Public liability insurance pays your legal defence costs and any compensation awarded if your business is found responsible for injuring a third party or damaging their property. It is not a legal requirement for most UK businesses, but it is contractually required by most commercial clients, government contracts, trade bodies and venue operators. Premiums start at £60 per year for sole traders in low-risk sectors. One in five UK SMEs has faced a liability claim, and the average legal defence cost alone exceeds £13,500 before any compensation is paid.

Public liability insurance is a commercial policy that indemnifies a UK business against third-party claims for accidental bodily injury or property damage arising from its activities, paying both legal defence costs and any compensation awarded up to the policy limit.

What Public Liability Insurance Covers — the Precise Definition

Public liability insurance responds when a third party — anyone outside your business — makes a claim that your business activities caused them injury or caused damage to their property. It covers two costs: the legal cost of defending the claim, and any compensation your business is ordered or agrees to pay.

Third parties include customers, clients, members of the public, delivery drivers visiting your premises, contractors working alongside you, and anyone else who is not on your payroll.

The covered scenarios are physical

- A customer slips on a wet floor in your shop and breaks their wrist

- Your cleaning operative knocks a client's monitor off a desk during a clean

- A tree you have been contracted to prune falls and damages a neighbour's fence

- A visitor to your market stall trips over your equipment and fractures an ankle

- Your decorator spills paint on a client's carpet during a redecoration job

What PLI does not cover — the three most important distinctions

Employees: Your own staff are covered by employers liability insurance, not PLI. These are separate, legally distinct products. Having PLI does not cover you for employee injury claims.

Your own property: PLI covers damage to other people's property. Damage to your own tools, equipment, or premises requires separate business contents or equipment insurance.

Professional negligence: If your advice or service causes a client financial loss, that is a professional indemnity claim. PLI covers physical harm and physical property damage — not financial loss from professional error.

Who Needs Public Liability Insurance — Legal vs Contractual Reality

Legally required: PLI is not legally required for most UK businesses. The one universally legally mandated insurance for businesses is employers liability insurance (under the Employers Liability (Compulsory Insurance) Act 1969). PLI is separately mandated for specific regulated sectors — SIA-licensed security operatives, Gas Safe-registered engineers, and a small number of other licensed activities.

Contractually required: Despite the absence of a universal legal mandate, PLI is functionally unavoidable for businesses that:

- Tender for government or NHS contracts (typically require £5m–£10m PLI)

- Work with commercial clients who include insurance clauses in their contracts

- Participate in trade body or industry accreditation schemes (Constructionline, CHAS, SafeContractor, NICEIC, NAPIT)

- Hire commercial venues, exhibition halls, or market pitches

- Work in sectors where clients routinely require evidence of PLI before engagement

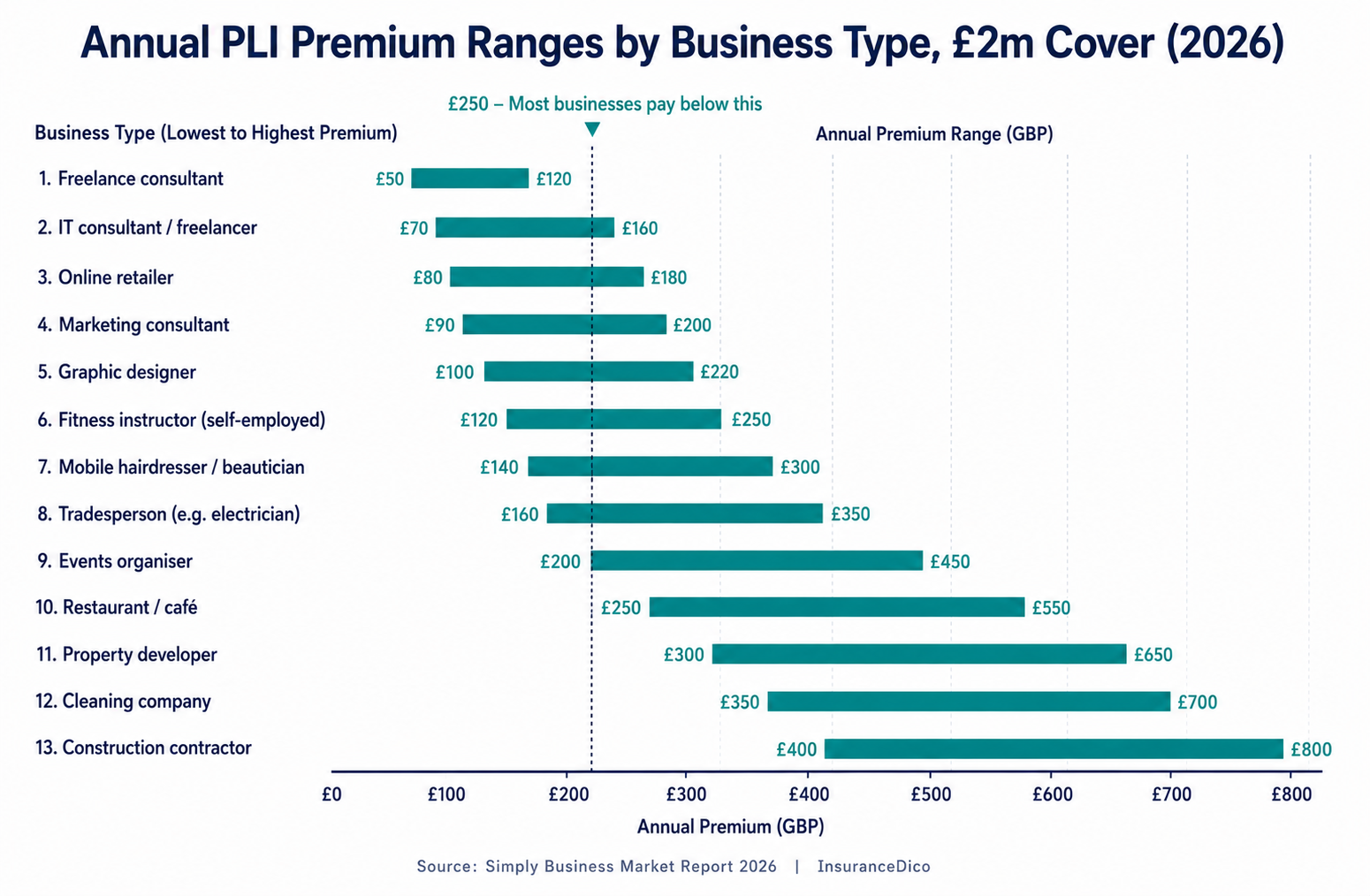

2026 Premium Data by Business Type

PLI premiums reflect the probability and potential severity of a claim for each business type. The gap between the cheapest and most expensive business categories is a factor of ten — and it is actuarially justified.

| Business Type | £1m Cover | £2m Cover | £5m Cover |

|---|---|---|---|

| Freelance consultant / remote professional | £60–£95 | £80–£130 | £110–£185 |

| IT contractor (on-site client visits) | £95–£165 | £125–£215 | £170–£295 |

| Cleaner / domestic cleaning contractor | £115–£185 | £150–£245 | £205–£335 |

| Retail shop (under £250k turnover) | £115–£195 | £150–£255 | £205–£350 |

| Personal trainer / fitness instructor | £125–£210 | £162–£275 | £220–£375 |

| Market trader / craft fair | £110–£185 | £144–£245 | £196–£335 |

| Painter and decorator | £120–£200 | £158–£265 | £215–£360 |

| Plumber (domestic) | £155–£255 | £200–£335 | £270–£455 |

| Electrician (domestic) | £165–£270 | £215–£355 | £290–£480 |

| Business Type | £1m Cover | £2m Cover | £5m Cover |

|---|---|---|---|

| Landscaper / gardener | £135–£225 | £175–£295 | £238–£400 |

| Caterer / food business | £150–£260 | £195–£340 | £265–£460 |

| Event company / organiser | £210–£400 | £275–£525 | £375–£715 |

| Construction contractor (5 employees) | £280–£520 | £365–£675 | £495–£915 |

What PLI Does Not Cover — the Exclusions Most Often Missed

Work at height above three metres: Many standard PLI policies exclude or restrict claims arising from work above three metres. Roofers, scaffolders, and window cleaners on upper floors need a policy that explicitly includes height work — not one that implicitly excludes it.

Unlisted subcontractors: If you engage subcontractors and one causes a third-party incident, standard PLI policies frequently exclude the claim unless the subcontractor is listed on the policy or holds their own PLI. Require PLI certificates from all subcontractors before work starts.

Gradual pollution and contamination: Sudden and accidental pollution events may be covered. Gradual contamination — slow chemical leaching, persistent effluent — is excluded as standard. Businesses handling chemicals, solvents, or fuels may need a specific pollution extension.

Product liability: PLI covers your activities and presence on site. If your business manufactures, imports, or sells physical products that cause harm, that is product liability — a separate coverage that must be specifically added or purchased as a standalone policy.

Professional negligence: If the claim against you is that your advice or work was wrong — not that you physically harmed someone — this falls to professional indemnity insurance. PLI and PI cover adjacent but different risks.

How PLI Claims Work — from Incident to Settlement

Immediately after an incident: Do not admit liability — not even as a social apology. Gather evidence: photos of the scene from multiple angles, names and contact details of any witnesses, a written factual record of what happened and when. Preserve any equipment or materials involved.

Notify your insurer without delay: Most PLI policies require notification 'as soon as reasonably practicable' after any incident that might give rise to a claim — not only after a formal claim has been made. Late notification gives insurers grounds to contest coverage at the point of claim. A brief email or phone call to your insurer or broker within 24–48 hours of the incident is the correct approach.

The insurer takes over: From the point of notification, your insurer appoints solicitors, manages correspondence with the claimant, and makes decisions about whether to settle or defend. You cooperate by providing information — you do not engage the claimant directly or instruct your own solicitors without your insurer's agreement.

Settlement or defence: The majority of UK PLI claims settle before reaching court. Where the claim has merit, the insurer settles at the lowest defensible figure. Where the claim is groundless, the insurer defends. Legal defence costs are covered by the policy — check whether they are included within or in addition to your coverage limit, as some budget policies include them within, reducing the effective compensation available.

The small claim calculation: Before making a claim, calculate the net benefit. A £500 repair claim with a £250 excess returns £250. If the resulting premium loading over three to five years exceeds £250, the claim costs more in the long run than self-funding. This calculation applies to every small claim across every line of business insurance.

| Entity | Attribute | Value | Source |

|---|---|---|---|

| Indemnity limit | Typical minimum for commercial contracts | £2,000,000 | Standard UK B2B contract clause |

| Indemnity limit | Typical minimum for UK government / NHS contracts | £5,000,000 | Crown Commercial Service |

| Legal defence costs | Treatment in 94% of UK SME PLI policies | In addition to the limit | Defaqto 2025 policy-wording survey |

| Excess | Typical voluntary excess range | £250–£1,000 | InsuranceDico 2026 broker survey |

| Notification window | Standard policy condition | As soon as reasonably practicable | ABI model wording |

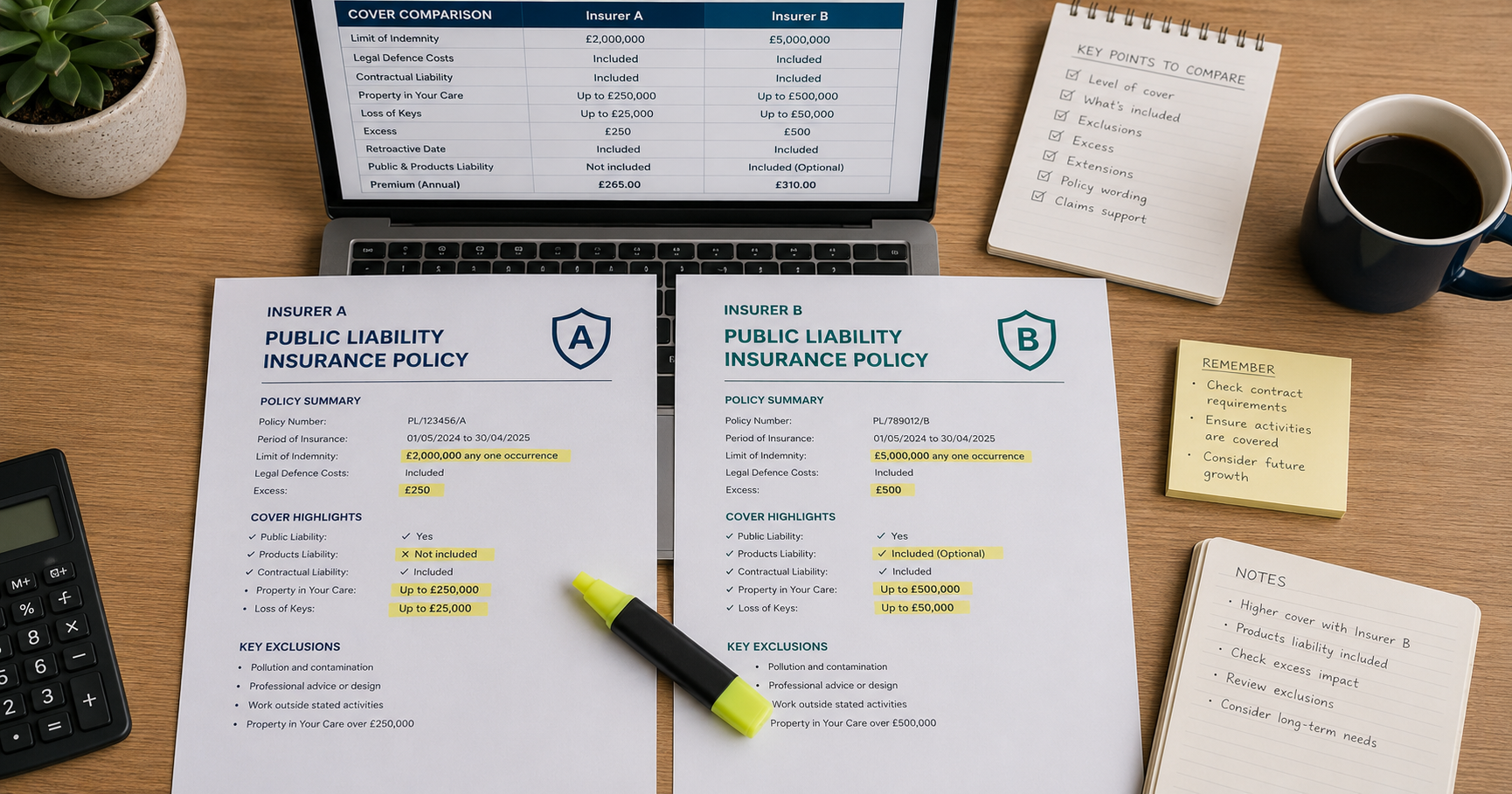

How to Choose PLI — the Five Checks Before Buying

- Confirm all your activities are covered. List your highest-risk business activities — specifically, the three scenarios most likely to produce a third-party claim. Confirm none are excluded by the policy wording. Ask the insurer or broker explicitly if you are unsure.

- Check legal defence costs — within or in addition to the limit. Policies that include legal costs within the coverage limit are materially worse for large claims. Prefer policies where legal defence costs are in addition to the liability limit.

- Match the coverage limit to your contractual requirements. Your largest current or target client sets the minimum. If that minimum is £5m, do not buy £2m to save £80 per year on premium.

- Verify the insurer's financial strength. A policy from a financially weak insurer carries counterparty risk. Look for Fitch or AM Best ratings if the insurer is unfamiliar. Policies underwritten at Lloyd's carry the Lloyd's A+ financial strength rating.

- Understand the renewal terms. Does the policy guarantee renewal after a claim, or can the insurer decline renewal? For businesses in sectors with higher claim frequency, guaranteed renewability is a material policy feature worth seeking.

“The exclusions section of the policy document — not the summary page — determines what is actually covered.”

Key takeaways

- Public liability insurance pays legal defence costs and compensation when your business injures a third party or damages their property.

- PLI is not legally required for most UK businesses, but commercial clients, government contracts and trade bodies make it functionally unavoidable.

- Premiums range from £60 a year for a freelance consultant at £1m cover to over £900 for a construction contractor at £5m cover.