Commercial property insurance protects your business premises, fixtures, fittings, equipment, and stock against physical loss or damage from events including fire, flood, storm, theft, and subsidence. It is not legally required for most businesses, but mortgage lenders require buildings coverage on any commercial property used as security, and commercial leases frequently make it a tenant obligation. Research by AXA and Zurich consistently shows that over 80% of UK commercial properties are underinsured — typically because rebuild cost is confused with market value.

Commercial property insurance is a UK business policy that pays to repair, rebuild, or replace your trading premises, fixtures, fittings, stock, and contents following physical loss or damage from an insured event.

What Commercial Property Insurance Covers

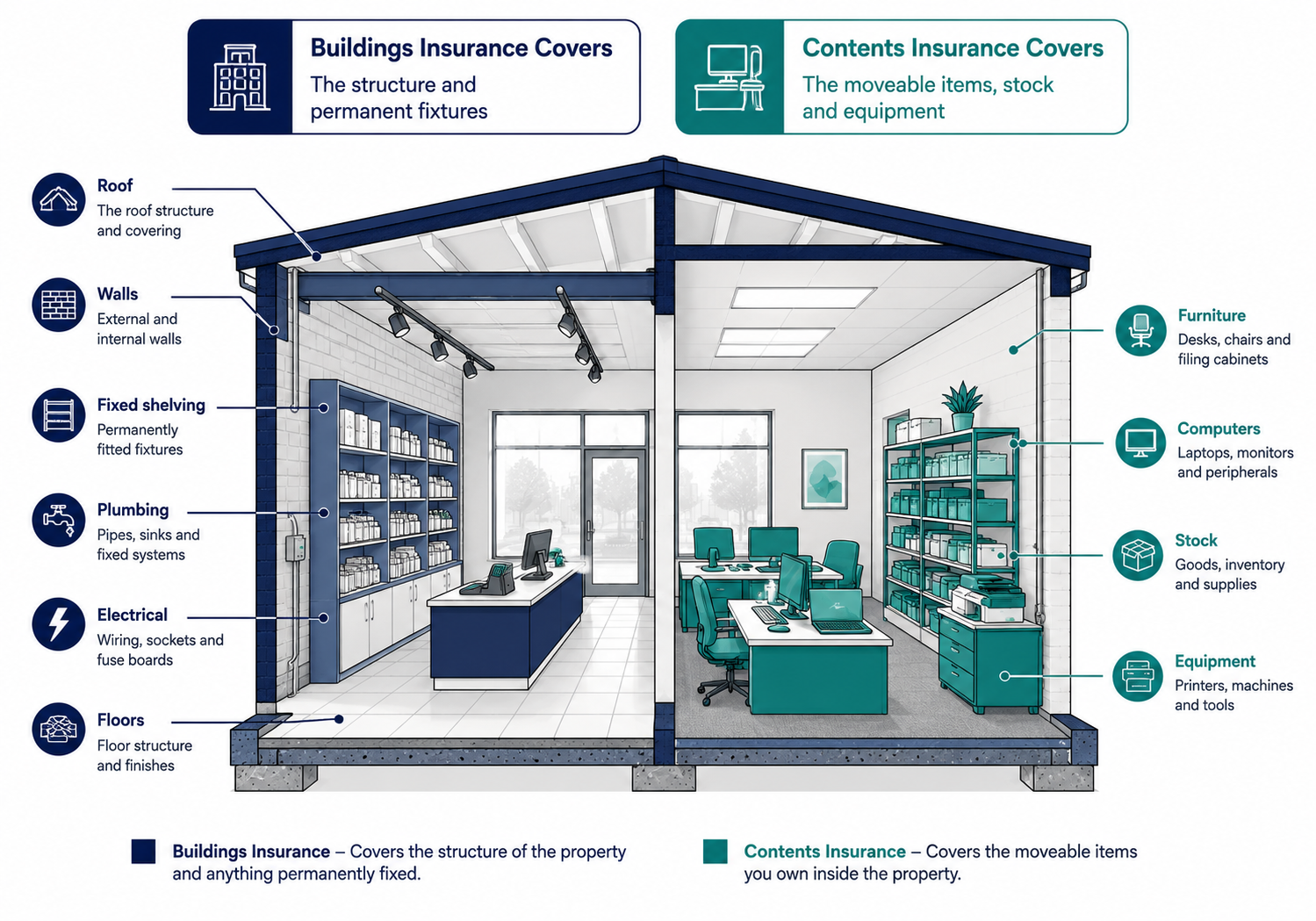

Commercial property insurance operates across two distinct coverage areas — the building itself and its contents — which can be purchased separately or combined into a single policy.

Buildings Coverage

Buildings insurance covers the physical structure of your commercial premises: walls, roof, floors, fixed installations, and permanently attached fixtures. For commercial property this extends to shop fronts and display windows, signs and awnings fixed to the exterior, car parks and perimeter fencing, built-in counters and shelving, plumbing, electrical installations, and heating and ventilation systems.

Covered events under a standard commercial buildings policy:

- Fire, explosion, and lightning strike

- Storm and flood damage

- Escape of water from burst pipes, overflowing tanks, or leaking appliances

- Subsidence and ground heave

- Theft and malicious damage

- Impact from vehicles, falling trees, or aircraft

- Riot and civil commotion

Contents Coverage

Contents insurance covers moveable business assets — anything that is not permanently fixed to the structure. For a commercial business this includes office furniture and equipment, computers and IT hardware, stock and raw materials, trade tools and portable equipment, business money on the premises (up to a sub-limit), and tenant's fixtures and fittings in leased premises.

The Critical Boundary for Tenants

If you lease your commercial premises, the lease terms determine responsibility for buildings insurance. Under most commercial leases:

- The landlord insures the building structure

- You insure your own contents, stock, and trade fittings

- Some leases require you to reimburse the landlord for a proportion of the buildings insurance premium via service charge

Always read the insurance clause in your commercial lease before arranging property insurance. Duplicating the landlord's buildings cover wastes premium. Failing to hold the required contents cover breaches the lease terms.

The Underinsurance Problem — Why 80% of UK Commercial Properties Are Exposed

Commercial property underinsurance is endemic in the UK market. Research from both Zurich Commercial and AXA Business Insurance has consistently found that more than 80% of UK commercial properties carry insufficient insurance — with the average insured sum representing only 65–70% of true rebuild cost.

Why Rebuild Cost and Market Value Are Not the Same

Market value is what you could sell or let the property for. It includes the land value, the location premium, and market supply and demand.

Rebuild cost is the cost of demolishing the existing structure and reconstructing it to the same specification — including demolition, site clearance, labour, materials, architects' fees, structural engineering, planning permission, and Building Regulations compliance.

For commercial properties, these two figures diverge significantly:

| Property Type | Typical Market Value | Typical Rebuild Cost |

|---|---|---|

| Retail unit, secondary high street | £180,000 | £220,000–£280,000 |

| Office suite, regional town | £320,000 | £280,000–£360,000 |

| Industrial unit, 5,000 sq ft | £450,000 | £380,000–£520,000 |

| Restaurant premises with fit-out | £280,000 | £350,000–£480,000 |

| Specialist manufacturing facility | £800,000 | £900,000–£1,400,000 |

The average clause consequence: When a commercial property is underinsured, insurers apply an average clause at the point of any claim — including partial claims. If your property is insured at 70% of its true rebuild cost, every claim is settled at 70% of its value. A burst pipe causing £35,000 in damage would be settled at £24,500. The remaining £10,500 is your uninsured loss.

2026 Commercial Property Insurance Costs

Commercial property insurance premiums are calculated on: the property rebuild cost (for buildings), the total insured value of contents and stock, the property use and sector, the property's location and risk factors (flood zone, crime rate, subsidence area), and the claims history.

Indicative 2026 Annual Premium Ranges

| Property Type / Use | Annual Premium (Buildings Only) | Annual Premium (Combined) |

|---|---|---|

| Small office suite (up to £500k rebuild) | £420–£780 | £580–£1,100 |

| Retail unit with stock (£300k rebuild, £100k stock) | £520–£950 | £720–£1,380 |

| Restaurant / café (£400k rebuild, specialist fit-out) | £680–£1,350 | £950–£1,950 |

| Light industrial / workshop (£600k rebuild) | £560–£1,050 | £760–£1,450 |

| Warehouse (£1m rebuild, £200k stock) | £880–£1,680 | £1,200–£2,380 |

| Pub / licensed premises | £750–£1,500 | £1,050–£2,150 |

What Significantly Increases Commercial Property Premiums

Flood zone location: Properties in Environment Agency flood risk zones attract material premium loadings. Under the Flood Re scheme for residential properties, flood risk is pooled. No equivalent scheme exists for commercial properties — commercial flood insurance is individually underwritten, and for high-risk locations the premium can be prohibitive. Consider FloodFlash parametric flood insurance as an alternative for high-risk commercial sites.

Listed building status: Grade I and Grade II listed commercial buildings require like-for-like reinstatement using period-appropriate materials under planning law. Rebuilding a listed Georgian townhouse commercial premises using modern materials is not permitted. Rebuild costs are substantially higher than equivalent unlisted properties, and some standard insurers exclude or limit coverage for listed buildings. Specialist brokers with Lloyd's market access are the appropriate route.

High-risk stock: Businesses storing flammable materials, hazardous chemicals, or high-theft items (electronics, pharmaceuticals, luxury goods) face material loading on contents premiums — and may require specialist coverage outside the standard commercial property market.

The Add-Ons Worth Including in a Commercial Property Policy

Business interruption extension: Standard commercial property insurance covers the repair or replacement of physical property. It does not cover the revenue your business loses while premises are uninhabitable or while the rebuild takes place. Business interruption insurance covers this gap — and is typically sold as a package with commercial property coverage.

Engineering and machinery breakdown: Standard property insurance covers external physical damage. Internal mechanical or electrical breakdown of plant, machinery, boilers, and HVAC systems requires a separate engineering inspection and breakdown policy. For manufacturing businesses and hospitality businesses dependent on refrigeration or cooking equipment, this is a critical gap if not included.

Terrorism: Standard commercial property policies exclude damage caused by terrorism under Pool Re legislation (Pool Reinsurance Company Ltd). If your premises are in a location assessed as higher terrorism risk — city centres, major infrastructure adjacent locations, iconic districts — terrorism coverage is available as an add-on through Pool Re-backed policies at modest cost.

Goods in transit: Stock and equipment that leaves your premises — deliveries, samples in a sales vehicle, equipment taken to client sites — is not covered by commercial property insurance while away from the insured location. Goods in transit insurance covers this gap.

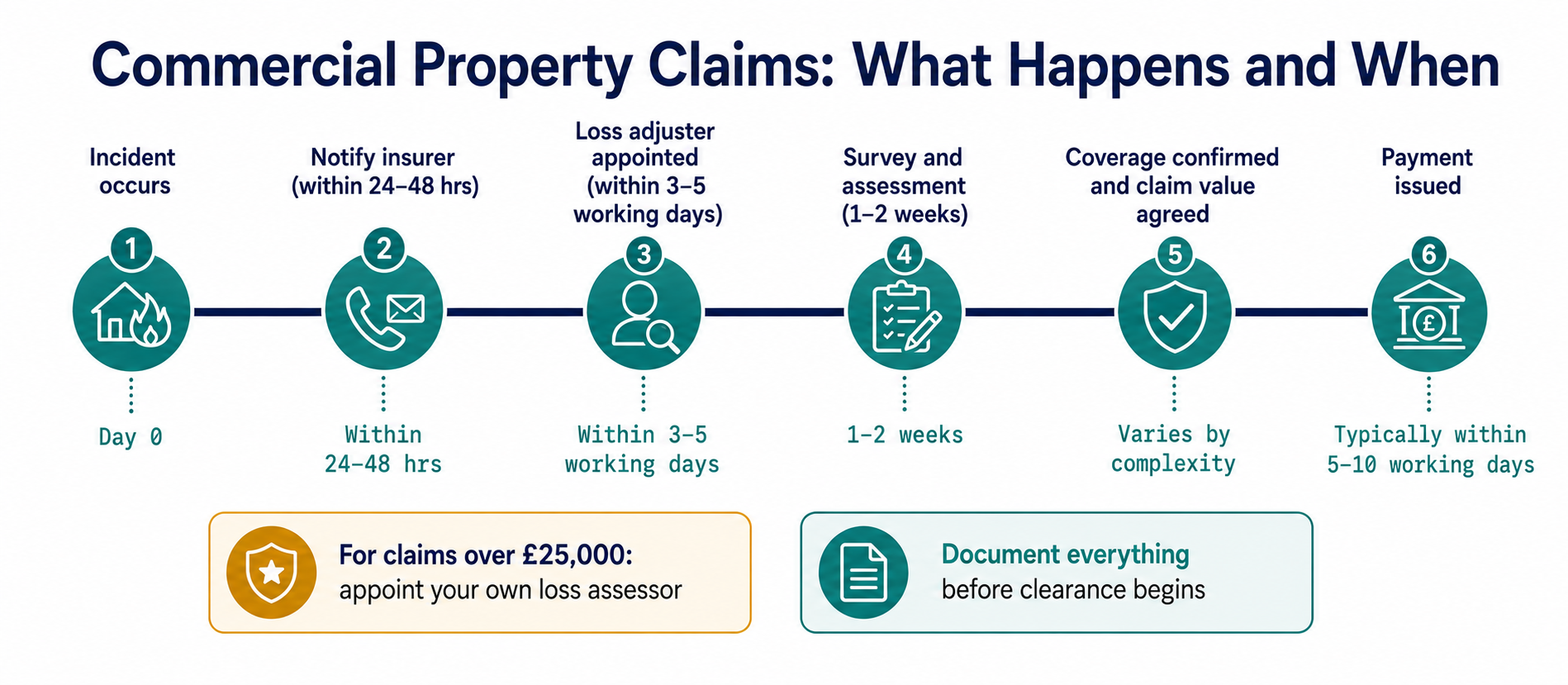

How to Claim on Commercial Property Insurance

Document before clearing: After any property damage event, photograph everything before any clearance, repair, or reinstatement work begins. The photographic and video record of the damage as found is the primary evidence base for the claim. Loss adjusters appointed by the insurer will visit, but their visit may be days after the incident — document independently before then.

Notify immediately: Most commercial property policies require notification "as soon as reasonably practicable" — in practice, within 24–48 hours of discovering the damage. For major losses — fire, flood, serious structural damage — call your broker or insurer before making any reinstatement decisions.

The loss adjuster's role: For claims above approximately £5,000–£10,000, insurers appoint a loss adjuster to assess the damage, establish coverage, and agree the claim value. The loss adjuster works for the insurer — they are qualified but not your advocate. For large or complex claims, appointing your own loss assessor (who works for you, not the insurer) is worth considering.

Mitigation obligation: You are obliged to take reasonable steps to prevent further loss after an insured event — boarding broken windows, drying out water damage, securing the premises against further theft. Mitigation costs are covered. Failure to mitigate gives the insurer grounds to reduce the claim settlement.