Professional indemnity insurance covers the legal costs and compensation a business pays if a client claims your professional advice, service, or work caused them financial loss. It is legally required for solicitors, financial advisers, architects, and chartered accountants, and contractually required for most professional service providers working with commercial clients. The average PI claim settled at £13,500 in the UK in 2023. Premiums start at £120 per year for low-risk professionals and reach £2,000+ for businesses with high contract values or prior claims.

Professional indemnity insurance is a UK business policy that pays a client's compensation and your legal defence costs when your professional advice, design, or service is alleged to have caused them financial loss.

What Professional Indemnity Insurance Covers — and Why It Differs From PLI

Professional indemnity insurance is triggered when a client suffers financial loss and attributes that loss to the quality, accuracy, or suitability of your professional work. The claim does not require physical harm to anyone or physical damage to any property — it requires only that the client can argue your professional output fell below the expected standard and cost them money.

The claims that PI responds to:

- An accountant prepares incorrect tax returns, resulting in an HMRC penalty for the client

- A consultant recommends a business strategy that proves commercially damaging

- An IT developer delivers software with a security flaw that leads to a client data breach

- A graphic designer produces a logo that infringes an existing trademark, requiring rebranding costs

- A surveyor misses a structural defect, leading to expensive remediation after purchase

- An architect's plans contain errors that require costly modifications during construction

In each case, the claim is financial — the client lost money because of your work. PI covers the legal cost of defending the claim and any compensation paid.

The distinction from public liability insurance

PLI covers physical harm and physical property damage caused by your presence or activities. PI covers financial harm caused by the quality of your professional output. The boundary in practice:

| Incident | Coverage |

|---|---|

| Architect's design is defective → expensive rework | Professional Indemnity |

| Architect leaves cable on floor → client trips | Public Liability |

| IT consultant's code has a flaw → client loses data | Professional Indemnity |

| IT consultant's laptop charger starts a fire | Public Liability |

| Consultant's advice leads to a poor business decision | Professional Indemnity |

| Consultant's equipment damages client's meeting room | Public Liability |

Most professional service businesses need both. They cover adjacent but genuinely different risks.

Who Is Required to Hold Professional Indemnity Insurance

Legally Mandated PI

The following professions are legally required to hold PI insurance as a condition of their regulatory authorisation:

| Profession | Regulator | Minimum PI Required |

|---|---|---|

| Solicitors (England and Wales) | Solicitors Regulation Authority (SRA) | £2m per claim (sole practitioner) |

| Solicitors (Scotland) | Law Society of Scotland | £2m per claim |

| Financial advisers and IFAs | Financial Conduct Authority (FCA) | £1.2m per claim (FCA minimum) |

| Architects | Architects Registration Board (ARB) | Adequate for the work undertaken |

| Chartered Accountants (ICAEW) | ICAEW | Appropriate to the work |

| Chartered Accountants (ACCA) | ACCA | Minimum defined in regulations |

| Chartered Surveyors (MRICS/FRICS) | RICS | RICS minimum requirements |

| Patent and trade mark attorneys | IPReg | Defined minimum levels |

| Insolvency practitioners | Insolvency Service | Defined per licence |

Contractually Required PI

Beyond the regulated professions, PI is contractually required in most commercial engagements involving professional advice or service delivery:

- Government contracts: Crown Commercial Service frameworks typically require PI at a level proportionate to the contract value

- NHS contracts: NHS Standard Contract requires appropriate PI coverage

- Corporate client contracts: Most FTSE 500 procurement teams include minimum PI requirements in supplier agreements — typically £1m–£5m

- Management consultancy: Major consulting buyers routinely require £5m PI

- Technology contracts: Software development, data processing, and IT services contracts commonly require £1m–£5m PI

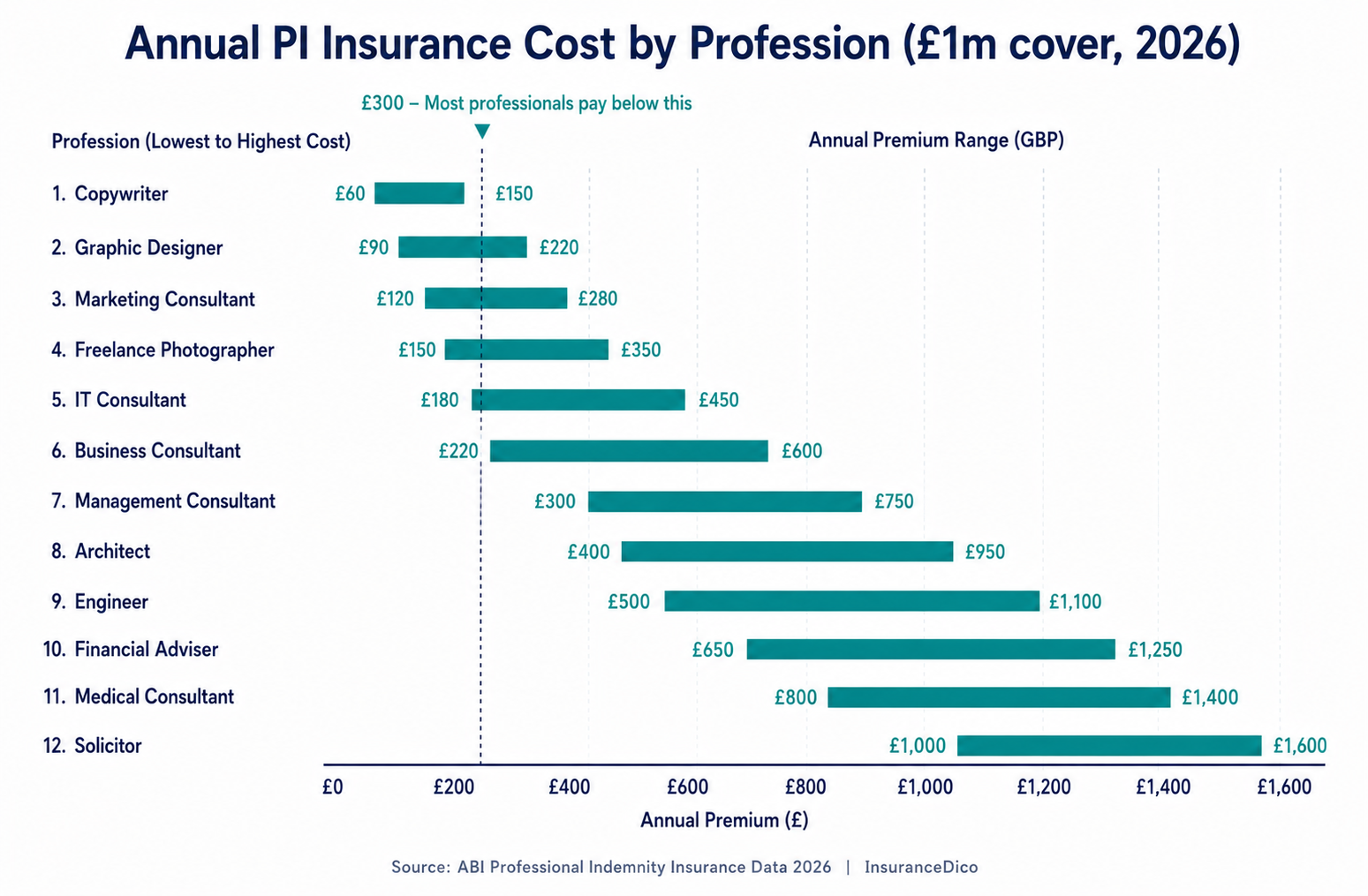

2026 Professional Indemnity Insurance Cost by Profession

PI premiums are calculated on the basis of the maximum financial loss your work could cause a client — not your revenue or your own assets. An adviser managing £500m in client funds faces higher PI exposure than a copywriter producing marketing materials, even if their annual fees are similar.

| Profession / Business Type | £500k Cover | £1m Cover | £2m Cover |

|---|---|---|---|

| Freelance copywriter / content creator | £100–£165 | £140–£225 | £195–£315 |

| Graphic designer / creative | £115–£185 | £158–£255 | £220–£355 |

| Marketing consultant | £130–£215 | £178–£292 | £248–£408 |

| Business coach / trainer | £120–£200 | £165–£272 | £230–£380 |

| HR consultant | £140–£230 | £192–£314 | £268–£438 |

| Management consultant | £200–£350 | £274–£478 | £382–£668 |

| IT contractor / developer | £180–£310 | £246–£424 | £344–£590 |

| Bookkeeper / management accountant | £155–£265 | £212–£362 | £296–£506 |

| Chartered accountant (practice) | £280–£480 | £383–£658 | £534–£918 |

| Solicitor (1–3 partners) | £600–£1,100 | £820–£1,504 | £1,148–£2,108 |

| Architect (sole practitioner) | £350–£650 | £478–£890 | £668–£1,244 |

| Financial adviser / IFA | £450–£800 | £615–£1,094 | £860–£1,530 |

| Recruitment agency | £240–£420 | £328–£574 | £458–£804 |

The loadings that increase premiums above these ranges:

- Prior PI claims — even successfully defended ones — typically produce a 30–80% premium loading

- Contract values materially above the typical range for your profession

- Work in high-litigation sectors — financial services, legal, healthcare

- American or Canadian clients (US litigation risk commands a significant loading)

- Prior regulatory investigations or disciplinary proceedings

How to Calculate the Right Coverage Limit

The correct PI coverage limit is not based on your turnover or your company size. It is based on the maximum financial loss your work could realistically cause a client.

The calculation framework:

Step 1 — Identify your highest-value client engagement. What is the largest contract or project you work on? What are the total fees? What is the client's total financial exposure in that project?

Step 2 — Estimate the worst credible outcome. If your work on that project failed catastrophically — wrong advice, defective deliverable, missed deadline causing cascading commercial damage — what could the total financial consequence be for the client?

Step 3 — Check your contractual minimums. Your largest client contract may specify a minimum PI level. This is your floor, not your ceiling.

Step 4 — Consider defence costs. A contested professional negligence claim in England and Wales can cost £40,000–£150,000 in legal fees to defend. If your PI limit is £500,000 and defence costs are included within it (not in addition), a contested claim could consume 20–30% of your coverage limit before any compensation is considered.

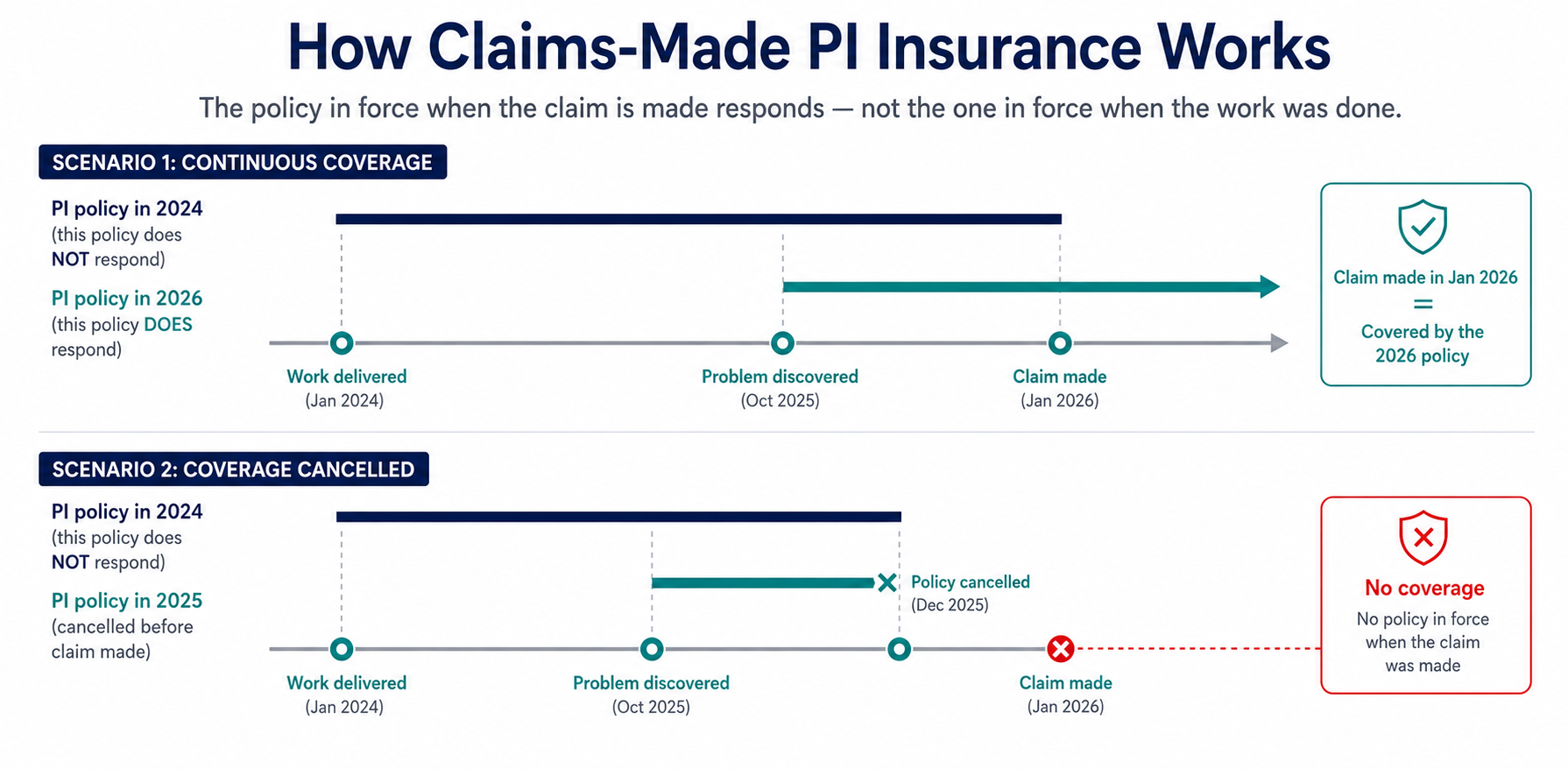

Claims-Made vs Occurrence Basis — the Policy Trigger That Matters

Professional indemnity insurance is almost universally written on a claims-made basis — not on an occurrence basis as most other business insurance is written.

What claims-made means: The policy that responds to a PI claim is the policy in force at the time the claim is made — not at the time the work was done. If you deliver a project in January 2024, the client discovers a problem in October 2025 and makes a claim in January 2026, the PI policy that responds is the one in force in January 2026.

Why this matters: If you cancel your PI policy after completing a project — believing the work is done and the risk is behind you — you have no coverage for a claim made after cancellation relating to that completed work.

Run-off cover: Run-off cover extends PI protection for claims made after a policy is cancelled, typically for two, three, or five years. It is essential for:

- Professionals retiring or closing their practice

- Companies winding down professional services operations

- Sole traders shifting to employment who wish to protect their prior consultancy work

Retroactive date: Your PI policy has a retroactive date — typically the date your first PI policy started. Claims arising from work done before the retroactive date are not covered. When switching PI insurer, confirm the new insurer maintains your original retroactive date — a new retroactive date leaves prior work unprotected.

What PI Does Not Cover — the Boundaries of the Policy

Intentional wrongdoing: PI covers negligent errors — mistakes made in good faith below the expected professional standard. It does not cover deliberate fraud, wilful misconduct, or intentional misrepresentation. Fraud is excluded from PI by all standard policies.

Contractual liability beyond legal duty: PI covers your legal duty of care to clients. If you have accepted contractual terms that impose a higher standard than your legal duty, the excess contractual liability is not automatically covered. Check PI policy wording for contractual liability exclusions before agreeing client terms.

Business disputes: PI is not a substitute for commercial dispute resolution. If a client refuses to pay your invoice, disputes the scope of work, or claims a penalty under contract terms — these are commercial disputes, not professional negligence claims, and PI does not fund their resolution.

Claims by employees: PI covers claims by clients. Employee claims are covered by employers liability insurance.

Bodily injury and property damage: Physical harm to a person or physical damage to property is PLI territory, not PI. Most professional service businesses need both.