Employers liability insurance is legally required for every UK business with one or more employees under the Employers Liability (Compulsory Insurance) Act 1969. The minimum coverage is £5m per claim. The penalty for operating without valid EL insurance is £2,500 per day. The requirement extends beyond permanent employees to include temporary workers, agency workers placed at your premises, apprentices, work experience participants, and — in some circumstances — self-employed contractors working under your supervision. Failure to display the EL certificate carries a separate £1,000 fine.

Employers liability insurance is a UK business policy, compulsory under the Employers Liability (Compulsory Insurance) Act 1969, that pays compensation and legal defence costs when an employee suffers injury, illness, or death caused by their work for you.

The Legal Framework — Exactly What the Law Requires

The Employers Liability (Compulsory Insurance) Act 1969 is the statute that makes EL insurance a legal requirement. It applies to virtually all UK employers and is enforced by the Health and Safety Executive (HSE).

The Act requires:

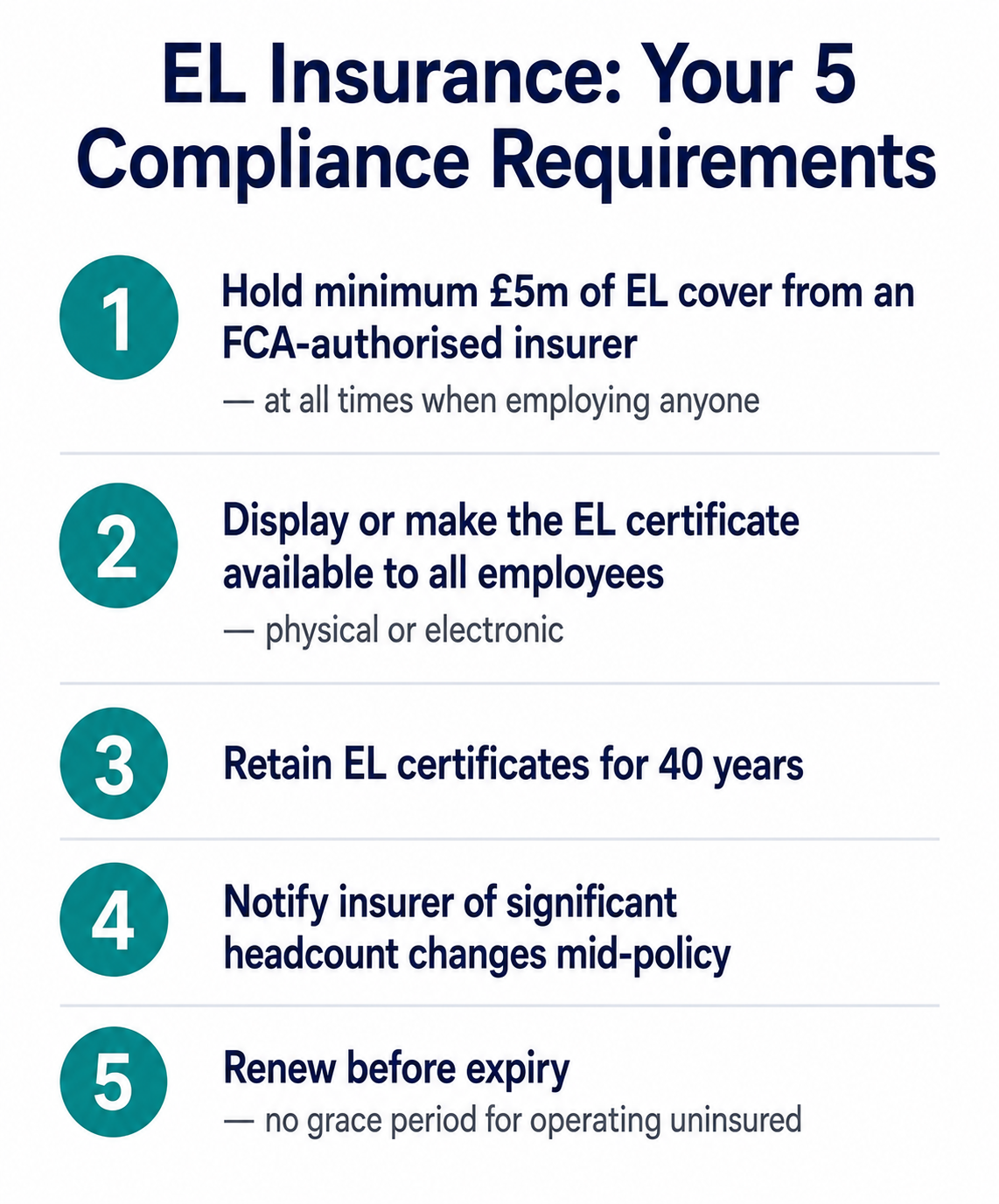

- A minimum of £5m of employers liability coverage per claim

- Coverage from an FCA-authorised insurer

- A valid certificate of insurance at all times when employing anyone who falls within the Act's definition of "employee"

The Employers Liability (Compulsory Insurance) Regulations 1998 add the requirement to display or make available the certificate of insurance to employees. Failure to display the certificate carries a £1,000 fine per day.

The penalties for non-compliance:

| Offence | Penalty |

|---|---|

| Operating without valid EL insurance | £2,500 per day |

| Failing to display or make EL certificate available | £1,000 per day |

| Providing false information about EL insurance | Up to unlimited fine |

These are not administrative charges. They are fines issued by the HSE under powers granted by the 1969 Act. The HSE conducts enforcement visits and may investigate following any workplace injury report, whether or not a claim is subsequently made.

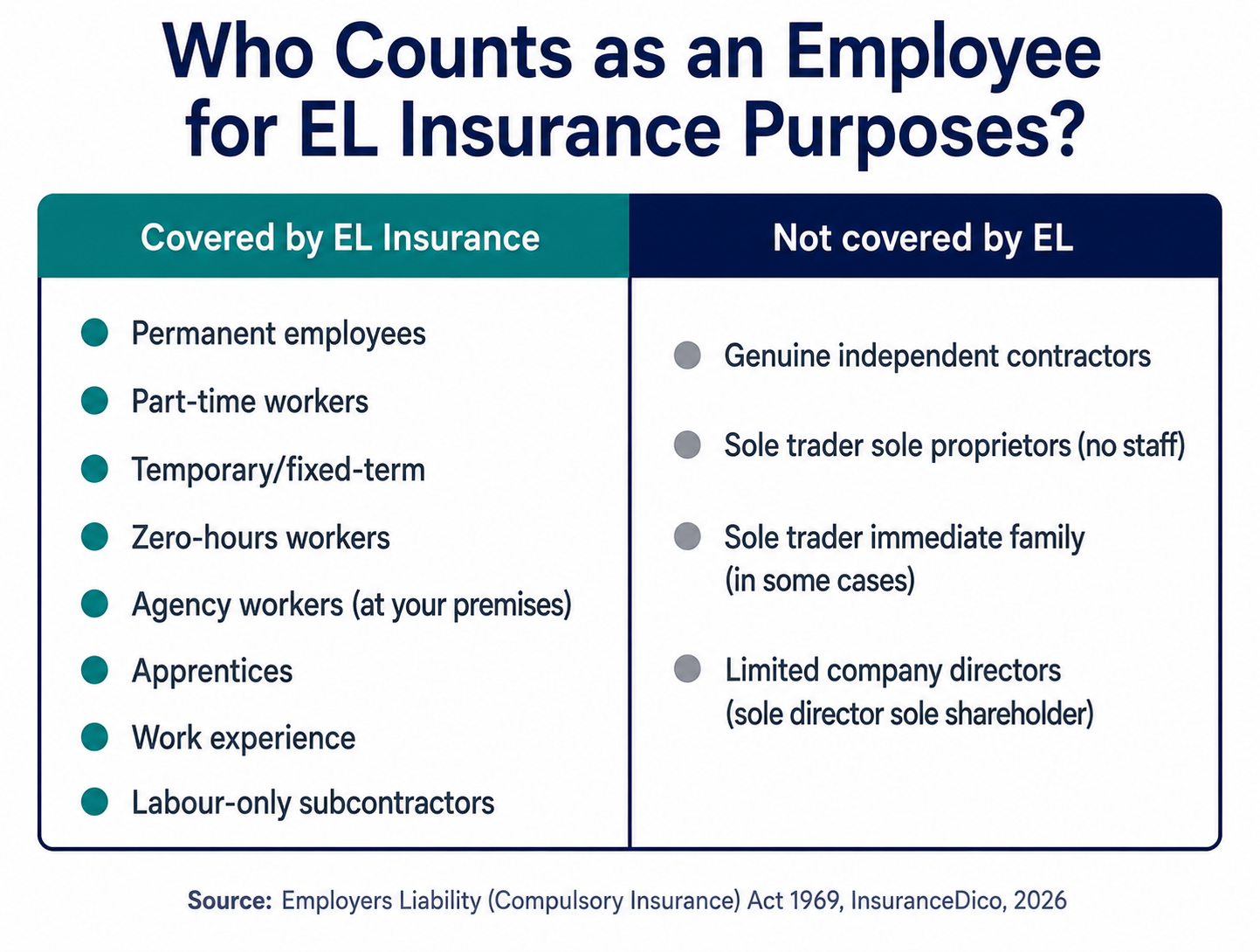

Who Counts as an "Employee" Under the Act — the Wider Definition

The most common source of EL compliance gaps is the assumption that "employees" means only permanent, salaried staff. The legal definition is considerably broader.

Included as employees for EL purposes:

Permanent employees — full-time and part-time staff on your payroll, regardless of hours worked.

Temporary workers — employees on fixed-term contracts, seasonal workers, and zero-hours contract workers engaged directly by your business.

Agency workers placed at your premises — where an employment agency supplies workers who operate under your day-to-day supervision and control, they are typically treated as your employees for EL purposes. Check the agency contract to confirm responsibility allocation.

Apprentices — all apprentices working under your supervision, including those on government apprenticeship schemes, are employees for EL purposes.

Work experience participants — school, college, and university work experience placements under your supervision and direction are employees for EL purposes for the duration of the placement.

Labour-only subcontractors (LOSCs) — a self-employed person who provides only their own labour (no materials, no equipment, no independent business structure) and works exclusively under your direction at your site may be classified as an employee for EL purposes regardless of how they are paid or what they call themselves.

Volunteers — in some circumstances, particularly in regulated care sectors, volunteers working under direct organisational supervision may be employees for EL purposes. Charities and care organisations should seek specific advice.

Not included:

- Genuinely independent contractors who supply their own tools, set their own methods, work for multiple clients, and bear their own commercial risk are not employees for EL purposes — but they should hold their own EL insurance if they have staff themselves

- Immediate family members of a sole trader or partnership in a non-limited business may be exempt — verify the specific criteria with your insurer

How Much Does Employers Liability Insurance Cost in 2026?

EL insurance premiums are calculated primarily on payroll — the total annual wage cost of your covered workforce — and the risk classification of your industry.

The payroll basis: Most EL insurers rate premiums per £100 of annual payroll. A cleaning business with £80,000 annual payroll in a moderate-risk sector might pay a rate of £0.65 per £100 of payroll — producing an annual premium of £520.

2026 EL premium indicators by sector

| Sector | Risk Classification | Approximate Annual Premium |

|---|---|---|

| Professional office services | Low | £180–£320 |

| Retail (non-food) | Low-medium | £250–£420 |

| Domestic cleaning | Medium | £310–£520 |

| Catering and hospitality | Medium | £350–£580 |

| Light manufacturing | Medium-high | £420–£700 |

| Construction (general) | High | £580–£980 |

| Roofing and demolition | Very high | £850–£1,600 |

| Care sector | Medium-high | £480–£820 |

Factors that reduce your EL premium:

Claims-free history: A five-year claims-free record earns meaningful discounts at renewal — typically 20–35% below base rates. EL is a long-tail class — claims can arise from illnesses that manifest years after the exposure. Good claims management and occupational health practices reduce the claims pool from which premiums are derived.

Documented health and safety management: Insurers weigh your health and safety management systems when pricing EL. A business with a documented risk assessment process, regular toolbox talks, PPE provision records, and a dedicated health and safety officer presents a demonstrably lower risk than one with none of these. Provide this documentation proactively at renewal.

Rehabilitation and return-to-work programmes: Insurers in the EL market have moved toward partnership with employers on early rehabilitation of injured workers. Businesses with structured return-to-work programmes have lower average EL claim costs and attract premium discounts at renewal.

What Employers Liability Insurance Covers

EL insurance responds when an employee makes a claim that they suffered injury, illness, or death as a result of their employment with you. The policy covers:

Legal defence costs: The cost of defending the claim, appointing specialist solicitors, expert witnesses, and any tribunal or court appearances.

Compensation awards: Any compensation ordered by a court or agreed in settlement — including damages for pain and suffering, loss of earnings, future care costs, and any provisional damages award for progressive conditions.

Regulatory investigation costs: Where an HSE investigation follows a workplace accident, some EL policies cover the cost of legal representation during the investigation.

What EL does not cover:

EL covers employees only. Third-party claims — customers, visitors, the public — require public liability insurance. Financial loss from professional errors requires professional indemnity insurance. Fines and penalties imposed by regulators (the £2,500 per day fine for operating without EL, for example) are specifically excluded from all EL policies — these are criminal penalties and no insurance covers them.

The EL Certificate — Display and Retention Requirements

Display requirement: Under the Employers Liability (Compulsory Insurance) Regulations 1998, the EL certificate must be displayed where employees can easily read it. For businesses with a single premises, a noticeboard display is the standard approach. For businesses with multiple sites, the certificate must be displayed at each location.

Electronic display: Regulations were updated to permit electronic display — the certificate can be made accessible to all employees via an intranet, company portal, or employee app rather than physical display. The requirement is accessibility to all employees, not a physical poster.

Retention requirement: You are required to retain EL certificates for 40 years. This unusual retention period exists because EL claims for occupational diseases — asbestosis, vibration white finger, noise-induced hearing loss — can arise decades after the exposure. If an employee makes a claim in 2040 for an illness contracted while working for you in 2026, you will need to produce the 2026 insurance certificate to establish coverage.

Common EL Compliance Failures — and How to Avoid Them

Failure 1 — Allowing EL to lapse between policy years: The most common compliance failure is a gap in EL coverage at renewal — either because the renewal was missed, the premium was not paid in time, or the insurer took time to issue the new certificate. Set your renewal reminder 30 days before expiry. Confirm the new certificate is in hand before the old one expires.

Failure 2 — Not updating headcount mid-policy: If your business doubles in size during the policy year — bringing on new employees, seasonal workers, or a significant number of agency workers — failing to notify the insurer is a material change. In a claim, insurers can reduce settlements proportionally if the declared headcount significantly understates the actual insured population.

Failure 3 — Assuming independent contractors do not trigger EL: As noted above, the employment status test for EL is broader than the commercial or tax definition of "employed." If you engage workers on a self-employed basis who work exclusively under your direction, they may be employees for EL purposes. If in doubt, carry EL insurance — the marginal cost of unnecessary EL coverage is far lower than the consequence of an uninsured employee claim.

Failure 4 — Failing to display the certificate: The £1,000 per day fine for failure to display or make the certificate available is rarely discussed but is a real HSE enforcement tool. Ensure the current year's certificate is accessible to all employees — whether physically or electronically.