Why Price Comparison Alone Fails for PLI

Price comparison sites perform one function well: they find the lowest headline premium for a defined set of inputs. They perform one function poorly: they distinguish between policies with meaningfully different coverage terms.

The inputs you provide to a comparison site, business type, turnover, coverage limit, excess, determine the price but not the coverage quality. Two insurers who both quote £110 for £2m PLI on a cleaning business may have policies where one covers claims from subcontractors and one does not. One covers work in residential properties above the third floor and one does not. One includes legal defence costs in addition to the coverage limit and one includes them within it, effectively reducing the available compensation by the cost of the defence.

These differences do not appear on the comparison results page. They appear in pages 12–28 of the policy document that you receive after purchasing.

The framework below identifies the specific terms to check before purchase, not after.

The Six-Point PLI Policy Comparison Framework

Point 1, Activity Coverage: Does the Policy Cover What You Actually Do?

Every PLI policy is underwritten on the basis of declared business activities. The activities you declare at application define what the policy covers. Activities you do not declare are activities the policy may not cover.

How to use this in comparison:

Before comparing prices, write down your three highest-risk business activities in specific terms. Not "general building work", but "installation of kitchen units in domestic properties, including cutting of fixed cabinetry and connection of water supply pipework."

Then, for each policy in your shortlist, find the section titled "activities covered" or "business description" and check that your specific activities are included. If the policy description uses generic terms (e.g. "property maintenance"), confirm with the insurer in writing that your specific activities are included.

The most common activity mismatch scenarios:

- A cleaning company that also provides ironing and laundry services, the additional services may not be covered under a policy rated for "commercial cleaning only"

- An IT contractor who visits clients for on-site support, a policy rated for "remote IT consultancy" may exclude on-site visit claims

- A photographer who does drone aerial photography, standard photography PLI typically excludes drone use; a specific drone operator extension is needed

Point 2, Legal Defence Costs: Within or In Addition to the Limit?

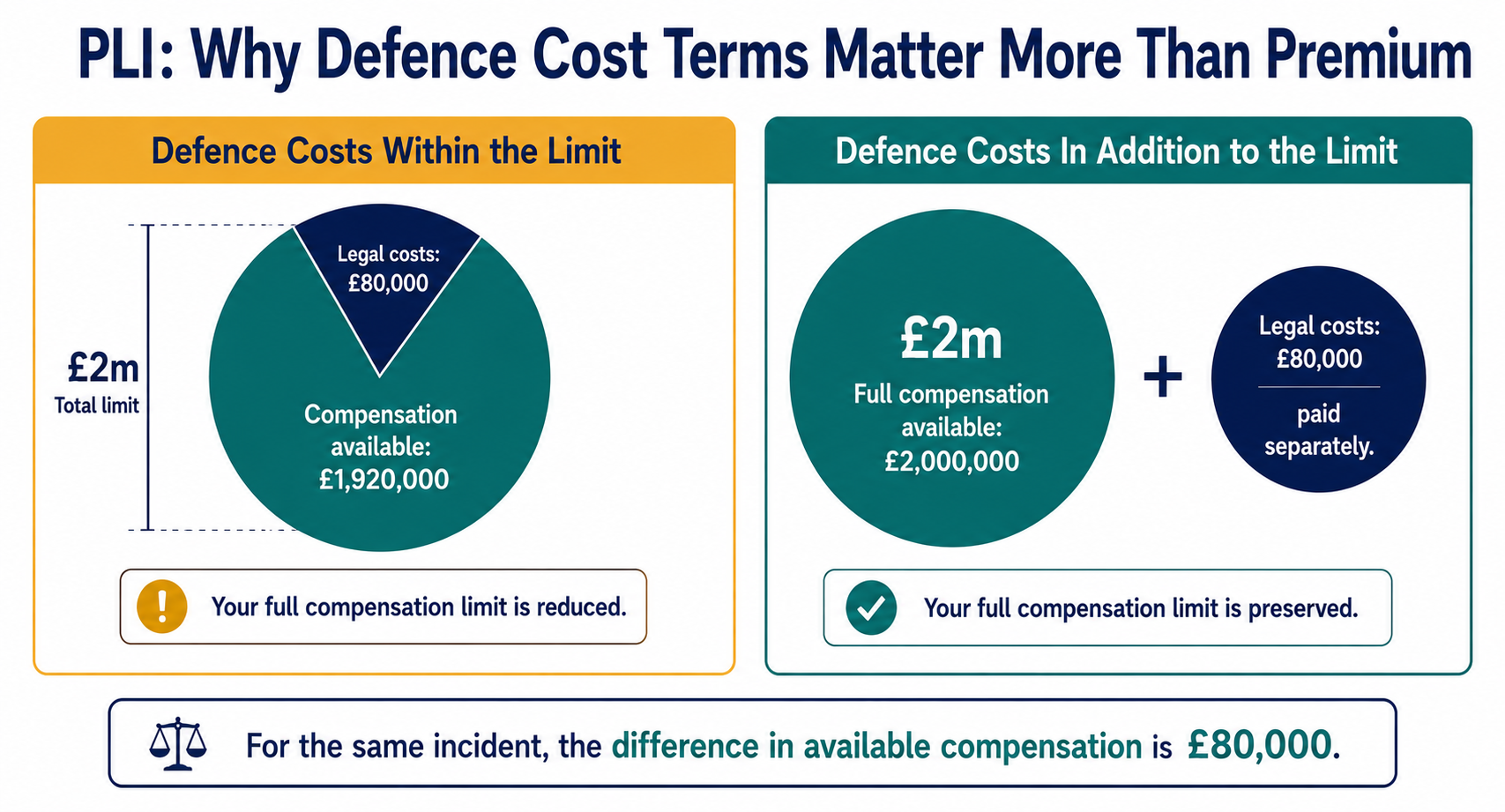

This is the most financially consequential policy term difference and the one most commonly overlooked.

Within the limit: Legal defence costs are deducted from your coverage limit. A £2m policy that includes £300,000 in legal defence costs within the limit effectively has only £1.7m available for compensation after a defended claim.

In addition to the limit: Legal defence costs are paid separately from the coverage limit. Your full £2m is available for compensation, and legal costs are covered on top.

Why this matters in practice:

A complex personal injury claim involving medical evidence, loss of earnings calculations, and specialist expert witnesses can generate £80,000–£250,000 in legal costs before settlement. On a policy with defence costs within the limit, this directly reduces the compensation available. On a policy with defence costs in addition to the limit, it does not.

The premium difference between these two structures is typically modest, often £15–£40 per year for mid-tier policies. The coverage difference can be hundreds of thousands of pounds on a significant claim.

How to identify which structure applies:

Look for the section titled "Legal Costs," "Claimants' Costs," or "Defence Costs" in the policy wording. Language such as "included within the limit of indemnity" indicates within-limit structure. Language such as "in addition to the limit of indemnity" indicates the preferred structure.

Point 3, Exclusions: The Clauses That Determine Claim Outcomes

The exclusions section of a PLI policy determines which claims are not paid. The following exclusions are the most frequently relevant and most commonly differ between policies at the same price point:

- Subcontractor exclusions: Does the policy exclude claims arising from activities of subcontractors engaged by you? Standard language: "This policy does not apply to any liability arising out of the activities of subcontractors." If you engage subcontractors, confirm whether your policy covers principal contractor liability for their activities.

- Height restrictions: Does the policy specify a maximum height above which coverage does not apply? Common thresholds: "above 3 metres from ground level." If your work involves heights, roofing, scaffolding, aerial installation, window cleaning above ground floor, a policy with a height restriction provides no coverage for your most common working environment.

- Care, custody, and control: Standard across all PLI policies, damage to property in your physical possession is excluded. But the boundary differs: some policies define this narrowly (only the specific item you are actively working on), while others define it broadly (any property at your worksite). The breadth of this exclusion can significantly affect tradespeople.

- Gradual pollution: Standard PLI covers sudden accidental pollution events. Gradual or accumulated pollution from your business activities, slow chemical leaching, persistent noise or vibration, is excluded. For businesses handling chemicals or operating machinery near third-party property, this distinction matters.

- Deliberate acts: All PLI policies exclude deliberate harmful acts. The relevant question is how employee misconduct is treated. An employee who acts roughly during work and accidentally causes injury (reckless rather than deliberate) may still be covered. An employee who deliberately damages client property is typically excluded.

Point 4, Insurer Financial Strength

A policy is only as good as the insurer's ability to pay the claim. For routine PLI claims, this is rarely a concern, all FCA-authorised insurers operating in the UK market are subject to Solvency II capital requirements. For very large claims, those approaching the policy limit, the insurer's financial strength becomes a more material consideration.

How to assess financial strength:

- Check the Fitch, Standard & Poor's, or AM Best rating for the insurer. An insurer rated A- or above by Fitch or S&P is considered financially strong. Ratings below BBB warrant attention.

- Policies underwritten at Lloyd's of London carry the Lloyd's A+ financial strength rating and are backed by Lloyd's central fund in addition to the individual syndicate. Lloyd's-backed policies are among the most financially secure in the UK market.

- Unknown or very recently established insurers without published ratings warrant specific due diligence. Very cheap premiums from unrated insurers are a risk signal.

Point 5, Claims Handling: In-House or Third Party?

The quality of claims handling differs between insurers. Some insurers manage claims in-house with dedicated teams who have authority to settle claims within defined limits. Others route claims through third-party claims management companies (CMCs) that operate under contractual incentives that may not align with rapid or generous settlement.

How to identify the approach:

Look for the claims notification section of the policy. If the claims contact is the insurer's own team (named insurer brand + "claims"), the handling is likely in-house. If it routes to a generic claims management company name, it is third-party handled.

Why this matters: A third-party claims handler may have average response times of 5–10 working days for initial acknowledgement. An in-house team at a major insurer typically responds within 24–48 hours. For an incident where a claimant's solicitors are already involved, the response time can affect the insurer's ability to manage the claim before the other party builds a strong evidential position.

Point 6, Renewal Terms: Can the Insurer Decline After a Claim?

Most standard PLI policies can be declined for renewal by the insurer after a significant claim. The insurer is not obligated to renew any policy. For businesses in sectors with higher claim frequency, the ability to renew after a claim is a material consideration.

Guaranteed renewability: Some specialist commercial insurers offer guaranteed renewability as a policy feature, committing to renew the policy at market rates regardless of claims history, subject to continued payment and no fraud. This is worth seeking for businesses with limited alternative market options.

The practical risk without guaranteed renewability: A business with a major PLI claim that cannot renew with the same insurer enters the market as a "claims-affected" risk. Premiums increase materially and some insurers decline to quote. A guaranteed renewal clause avoids this.

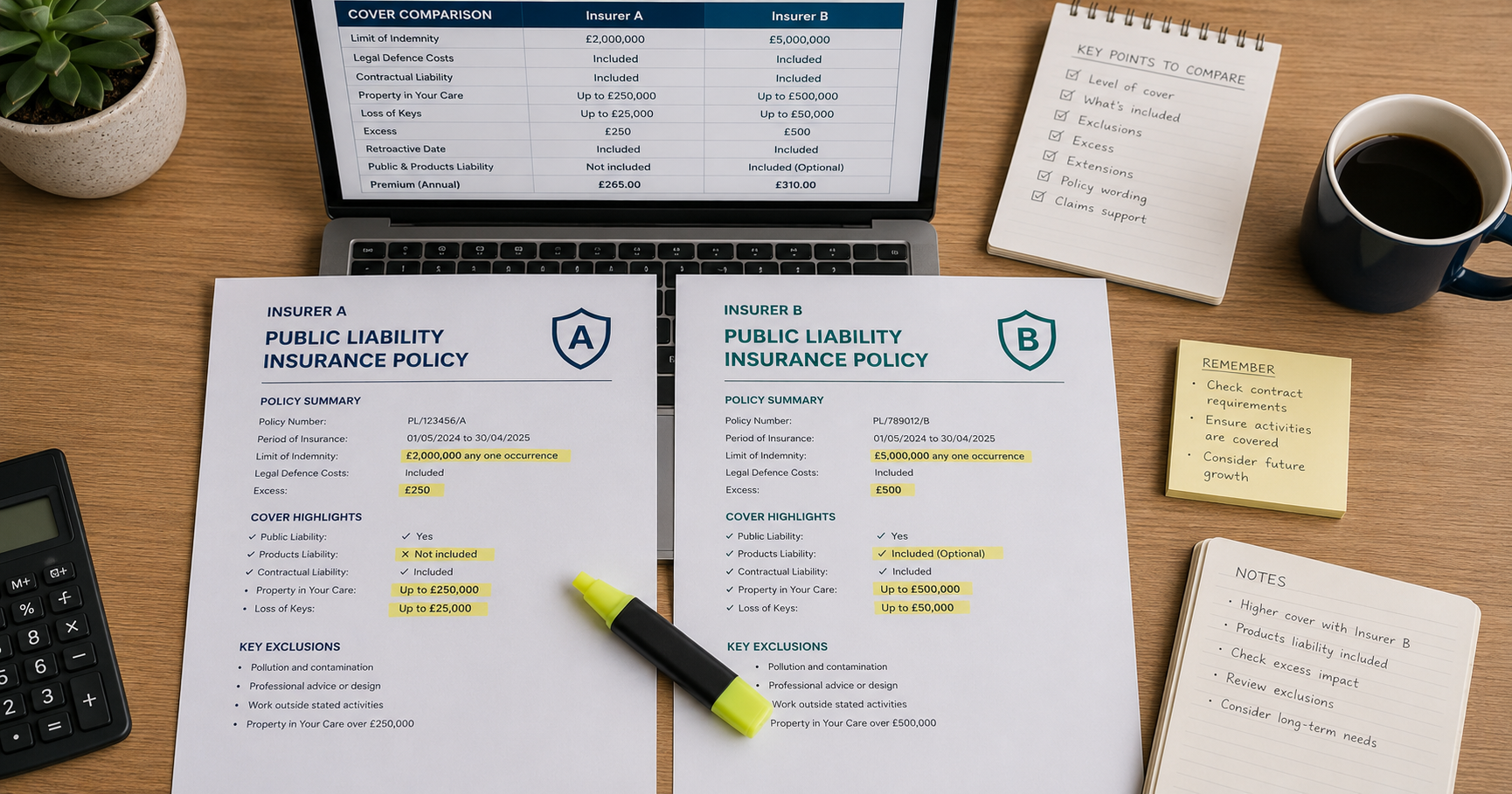

A Worked Example, Two Policies, Same Premium, Different Outcomes

The table below sets out two real-world style policy schedules at almost identical premiums. The headline numbers look similar; the underlying terms do not. This is exactly the kind of comparison a price-only aggregator obscures.

| Cover Comparison | Insurer A | Insurer B |

|---|---|---|

| Limit of Indemnity | £2,000,000 | £5,000,000 |

| Legal Defence Costs | Included | Included |

| Contractual Liability | Included | Included |

| Property in Your Care | Up to £250,000 | Up to £500,000 |

| Loss of Keys | Up to £25,000 | Up to £50,000 |

| Excess | £250 | £500 |

| Retroactive Date | Included | Included |

| Public & Products Liability | Not included | Included (Optional) |

| Premium (Annual) | £265.00 | £310.00 |

For £45 more per year, Insurer B more than doubles the indemnity limit, doubles property-in-care and loss-of-keys sub-limits, and offers an optional products liability extension that Insurer A excludes entirely. The higher excess on Insurer B is the only term that favours the cheaper policy, and it is dwarfed by the cover differences on any claim of meaningful size.

The Provider Comparison, How Major UK PLI Insurers Differ

Premium vs Coverage Quality Trade-offs by Provider Type

Direct online providers (Simply Business, Policy Bee, Quotezone): Fastest to obtain. Price competitive. Most use standard rating engines with limited ability to tailor coverage for unusual activities. Best for straightforward business types with standard activities. Not suitable for unusual trades, high-risk activities, or businesses with prior claims.

Major brand insurers (Hiscox, AXA Business, Aviva Business): Stronger coverage terms, in-house claims handling, and in the case of Hiscox, Lloyd's-backed underwriting. Higher premiums than the cheapest online options but with materially better policy terms for claims involving subcontractors, height work, and complex trades.

Specialist commercial brokers (BIBA-registered): The appropriate route for businesses with prior claims, unusual activities, high-risk trades (demolition, scaffolding, chemical handling), high-value contract requirements (£10m+), or businesses that have been declined by standard market insurers. Specialist brokers access Lloyd's syndicates and non-standard market capacity that is not available through comparison sites.

⚠️ Warning: Headline premium is the wrong anchor. A £120 policy with a £1m limit and a £1,000 excess is more expensive in any real claim than a £180 policy with £5m and a £250 excess. Compare on net exposure, not sticker price.