Car insurance is a legal requirement in the UK under the Road Traffic Act 1988 — driving or keeping a vehicle on a public road without it is a criminal offence carrying an unlimited fine, six penalty points, and potential vehicle seizure. The average UK car insurance premium reached £635 per year in Q1 2026 (ABI data) — up 8% year-on-year, following a 21% rise in 2023. The most important levers you have over your premium are your no-claims bonus, your voluntary excess, and your vehicle choice. Young drivers (17–24) pay an average of £1,100 per year — black box policies typically cut this by 20–30%.

Car insurance UK is a regulated motor insurance product mandated by the Road Traffic Act 1988, available at three statutory cover levels — third party only, third party fire and theft, and comprehensive — and recorded centrally on the Motor Insurance Database.

The legal requirement — what UK law actually says

Motor insurance is one of only two insurance products that UK law makes universally compulsory (the other is employers' liability for businesses with staff). Under the Road Traffic Act 1988, it is illegal to use or keep a motor vehicle on a public road in the UK without at minimum third party insurance in force.

The penalties for driving uninsured are not administrative. They are criminal — and they apply whether or not you were aware your cover had lapsed.

| Penalty | Detail |

|---|---|

| Fixed penalty | £300 fixed penalty notice |

| Court conviction | Unlimited fine at magistrates' court |

| Penalty points | 6–8 points on your licence |

| Vehicle seizure | Police can seize your vehicle on the spot |

| Vehicle destruction | If uninsured and unclaimed, the vehicle can be crushed |

| Driving ban | Court discretion — particularly for repeat offences |

The Continuous Insurance Enforcement (CIE) system cross-references the DVLA vehicle registration database with the Motor Insurance Database (MID) — a central record of all insured vehicles in the UK. If your vehicle appears in DVLA records but not MID, the DVLA sends an Unlicensed Vehicle Enquiry automatically. CIE means you cannot allow insurance to lapse on a registered vehicle without consequence — even if you do not drive it.

The SORN exception. If you keep your vehicle on private land and do not use it on a public road, you can legally declare a Statutory Off Road Notification (SORN) through the DVLA. A SORNed vehicle does not require insurance, but cannot be driven on a public road without reinstating insurance first.

The Motor Insurers' Bureau (MIB). If you are involved in an accident with an uninsured driver, the MIB compensates victims. The MIB is funded by a levy on all insured drivers — one reason insured drivers pay more in areas with higher rates of uninsured motoring.

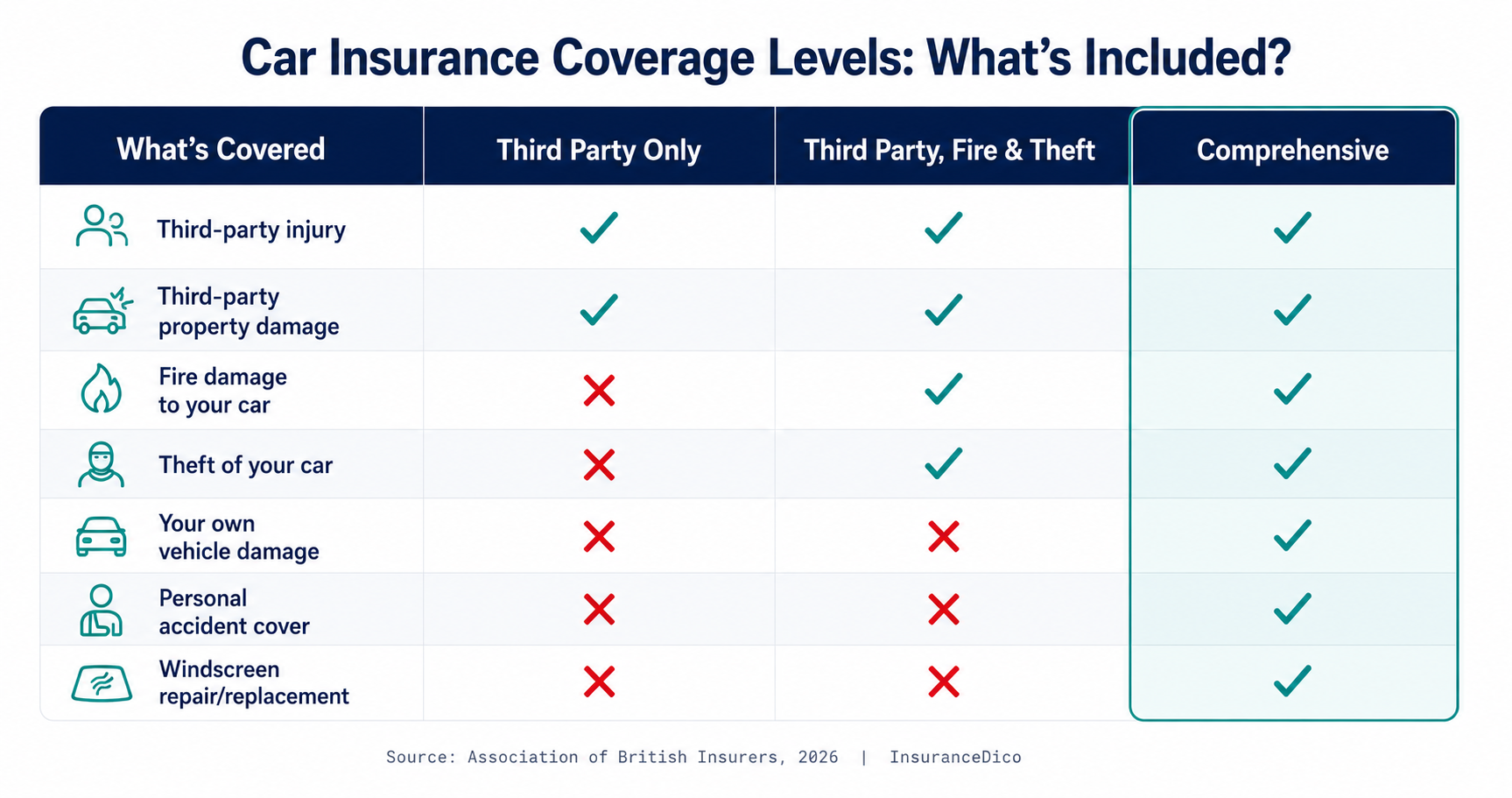

The three levels of cover — and the counterintuitive truth about which is cheapest

UK car insurance is offered at three levels. Most drivers assume they form a straightforward ladder from cheapest to most expensive. They do not.

Third Party Only (TPO)

The legal minimum. Covers damage or injury you cause to other people, their vehicles, and their property. Does not cover your own vehicle, your own injuries, fire damage to your vehicle, or theft of your vehicle. TPO is appropriate for vehicles of very low value (under £1,000) where the cost of repairing or replacing your own vehicle is less than the premium difference between TPO and comprehensive.

Third Party, Fire and Theft (TPFT)

Covers everything TPO covers, plus fire damage to your vehicle and theft of your vehicle or its contents. Still does not cover damage to your own vehicle in an accident you cause.

Comprehensive

Covers all of the above plus damage to your own vehicle regardless of fault, personal accident cover, and windscreen repair and replacement. Most comprehensive policies also include courtesy car provision while your vehicle is being repaired.

Why UK car insurance premiums are at record highs in 2026

The average UK car insurance premium rose 21% in 2023 and a further 8% in 2024, reaching £635 per year in Q1 2026 (ABI Quarterly Motor Insurance Premium Tracker). For drivers under 25, the average exceeds £1,100. For drivers of high-performance vehicles in London, premiums above £3,000 are not unusual.

Claims inflation. Vehicles manufactured after 2018 are significantly more sensor-laden than predecessors — a LIDAR sensor in a wing mirror can cost £1,400 to replace. Paint matching for vehicles with metallic and specialist finishes has increased in cost. Labour rates at franchised dealerships have risen 18% in three years. These costs flow directly through to premiums.

Replacement vehicle costs rose during the semiconductor shortage of 2021–2023, and insurers' repair-network costs rose in parallel. Whiplash fraud, despite the 2021 Whiplash Reform Programme, continues to represent a significant cost within the motor insurance pool.

| Factor | Action | Typical Premium Reduction |

|---|---|---|

| No-Claims Bonus | Preserve your NCB — avoid small claims below £1,500 | 5-year NCB = 50–75% discount |

| Voluntary excess | Increase from £250 to £500 | 10–20% reduction |

| Telematics policy | Accept black box monitoring (especially under 30) | 15–30% reduction |

| Annual payment | Pay annually rather than monthly | 8–15% reduction (avoids implicit APR) |

| Vehicle security | Approved alarm, immobiliser, tracker | 5–15% reduction |

| Parking location | Garage vs driveway vs street | 5–12% reduction |

| Low annual mileage | Declare accurate mileage (under 7,000/yr) | 5–10% reduction |

| Occupation | Some professions carry lower risk profiles | Variable |

How your premium is calculated — the 12 factors insurers actually use

Understanding how insurers price motor risk removes the mystification from comparison results and helps you make better decisions about what you declare at application.

| Entity | Attribute | Value | Source |

|---|---|---|---|

| Age | Risk profile | Peaks 17–24, lowest 30–69, rises again after 70 | ABI Motor Insurance Tracker 2026 |

| No-Claims Bonus | Most powerful single lever | 5+ years claim-free typically earns 50–75% discount | ABI / InsuranceDico broker survey 2026 |

| Vehicle insurance group | Group rating 1–50 | Group 1 small city car vs Group 45 performance car | Thatcham / ABI Group Rating Panel 2026 |

| Annual mileage | Exposure to risk | Under-declaration is material non-disclosure; voids policy | Financial Conduct Authority handbook |

| Postcode | Crime, density, claims history | Rural to city can add 30–60% for same driver/vehicle | ABI postcode rating data 2026 |

| Overnight parking | Theft exposure | Locked garage reduces premium 5–12% vs street | InsuranceDico broker survey 2026 |

| Occupation | Statistical risk class | Teachers/engineers low; couriers/journalists higher | ABI occupational rating tables 2026 |

| Usage type | SDP / commute / business | Business use undeclared invalidates cover at claim | Financial Ombudsman Service decisions 2024–26 |

| Claims & convictions (CUE) | Claims & Underwriting Exchange database | Insurers check CUE at every quote | Insurance Database Services Ltd, CUE 2026 |

| Named drivers | Driver mix on the policy | Adding experienced driver can reduce; young driver raises | InsuranceDico broker survey 2026 |

| Security features | Thatcham-approved devices | Approved alarm/immobiliser/tracker = 5–15% off | Thatcham Research 2026 |

| Voluntary excess | Policyholder contribution | Higher excess = lower premium (e.g. £250→£500 = 10–20% off) | InsuranceDico broker survey 2026 |

The add-ons that are worth having — and the ones that are largely margin

Car insurance add-ons are a significant source of insurer profit margin. Not all are worthless — but several are routinely oversold.

Worth considering

- Motor legal protection (£25–£35/year) — funds the legal pursuit of an at-fault driver's insurer for uninsured losses, excess, loss of earnings and personal injury. Genuine value for its price.

- NCB protection (£50–£80/year) — prevents your no-claims discount from reducing after a fault claim. Most valuable if you have five or more years' NCB built up.

- Breakdown cover (£30–£80/year) — valuable only if you do not already have AA, RAC, or Green Flag membership. Check before adding to avoid duplication.

Questionable value for most drivers

- Key cover (£25–£40/year) — average key replacement for a modern keyless vehicle is £250–£600. Over three years, the premium often equals or exceeds the cost of one replacement.

- Courtesy car upgrade (£15–£30/year) — matters only if driving a small city car for two to three weeks during repairs would genuinely cause you hardship.

- Windscreen cover — included in most comprehensive policies as standard. Confirm before paying extra.

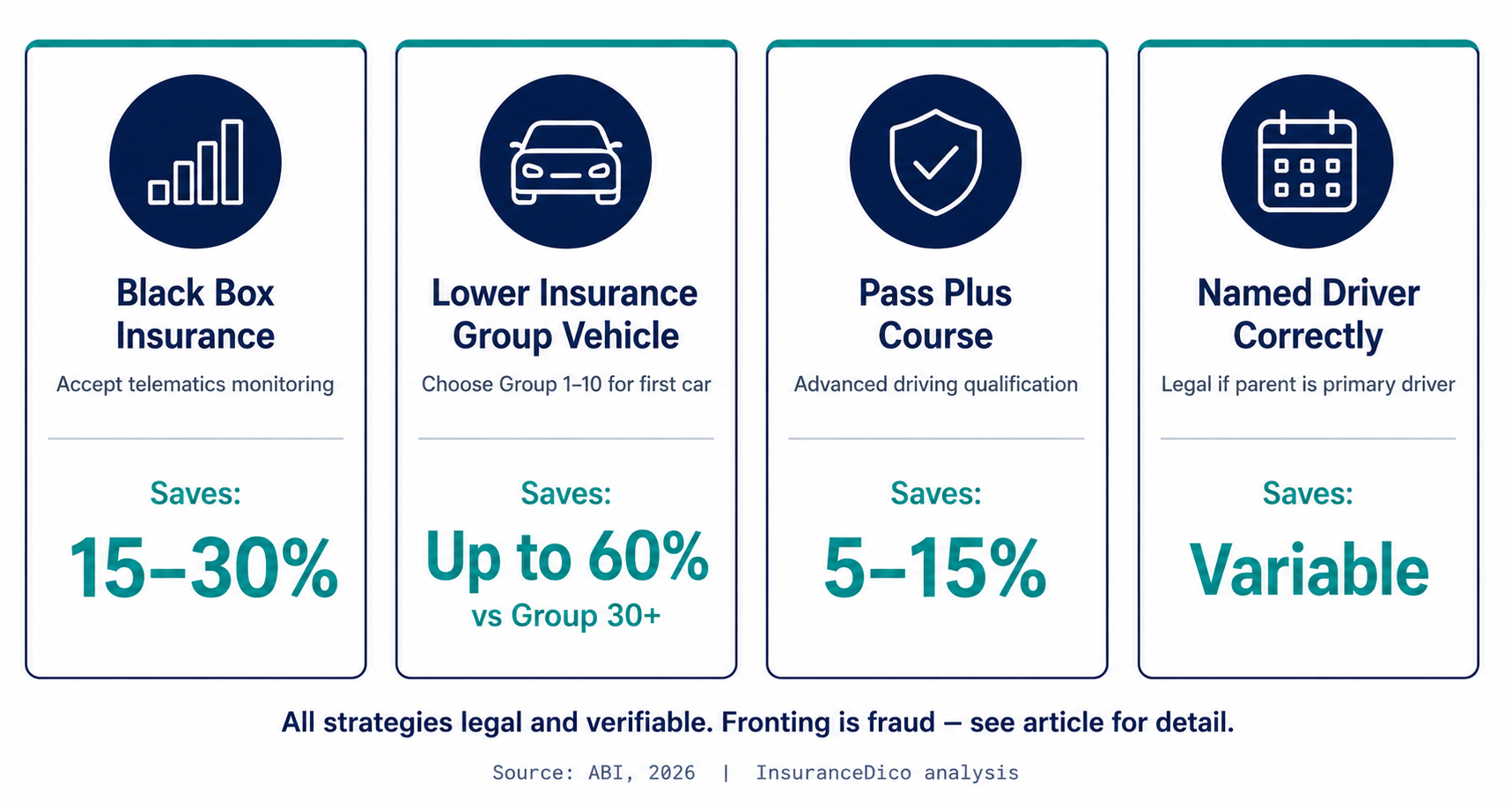

Car insurance for young drivers — cutting costs without cutting corners

Drivers aged 17–24 pay the highest car insurance premiums of any age group. RAC Foundation data shows newly qualified drivers are involved in accidents at a rate three to four times higher per mile than drivers with five or more years' experience.

Black box (telematics) insurance — the biggest legitimate saving

A telematics device (or smartphone app) monitors your driving behaviour: speed relative to limits, acceleration and braking sharpness, cornering forces, time of day, and mileage. Safe driving — measured consistently over the policy term — earns premium reductions at renewal and, in some policies, mid-term adjustments. Typical saving: 20–30% below standard market rate for equivalent coverage at the start of the policy.

What to check: Does the policy restrict night driving (typically midnight to 5am)? Is there a mileage cap? What happens if the device registers a "bad driving" incident? Best providers in 2026: Marmalade, ingenie, Hastings Direct black box, Admiral LittleBox. Each uses different scoring methodologies — compare the specific terms, not just the headline rate.

First-car selection — insurance group matters more than purchase price

A vehicle in group 1–5 (typically a small, naturally aspirated, economy car) can cost £700–£1,200 per year to insure for a 19-year-old. A vehicle in group 20–30 can cost £2,500–£4,000 per year for the same driver. Check the insurance group of any vehicle before agreeing to purchase it — the ABI's vehicle insurance groups lookup tool is freely accessible online.

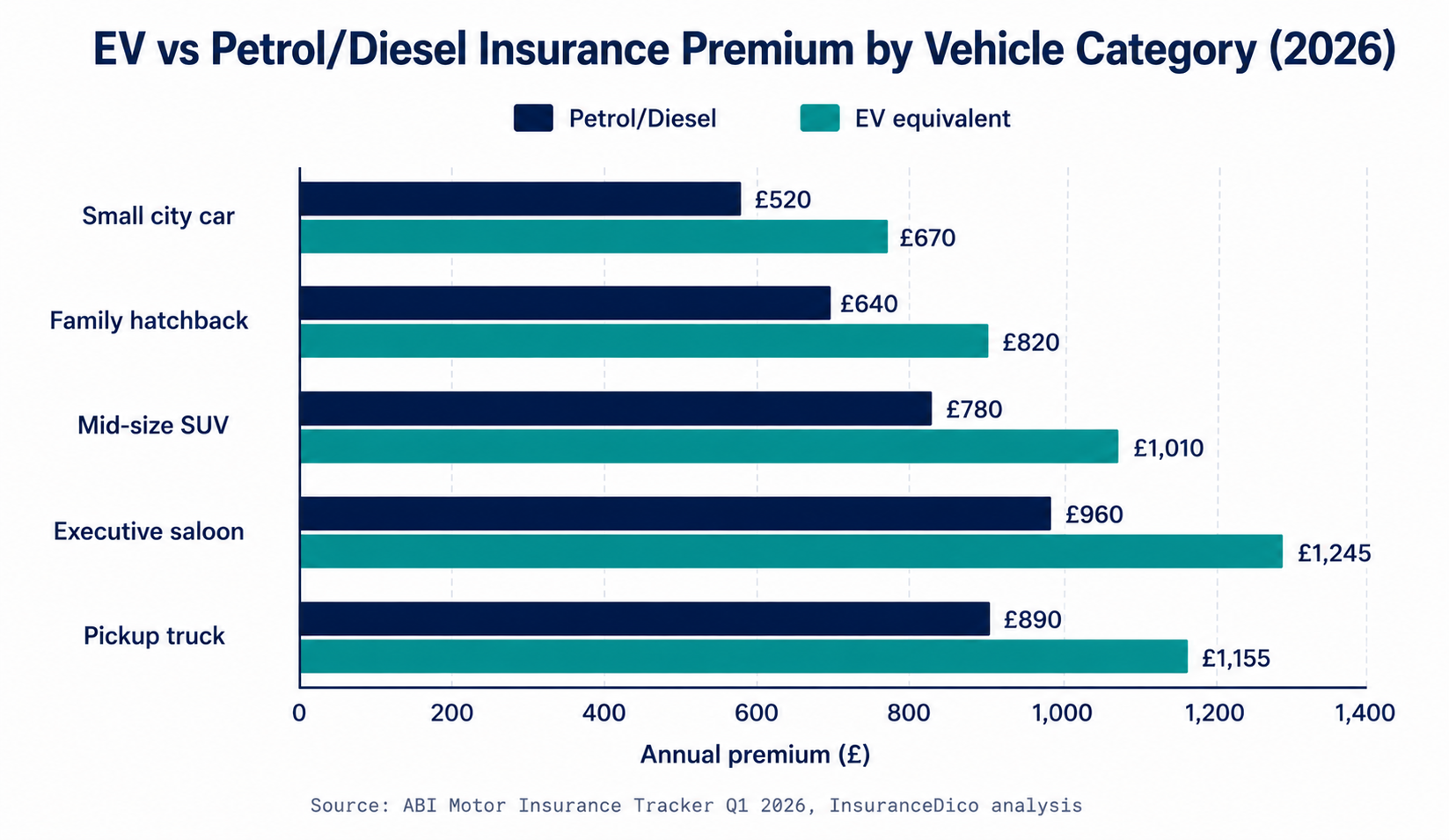

Electric vehicle insurance — why it costs more and how the gap is narrowing

Electric vehicles are systematically more expensive to insure than equivalent petrol or diesel vehicles. ABI data for 2024 shows EV insurance premiums averaging 25–30% above ICE equivalent models.

Repair costs and specialist labour. EV structural repair after even moderate collision damage frequently requires high-voltage battery system assessment before bodywork can proceed. Not all bodyshops are HV-accredited — this limits the repair network.

Parts availability. EV-specific components — electric motors, inverters, charging systems — have less established supply chains than ICE equivalents. Battery replacement exposure. A damaged battery pack costs £8,000–£18,000 for a typical family EV. As battery prices continue to fall (BNEF projects pack costs below $80/kWh by 2027), this premium driver will reduce.

- Battery damage — confirm whether your policy covers deep discharge, charging errors and thermal events, and whether a degraded (not failed) battery is covered.

- Home charging equipment — some EV policies include cover for home wall box chargers; others exclude them. Your home insurance may cover it — check both for duplication or gap.

- Public charging liability — if your cable causes damage to a charging station, liability cover applies. Confirm this is included.

How to make a car insurance claim — avoiding the mistakes that reduce your payout

The actions you take in the first 24 hours after an accident directly affect the outcome of your insurance claim. Most claim disputes arise not from policy coverage gaps but from inadequate evidence collection at the scene.

- Stop and remain at the scene. Leaving the scene of an accident is a criminal offence under the Road Traffic Act 1988, regardless of fault.

- Collect the other driver's details. Full name, address, phone, vehicle registration, insurer name and policy number. You are legally entitled to this information and they are legally required to provide it.

- Photograph everything before vehicles are moved. Both vehicles from multiple angles, all damage, road position, skid marks, road signs, traffic signals, weather, and any visible injuries.

- Gather witness details. Name and phone number of any independent witness. Dashcam footage from your vehicle or others nearby. CCTV from nearby premises.

- Do not admit liability. Even an apology — "I'm sorry, I didn't see you" — can be used against you as an admission of fault. State facts only.

- Report to police if required. If anyone is injured, a vehicle is not roadworthy, or the other driver fails to stop, the accident must be reported within 24 hours under the Road Traffic Act.

Notifying your insurer. Most policy terms require notification "as soon as reasonably practicable" and specify a maximum period (typically 14–30 days). Failure to notify even a non-fault accident can technically void coverage for the incident.

Key takeaways

- Car insurance UK is legally compulsory under the Road Traffic Act 1988 at minimum third-party level.

- Car insurance UK premiums average £635 in 2026; no-claims bonus and excess are your biggest levers.

- Car insurance UK for young drivers averages £1,100 — black box telematics cuts this 20–30%.