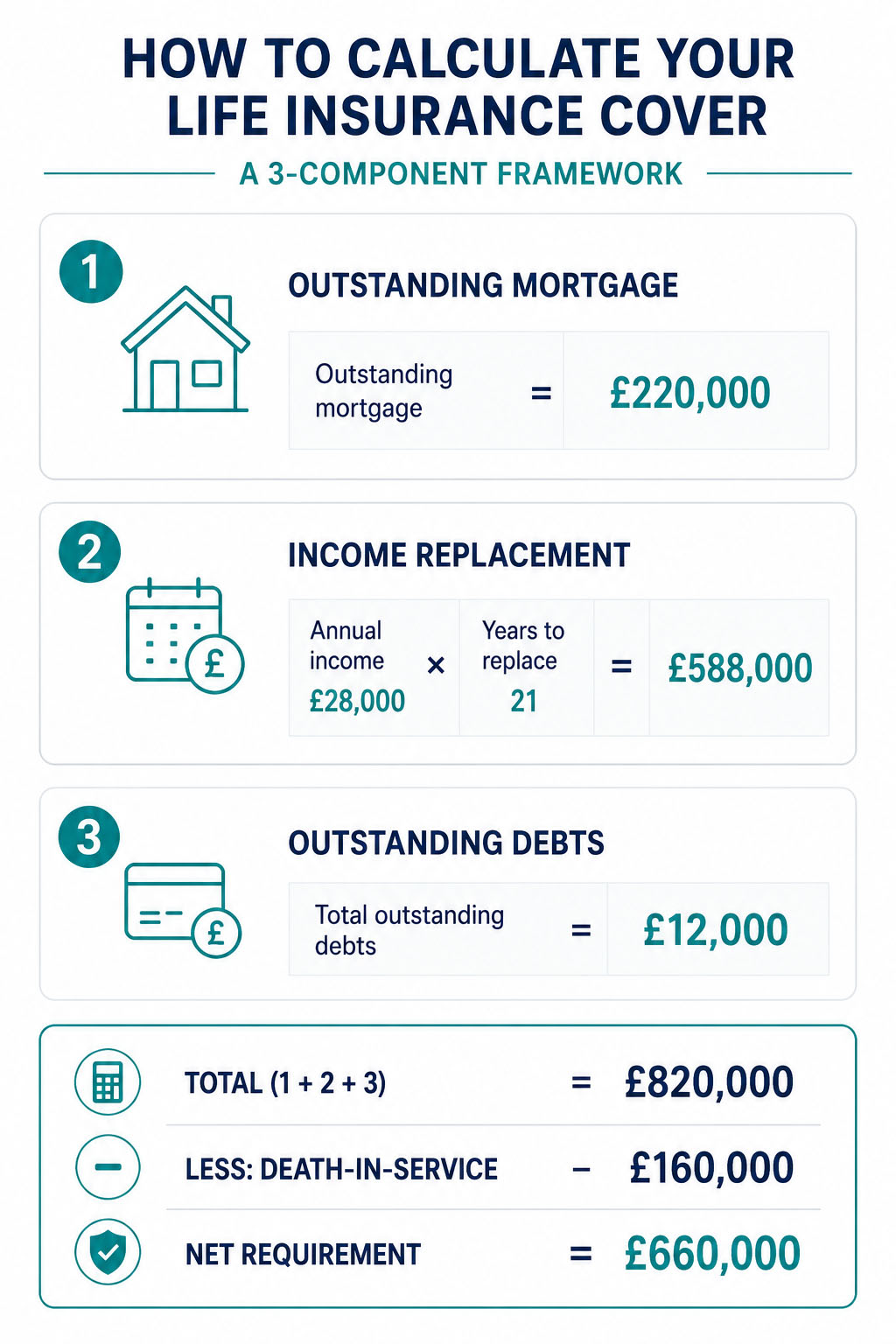

How Much Life Insurance Do You Actually Need? The Calculation

Most guidance defaults to '10 times your salary.' This is a starting point that frequently produces the wrong answer. The correct calculation has three components.

Component 1: Mortgage and secured debt. Your outstanding mortgage balance. This is the most straightforward figure — the surviving partner needs sufficient funds to pay off the mortgage or continue servicing it independently.

Component 2: Income replacement for dependants. Calculate the annual income your family needs to maintain their standard of living. Multiply by the number of years until your youngest child is financially independent (typically age 21–25). A 35-year-old with a 3-year-old child needs approximately 21 years of income replacement. At 70% replacement rate: if you earn £40,000, your family needs £28,000 per year. Over 21 years, that is £588,000 in today's terms (before inflation adjustment).

Component 3: Outstanding unsecured debts. Personal loans, car finance, business debts you have personally guaranteed.

Add the three components. Subtract existing coverage:

- Death-in-service benefit from your employer (typically 4× salary — check your employee handbook)

- Existing life insurance policies

- Savings and investments that are readily accessible

The result is your net coverage requirement.

Three Worked Examples

Example 1 — Sole earner with young children: Income £45,000. Mortgage £220,000 outstanding. Two children aged 3 and 6. Non-earning partner. Outstanding car finance £8,000. → Mortgage £220k + income replacement (£31,500 × 20 years = £630,000) + debts £8,000 = £858,000 required.

Example 2 — Dual income couple, no children: Each earns £35,000. Joint mortgage £180,000. No dependants. Surviving partner can service mortgage on their income alone. → Primary requirement: eliminate mortgage stress. Each partner: £180,000–£200,000 in level or decreasing term cover.

Example 3 — Business owner, complex obligations: Income £80,000. Mortgage £350,000. Two children. Director's loan £60,000 personally guaranteed. No death-in-service. → Mortgage £350k + income replacement (£56,000 × 18 years = £1,008,000) + business debt £60k = £1,418,000 required.

Inflation and indexation. A £600,000 level term policy purchased today buys £600,000 of cover in 25 years' time — and 25 years of consumer-price inflation will have eroded its real value materially. Most UK insurers offer an indexation option that increases the sum insured each year in line with RPI or a fixed percentage (typically 3–5%), with the premium rising proportionately. For cover sized to dependants' income over a long horizon, indexation is generally worth the additional premium; for cover sized to a known mortgage balance that itself reduces, it is not.

Trusts and beneficiary nomination. Writing a personal life insurance policy 'in trust' achieves two things: the payout falls outside your estate for inheritance tax purposes, and it is paid directly to the trustees on production of the death certificate rather than waiting for probate. Probate currently takes 16 weeks on average in the UK and longer where the estate is contested. Most insurers provide a free trust template at the point of application — using it should be the default, not an afterthought.

How Much Does Life Insurance Cost? (2026 Data)

The table below shows indicative 2026 market premiums for a non-smoking individual in good health. Smoking status approximately doubles the premium at any age.

| Age | £150,000 level term, 20 years | £300,000 level term, 25 years | £500,000 level term, 25 years |

|---|---|---|---|

| 25 | £5–£8/month | £9–£14/month | £13–£22/month |

| 30 | £6–£10/month | £11–£18/month | £17–£28/month |

| 35 | £8–£14/month | £15–£26/month | £24–£42/month |

| 40 | £13–£22/month | £24–£42/month | £38–£68/month |

| 45 | £20–£36/month | £38–£65/month | £60–£105/month |

| 50 | £33–£58/month | £62–£110/month | £100–£175/month |

What drives your premium beyond age:

- Smoking status: Classify as smoker if any tobacco or nicotine product in past 12 months. Vaping is treated as smoking by most UK insurers in 2026. Premiums approximately double.

- Health history: Conditions that typically increase premiums include type 2 diabetes (50–150% loading depending on HbA1c control), treated hypertension (20–80% loading), BMI above 30 (5–50% loading by BMI bracket), and previous serious illness. Conditions that may result in exclusions rather than loadings include active mental health treatment and some heart conditions.

- Policy term: Longer terms cost more. A 30-year policy for the same coverage amount costs approximately 40–60% more per month than a 20-year policy.

- Coverage amount: Premiums are broadly linear with coverage amount until underwriting thresholds (typically £750,000–£1,000,000) where full medical underwriting is triggered.

Getting Life Insurance With Pre-Existing Medical Conditions

Pre-existing conditions complicate life insurance underwriting, but they rarely make it impossible. Insurers take one of four approaches:

- Standard terms: Cover at normal premium rates, typically where the condition is well-managed, stable, and does not significantly increase mortality risk.

- Non-standard terms (rated policy): Cover at a higher premium reflecting the additional risk. Premium loadings of 50–200% are common for conditions like managed diabetes, treated hypertension, and obesity.

- Exclusion: Cover is offered but the specific condition is excluded from covered causes of death. This is more common in critical illness underwriting than life insurance.

- Declined: Cover is refused. This is less common than people assume — most conditions can be covered at some price. If declined by one insurer, a specialist broker accessing Lloyd's and non-standard markets can often find coverage.

Disclosure obligations under the Consumer Insurance (Disclosure and Representations) Act 2012. UK consumers are required to take 'reasonable care' to answer the insurer's questions accurately and completely. The insurer cannot void a policy for an honest mistake, but deliberate or reckless misrepresentation is grounds for full avoidance. The practical implication: answer every question on the application form, do not omit conditions because they 'feel resolved', and disclose family history where the form asks for it. If you are unsure whether something is material, disclose it and let the underwriter decide.

Working with a specialist broker for non-standard cases. For applicants with diabetes, treated cancer, mental health history, high-risk occupations (offshore, aviation, certain trades), or hazardous pursuits (climbing, motorsport, diving below 30 metres), a broker with access to specialist underwriters at Lloyd's and the non-standard market will typically secure cover at materially better terms than a direct application to a mainstream insurer. The broker is paid commission by the insurer; you pay nothing extra.

How to Buy Life Insurance in the UK — Direct, Comparison, or Broker

There are three routes to placing a life insurance policy in the UK in 2026, and the right one depends on the complexity of your case.

Direct from an insurer. Best when your case is straightforward: standard occupation, no significant medical history, single applicant, mainstream sum insured (under £750,000). Insurers' direct channels — Aviva, Legal & General, Royal London, Vitality — offer competitive premiums and increasingly streamlined online underwriting. The trade-off is that you only see one insurer's terms.

Through a price comparison website. Aggregators (Compare the Market, MoneySuperMarket, GoCompare) panel a subset of insurers and surface the cheapest premium for the cover band you select. They work well for level and decreasing term cover at standard rates. They do not handle non-standard underwriting well: a 'declined' from one panel insurer does not trigger a re-quote across non-panel markets, and the comparison results assume standard health terms.

Through an independent protection broker (regulated by the FCA, ideally Protection Distributors Group member). Best when your case is non-standard, when you want cover above £750,000, when you need a combined life-and-critical-illness arrangement structured carefully, or when you want the policy written in trust. The broker is paid commission by the insurer and the comparison quote includes that cost — there is no extra charge to you. For higher-complexity cases the access to specialist underwriters and the structuring advice typically more than offset any premium difference versus direct purchase.

Regulatory protection. All UK life insurance policies are regulated by the Financial Conduct Authority (FCA). In the unlikely event your insurer fails, the Financial Services Compensation Scheme (FSCS) covers 100% of long-term insurance liabilities with no upper limit. Complaints that are not resolved by the insurer within eight weeks can be escalated to the Financial Ombudsman Service (FOS) at no cost to the consumer.