Specialist insurance covers risks that fall outside the standard buildings, contents, car, and life insurance categories — pet treatment costs, wedding cancellation, gadgets, self-employed income protection, and non-standard vehicles. Most specialist products are underwritten by the same major insurers as standard policies but distributed through narrower channels. The key decision in every specialist category is the same: does the premium cost less than the expected value of the risk being transferred? This guide answers that question with data for each product type.

Specialist insurance UK is a group of regulated non-standard insurance products — pet, wedding, gadget, self-employed liability and income protection, over-50s life cover, and classic vehicle policies — designed to cover risks that fall outside mainstream buildings, contents, motor and life insurance categories.

Pet insurance — the maths most pet owners get wrong

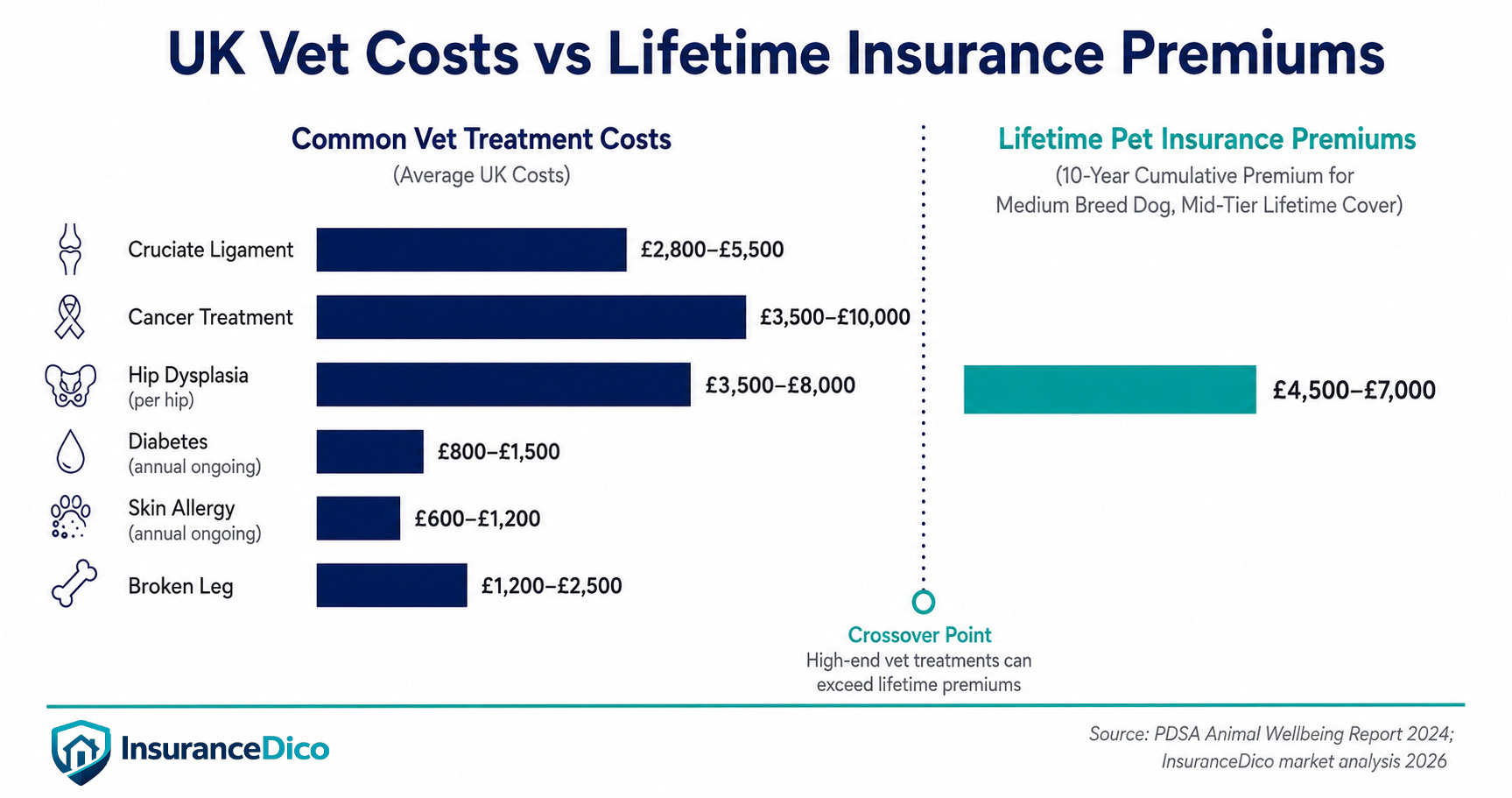

The UK has 13 million dogs and 12 million cats. The People's Dispensary for Sick Animals (PDSA) estimates that only 4.1 million pets are insured — meaning the majority of UK pet owners are self-insuring a risk that regularly exceeds £1,000 per treatment episode.

The argument against pet insurance is straightforward: premiums accumulate over a pet's lifetime and may exceed what you ever claim. The argument for it is equally straightforward: a single serious illness or injury can cost £3,000–£12,000 in a single episode, and most pet owners do not have this in accessible savings.

| Pet Type and Breed | Monthly Premium | Annual Premium |

|---|---|---|

| Cat (mixed breed, under 3) | £12–£22 | £145–£265 |

| Cat (pedigree, under 3) | £18–£35 | £215–£420 |

| Dog (small breed, under 3) | £22–£38 | £265–£455 |

| Dog (medium breed, under 3) | £28–£55 | £335–£660 |

| Dog (large breed, under 3) | £35–£75 | £420–£900 |

| French Bulldog (under 3) | £60–£130 | £720–£1,560 |

| Dog (any breed, 8–10 years) | £80–£180+ | £960–£2,160+ |

The three types of pet insurance — and the one worth buying

Accident only covers veterinary treatment following an accident but not illness. The cheapest option at £5–£15 per month — suitable only if you genuinely cannot afford broader cover, since most veterinary expenditure is illness-related, not accident-related.

Time-limited (annual cover) covers each condition for 12 months from first treatment. After 12 months or when the annual limit is reached (whichever comes first), that condition becomes excluded — permanently. For chronic conditions that develop and require ongoing treatment, this policy type provides cover for the first year and nothing thereafter.

Lifetime cover covers each condition up to the policy limit per year, with the limit resetting at each annual renewal. The only policy type that provides meaningful protection for chronic conditions such as diabetes, arthritis, allergies, and heart disease — all of which require ongoing annual treatment. Lifetime cover is the correct choice for most pet owners.

The pre-existing condition rule in pet insurance

Unlike human insurance, which can cover pre-existing conditions with a loading, pet insurance almost universally excludes any condition present before the policy start date — permanently. A dog with a cruciate ligament injury before the policy starts will never have cruciate ligament treatment covered by that policy, regardless of how long you hold it. The practical implication: insure your pet while it is young and healthy.

Wedding insurance — the coverage most couples don't know they need

The average UK wedding in 2025 cost £19,184 according to Hitched.co.uk's annual survey — the single largest one-day expenditure most couples make. Yet fewer than 15% of couples insure it, according to the Wedding Planning Association. The reason most insurers give for the claims they pay is that venues close unexpectedly, suppliers fail, and circumstances beyond the couple's control force cancellation or rearrangement at significant cost.

What wedding insurance covers

- Cancellation and rearrangement for serious illness, bereavement, redundancy, severe weather, or venue failure.

- Venue failure — insolvency, ceasing trading, or cancellation of your booking. The most significant single risk in modern wedding planning.

- Supplier failure — caterer, photographer, florist, band, or car company fails to appear or ceases trading.

- Wedding attire — most policies cover up to £3,000–£5,000 for the dress, with individual limits per item.

- Rings and gifts — loss, theft, or damage before or on the wedding day.

- Personal liability — accidental damage to the venue or injury to a guest caused by the couple or their arrangements.

| Wedding Budget | Basic Cover | Standard Cover | Comprehensive |

|---|---|---|---|

| Up to £7,500 | £35–£55 | £55–£80 | £80–£120 |

| £7,500–£15,000 | £55–£80 | £80–£120 | £120–£175 |

| £15,000–£25,000 | £75–£110 | £110–£165 | £165–£240 |

| £25,000–£50,000 | £110–£165 | £165–£240 | £240–£350 |

When to buy: as soon as the first deposit is paid — not close to the wedding date. Cancellation protection applies from the policy start date. Buying wedding insurance six months before the wedding leaves all deposits paid in the preceding six months unprotected.

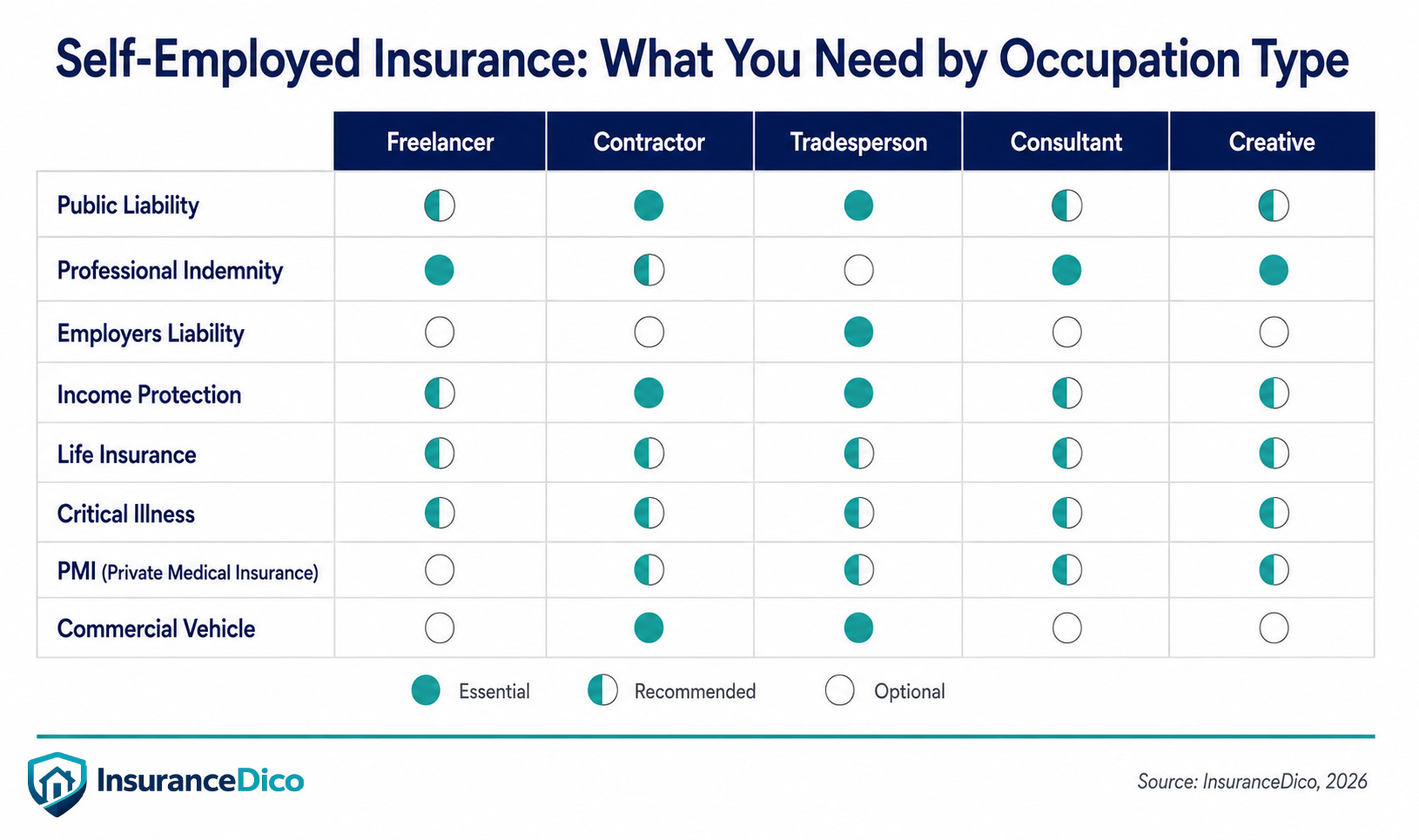

Self-employed insurance — the complete checklist no one gives you

The UK had 4.3 million self-employed workers in 2024 according to ONS labour market statistics. Self-employment removes the safety net that employment provides automatically: statutory sick pay, employer-funded death-in-service cover, employer-arranged pension, and often employer group health insurance. The self-employed insurance gap is not one gap — it is several, each requiring a different product.

Tier 1 — Non-negotiable for client-facing self-employed

Public liability insurance (if you visit clients, work on third-party premises, or have anyone visit your workspace). Contractually required by most clients. Costs £60–£250/year for most professional service providers.

Professional indemnity insurance (if you provide advice, design, code, consult, or deliver professional services of any kind). Required by most contracts and regulated by law for some professions. Costs £120–£600/year depending on coverage limit and profession.

Tier 2 — Essential for financial protection of the individual

Income protection insurance covers 50–70% of income if you cannot work due to illness or injury. Self-employed workers are not entitled to statutory sick pay — without income protection, illness means no income from day one. Costs £30–£120/month depending on age, health, deferred period, and income level.

Life insurance (if you have dependants or a mortgage). Employment does not provide life cover to the self-employed — there is no death-in-service benefit. Costs from £9/month for a healthy 30-year-old with £200,000 coverage.

Tier 3 — Strongly recommended depending on circumstances

Critical illness cover pays a lump sum on diagnosis of serious illness. Especially valuable for the self-employed because the financial consequence of being unable to work extends beyond monthly income to business viability itself. Costs £25–£80/month depending on age, health, and coverage amount.

Private medical insurance — access to faster specialist care is directly relevant to income: a self-employed person waiting 32 weeks for orthopaedic treatment loses 32 weeks of potential billings during that period. PMI reduces this to days. Costs £65–£145/month for a standard policy at age 35–45.

Tier 4 — Occupation-specific

Commercial vehicle insurance (sole traders using a vehicle for work — delivery drivers, tradespeople, mobile service providers). Personal car insurance explicitly excludes business use; failure to declare business use voids a motor claim. Costs £150–£400/year above personal car insurance rates.

Employers liability insurance (if you engage any workers, even informally or temporarily). A sole trader who takes on a labourer for three days is an employer for those three days. EL insurance is legally required from the first day. Costs £120–£300/year for minimal headcount.

Gadget insurance — when it's worth it and when your home insurance already covers it

Gadget insurance is one of the most frequently purchased and least critically evaluated specialist insurance products. Before purchasing a standalone gadget policy, two checks are necessary.

Check 1: Does your home contents insurance already cover the gadget? Standard home contents insurance covers electronics in the home up to the single-item limit (typically £1,500–£2,500). A laptop worth £900 is covered in the home under most contents policies.

Check 2: Does your home insurance personal possessions extension cover it outside the home? A personal possessions extension covers items away from the home — a phone stolen from a café, a laptop damaged at an airport. This extension costs £15–£40/year and covers multiple items under a single extension. If both answers are yes, a standalone gadget policy is duplication.

When standalone gadget insurance makes sense

- You rent and do not have home contents insurance. Without home insurance, there is no contents coverage to extend.

- You own an item that exceeds your contents policy's single-item limit — a professional camera worth £3,500, a high-end laptop worth £2,800.

- You need breakdown and mechanical failure coverage — contents insurance does not cover a phone screen that develops a fault or a battery that fails. Gadget insurance typically covers mechanical breakdown within the first two years.

| Device | Typical Replacement Cost | Gadget Insurance Cost | Breakeven |

|---|---|---|---|

| Flagship smartphone (£800–£1,200) | £800–£1,200 | £8–£15/month | Claim every 5–10 years |

| Mid-range smartphone (£300–£500) | £300–£500 | £5–£8/month | Claim every 4–6 years |

| Laptop (£700–£1,400) | £700–£1,400 | £8–£18/month | Claim every 4–8 years |

| Tablet (£350–£900) | £350–£900 | £5–£12/month | Claim every 4–7 years |

Over-50s financial protection — the products explained honestly

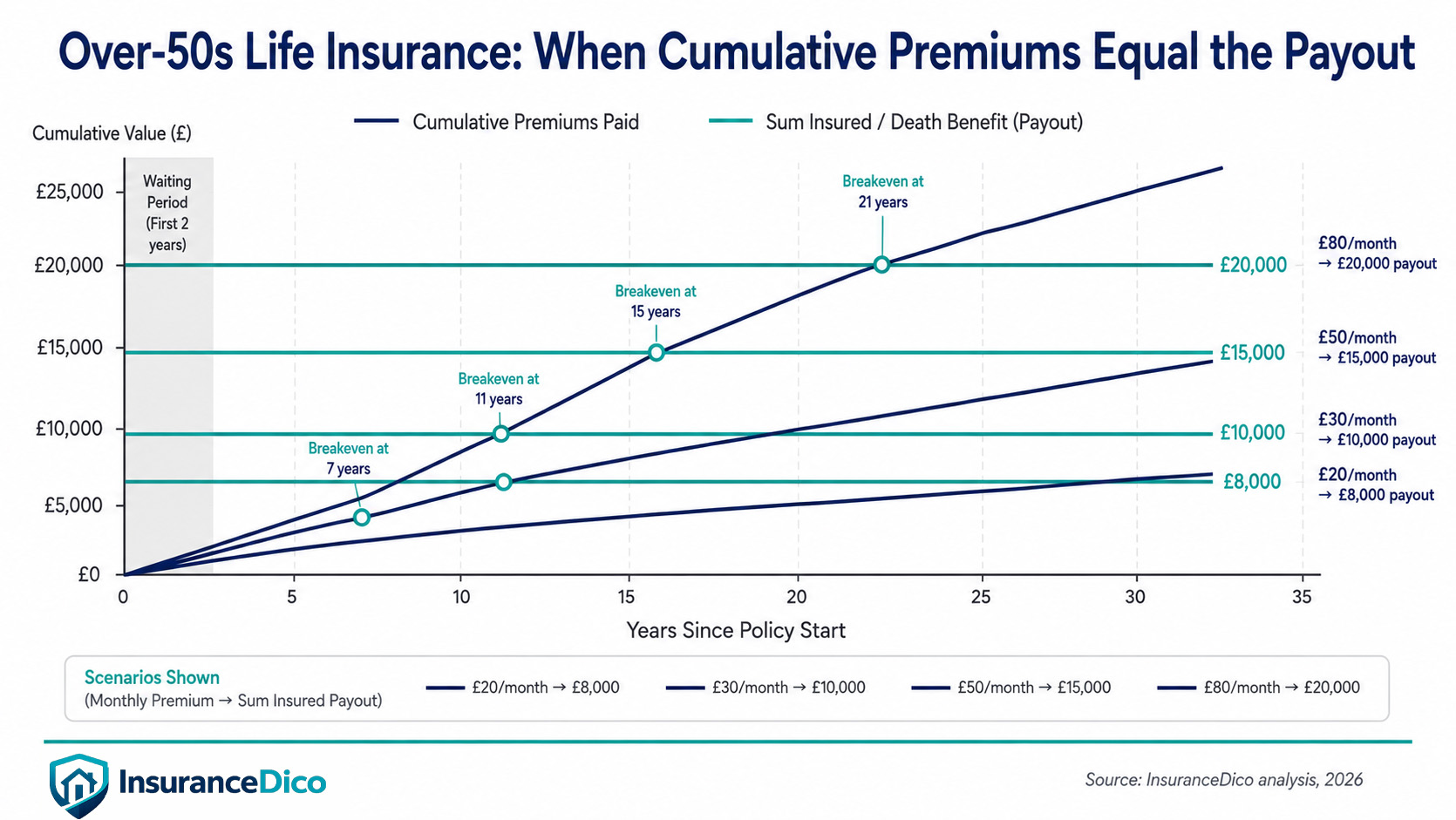

The over-50s insurance market attracts significant advertising spend and generates significant misunderstanding. Over-50s life insurance (also marketed as guaranteed life insurance) accepts applicants aged 50–85 without medical underwriting. A fixed monthly premium buys a fixed lump sum — typically £5,000–£25,000 — paid to beneficiaries on death.

The waiting period most buyers miss: standard over-50s plans include a waiting period of 12–24 months during which the full sum insured is not paid. If you die during the waiting period, premiums paid are returned but the full sum insured is not.

| Monthly Premium | Sum Insured | Months to Break Even | Years After Waiting Period |

|---|---|---|---|

| £20 | £8,000 | 400 months | 31.3 years |

| £30 | £10,000 | 333 months | 26.8 years |

| £50 | £15,000 | 300 months | 23.0 years |

| £80 | £20,000 | 250 months | 18.8 years |

If you take out a plan at 55 and live to 85, you will have paid premiums for 30 years. At £30/month that is £10,800 paid in — equal to a £10,000 death benefit. Over-50s life insurance is not cost-efficient as a savings vehicle. Its value is guaranteed acceptance for people with medical conditions who cannot access standard term life insurance, and for those who want to guarantee a sum for funeral costs without medical underwriting.

Care insurance

Care insurance — covering residential or nursing home fees in old age — is one of the most financially significant unaddressed risks in the UK. The average cost of residential care in England was £35,000 per year in 2024 (Laing Buisson). Average stay is 2.5 years, producing an average total care cost of approximately £87,500. Local authority funding applies only where assets fall below £23,250 in England — above this threshold, individuals self-fund entirely.

Immediate needs annuities pay a guaranteed monthly income for life in exchange for a lump sum, purchased at the point of entering care. Available through specialist providers including Partnership (a Legal & General subsidiary) and Just Group. Pre-funded care insurance is a small market — most products have been withdrawn from the standard market and are now available primarily through specialist financial advisers.

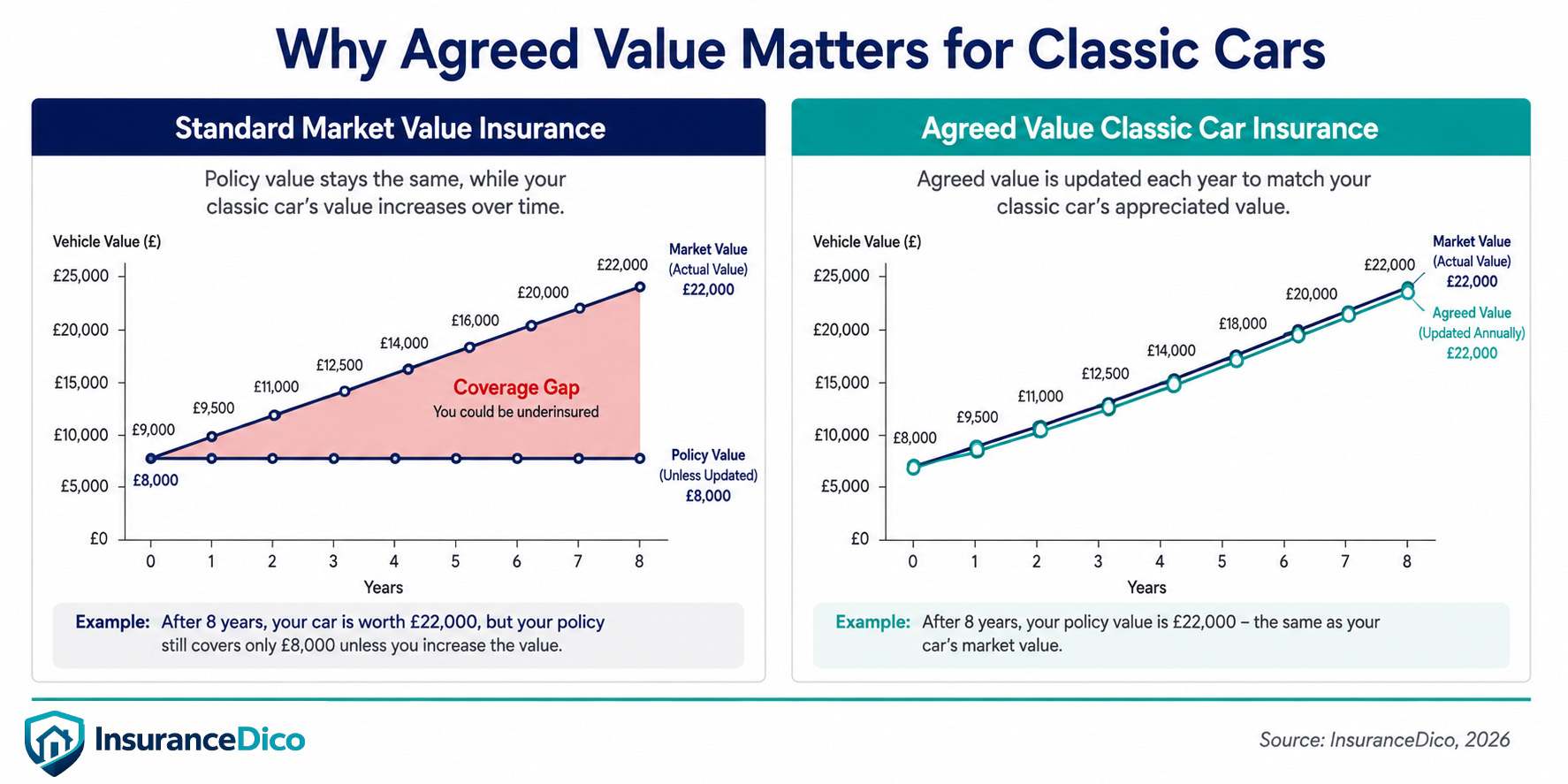

Classic car insurance — why agreed value changes everything

Classic car insurance is distinct from standard motor insurance in one fundamental way: the insurer agrees a fixed payout value with the policyholder at inception — rather than settling at market value at the time of a total loss claim.

Market value settlement (standard motor insurance) pays the market value at the time of the claim. For a depreciating modern vehicle, this is fair. For a classic car that has appreciated over time — a 1973 Porsche 911, a 1968 Ford Mustang — the market value at claim date may be very different from when you purchased the policy.

Agreed value settlement (classic car insurance) fixes a specific value at inception based on a professional valuation, and pays this amount in the event of a total loss. A classic Mini bought for £8,000 in 2018 may be worth £22,000 in 2026 — most classic car insurance policies include agreed value by default and prompt for revaluation at each annual renewal.

Limited mileage policies

Most classic car policies are sold as limited mileage products — restricting annual mileage to 3,000, 5,000, or 7,500 miles per year in exchange for significantly reduced premiums. The reduction reflects lower accident exposure and the profile of the classic car driver: statistically more experienced, more careful, and involved in fewer accidents per mile than the general motoring population. Exceeding the agreed mileage limit is a material change that should be notified to your insurer.

What qualifies as a classic car

- DVLA free road tax eligibility: vehicles manufactured 40+ years ago are exempt from vehicle excise duty — often used as a proxy for "classic".

- Insurer definitions: specialist classic car insurers (Hagerty, Adrian Flux, Footman James, Heritage Insurance) typically apply their own criteria — usually a combination of age (15–30+ years), maintained condition, and limited usage.

- Market reference: classic car valuations are published by Practical Classics, Classic Cars magazine, and auction houses (Bonhams, RM Sotheby's) — the reference for agreed value negotiations with insurers.

Key takeaways

- Specialist insurance UK covers risks outside standard buildings, contents, motor and life — pet, wedding, self-employed, gadget, over-50s and classic vehicles.

- Specialist insurance UK products are governed by category-specific exclusions (pet pre-existing, wedding known circumstance, motor business use) that void claims if ignored.

- Specialist insurance UK pricing is best judged by expected risk transfer — premium versus realistic claim value — not by headline monthly cost.