Business interruption insurance covers the revenue your business loses and the ongoing fixed costs it cannot avoid when a physical event forces it to close or significantly reduce trading. Standard policies require physical property damage — fire, flood, or structural failure — as the trigger. The COVID-19 test case (FCA v Various Insurers, Supreme Court January 2021) established that certain policy wordings also cover disease-related closure. The indemnity period — how long the policy pays — is the most critical variable in BI insurance and the one most commonly set too low. The average BI claim paid in the UK is £45,000.

Business interruption insurance is a UK commercial policy that pays the gross profit or revenue lost, the ongoing fixed costs, and the increased cost of working a business incurs while an insured event prevents it from trading normally — typically triggered by physical property damage covered under a commercial property policy.

What Business Interruption Insurance Does — and the Gap It Fills

Commercial property insurance pays for the physical reinstatement of your damaged premises — rebuilding a wall, replacing stock destroyed by fire, restoring flooded office space. What it does not pay is the revenue your business loses during the weeks or months that reinstatement takes.

Business interruption insurance fills this gap. While your premises are unoccupied or uninhabitable following an insured event, BI insurance pays:

Gross profit or revenue loss: The difference between your projected trading income during the interruption period and your actual income, up to the maximum indemnity period and the sum insured.

Ongoing fixed costs: Expenses that continue regardless of whether you are trading — rent or mortgage payments, loan repayments, contracted staff salaries, standing utility charges. These costs accumulate while the business cannot earn.

Increased cost of working: Additional costs incurred to maintain trading during the interruption — hiring temporary premises, sourcing stock from a more expensive supplier, paying overtime to compress work into fewer operating hours, or renting equipment to replace damaged items. These additional costs are covered to the extent they reduce the trading loss below the gross profit cover.

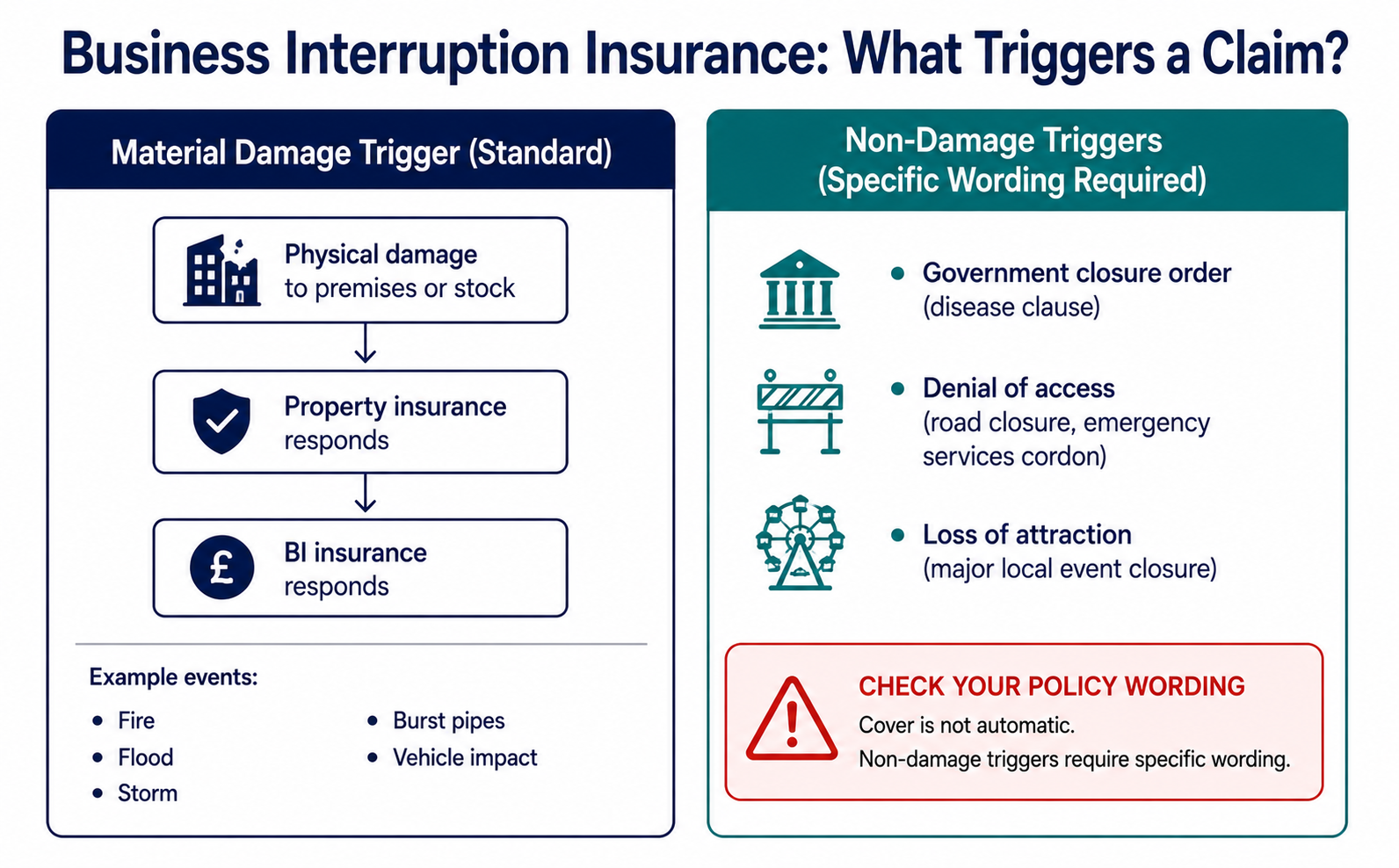

The Trigger — What Starts a BI Claim

Standard Damage-Based Trigger

The standard business interruption policy trigger is material damage to insured property — physical loss or damage to your premises, equipment, or stock that is covered by your commercial property policy. If the property policy responds, the BI policy also responds.

This means: a fire, a flood, a burst pipe, a vehicle impact, a gas explosion. These trigger both the property claim (reinstatement) and the BI claim (lost trading during reinstatement).

The critical link: BI insurance is almost universally purchased as an extension to or alongside a commercial property policy. If you do not hold commercial property insurance, or if the property claim is declined, the BI claim typically cannot be triggered. BI does not stand alone — it stands on top of a valid property claim.

The COVID-19 Lesson — What Non-Damage Triggers Cover

The most significant development in UK business interruption insurance in recent decades was the FCA's test case litigation against multiple UK insurers following COVID-19 business closures in 2020.

The UK Supreme Court ruled in January 2021 that certain policy wordings — specifically those with "disease at the premises" clauses, "denial of access" clauses, and "prevention of access" clauses — did trigger coverage for pandemic-related closure, even without physical property damage.

What this established

- BI policies with specific non-damage triggers (disease, denial of access, loss of attraction) can respond to events without physical property damage

- Policy wording is decisive — two policies from the same insurer at the same price could respond differently to the same event depending on exact wording

- Reading the trigger clause before purchasing is essential, not optional

What post-COVID policies say

Most BI policies issued or renewed after 2021 have been reworded to clarify (and in many cases restrict) non-damage triggers. Pandemic coverage, specifically, has been excluded from most standard BI policies as a named exclusion. Some specialist BI products and captive arrangements maintain pandemic coverage, but they are not standard market products.

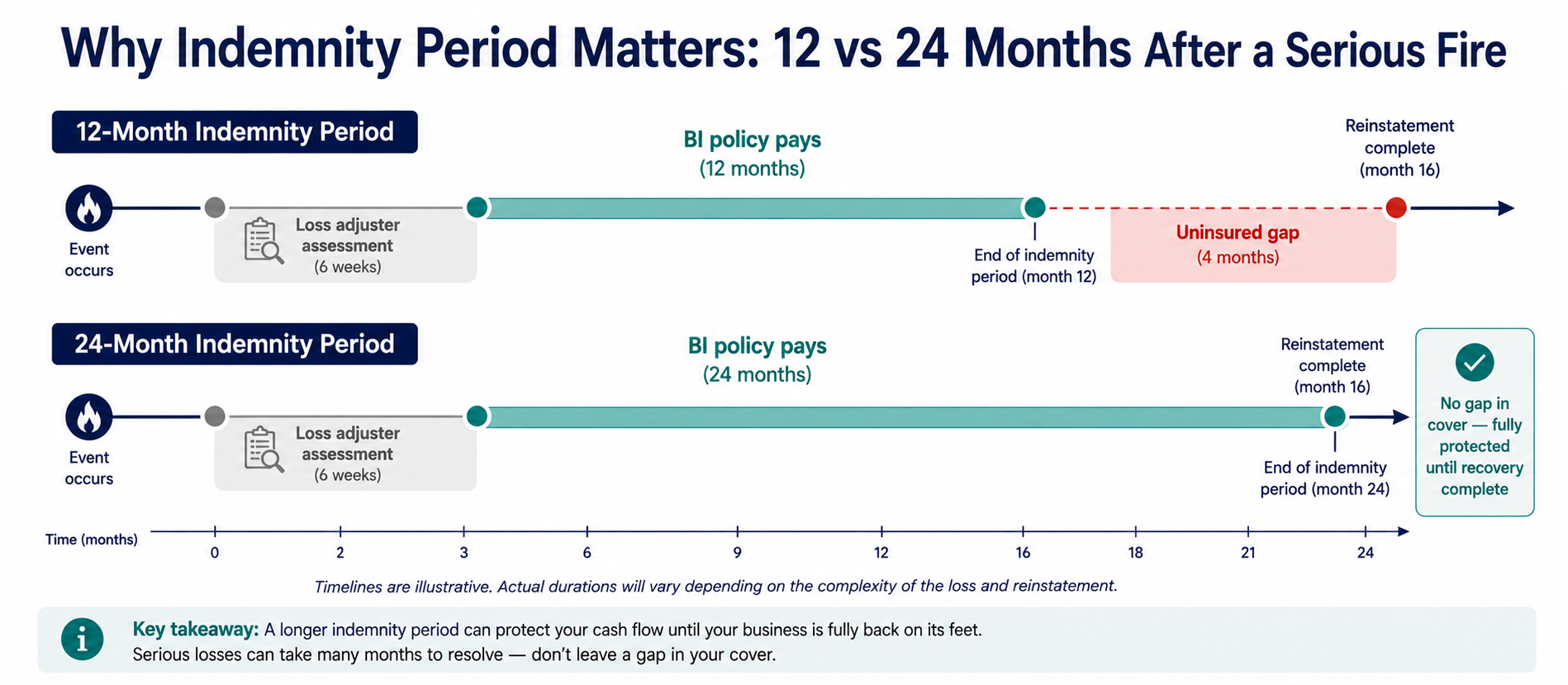

The Indemnity Period — the Variable Most Businesses Set Too Low

The indemnity period is how long your BI policy pays out following an insured event. It is the single most important variable in BI insurance and the one most frequently set incorrectly.

Why Standard 12-Month Policies Are Often Inadequate

A 12-month indemnity period sounds generous. For most serious property losses, it is not:

- A serious fire requiring complete structural reinstatement typically takes 12–18 months from assessment to completion

- Planning permission for any building work adds 8–16 weeks to a standard commercial reinstatement

- A specialist commercial fit-out — restaurant kitchen, dental surgery, manufacturing equipment installation — can add a further 3–6 months after the structure is complete

- Insurance assessment and loss adjuster approval typically begins 4–6 weeks after the event

A business with a 12-month indemnity period that suffers a total structural loss may receive BI payments for only 4–6 months of actual recovery — the period after the property assessment is complete but before reinstatement finishes.

| Property Type | Recommended Minimum Indemnity Period |

|---|---|

| Standard office (leasehold) | 24 months |

| Retail unit with standard fit-out | 24 months |

| Restaurant or hospitality with specialist fit-out | 36 months |

| Manufacturing or industrial premises | 36 months |

| Listed building or specialist commercial | 36–48 months |

| Any property requiring planning permission | 36 months minimum |

How the Sum Insured Is Calculated — and Why It Is Commonly Wrong

BI insurance is typically written on one of two financial bases:

Gross profit basis: Covers the gross profit of the business — turnover minus variable costs (the costs that would not have been incurred had the business not been trading, such as materials and direct labour). Fixed costs continue and are covered within the gross profit figure.

Revenue basis: Covers the total turnover of the business without deducting variable costs. This is simpler to calculate but results in a higher sum insured and therefore a higher premium — appropriate where variable costs are minimal.

The underinsurance problem specific to BI

Unlike commercial property underinsurance (which arises from confusing market value with rebuild cost), BI underinsurance typically arises from:

- Using historic rather than projected figures: Many businesses set their BI sum insured based on last year's accounts. If turnover has grown 25% in the past year, a claim against the prior year's sum insured produces a proportional shortfall.

- Excluding growth projections: If your business has secured new contracts or entered a growth phase, the pre-loss revenue position may significantly understate what you would have earned during the interruption period.

- Forgetting the increased cost of working: Sourcing materials from a more expensive supplier, renting temporary premises at above-market rates, or expediting equipment delivery at premium cost — all of these increased working costs must be factored into the BI sum insured.

How to calculate your BI sum insured correctly:

- Take your projected annual gross profit (for the coming policy year)

- Multiply by the indemnity period in years (e.g. ×2 for a 24-month period)

- Add an estimate of your maximum increased cost of working under a severe interruption scenario

- This total is your BI sum insured

For businesses with variable or seasonal revenue, the calculation should reflect peak trading periods — a retail business closed during its October–December peak generates a BI loss far in excess of its annual average monthly figure.

What Business Interruption Insurance Does Not Cover

No physical damage: Standard BI policies require material property damage as the trigger. A business that loses a major client, faces a key employee resignation, or suffers a reputational crisis without any physical event has no BI claim under a standard policy.

Pandemic (post-COVID policies): As noted, most post-2021 BI policies explicitly exclude pandemic-related closure. This is now a named exclusion, not an ambiguous gap.

Cyber-related interruption without physical damage: A ransomware attack that locks your IT systems and prevents trading is not a BI event under a standard commercial property and BI policy — it requires cyber insurance with a specific cyber business interruption extension.

Trading losses from pre-existing conditions: BI covers the difference between projected and actual trading during the interruption period. If the business was already in decline before the insured event, the insurer calculates the BI loss against the actual trading trajectory, not the fictional scenario of continued strong trading.

Consequential losses from loss of customers: Even with BI insurance, some losses are not recoverable — customers who went to competitors during your closure may not return. BI covers the trading loss during the interruption period. Permanent loss of market share following reinstatement is not covered.

2026 Business Interruption Insurance Cost Indicators

BI insurance is almost always purchased as part of a combined commercial property policy — standalone BI is available but rare. Premium indicators below are for BI coverage as part of a combined commercial property policy.

| Business Type | BI Annual Premium (12-month indemnity) | BI Annual Premium (24-month indemnity) |

|---|---|---|

| Small retail unit (£150k gross profit) | £220–£380 | £310–£530 |

| Office (professional services, £200k GP) | £180–£320 | £252–£448 |

| Restaurant / café (£180k GP) | £280–£490 | £392–£686 |

| Light industrial (£250k GP) | £260–£460 | £364–£644 |

| Wholesale / distribution (£400k GP) | £380–£680 | £532–£952 |