Key man insurance — also called key person insurance — is a life insurance or critical illness policy taken out by a business on an individual whose death or serious illness would cause material financial damage to the business. The business pays the premiums and receives the payout. It is distinct from personal life insurance (where the family benefits) and from shareholder protection (which deals with ownership transfer). The tax treatment is nuanced — premiums may or may not be corporation tax deductible depending on the structure and purpose of the policy. Coverage is typically set at three to five times the individual's annual contribution to gross profit.

Key man insurance is a UK business protection product where the company owns and benefits from a life or critical illness policy on an essential individual — paying a lump sum to the business if that person dies or is diagnosed with a covered serious illness, compensating for lost revenue, recruitment costs, and operational disruption.

What Key Man Insurance Is — and the Three Things It Is Not

Key man insurance is a business protection product. Three common confusions are worth clearing upfront:

It is not personal life insurance. Personal life insurance names the individual's family or estate as beneficiary. Key man insurance names the business as beneficiary. The payout goes to the company's bank account — not to the individual's family. If a director wants their family protected, they need a separate personal life insurance policy alongside any key man cover the business holds on them.

It is not shareholder protection. Shareholder protection insurance funds the purchase of a deceased or critically ill shareholder's shares by the remaining shareholders. Key man insurance compensates the business for the financial loss caused by losing the person — it does not resolve the ownership question.

It is not employers' liability insurance. EL covers physical injury to employees during work. Key man insurance covers the business's financial exposure to losing a specific individual entirely.

What key man insurance actually does: When a business loses a key person — through death or serious illness — it typically faces one or more of these financial consequences:

- Loss of revenue generated by that individual (a top-performing sales director, a specialist fee-earner in a professional practice, a founder with key client relationships)

- Cost of finding, recruiting, and onboarding a replacement (typically 50–200% of annual salary for senior roles)

- Loss of a specific capability that cannot be immediately replaced (a specialist technical qualification, a regulatory approval held personally)

- Disruption to a live contract or project that the individual was leading

- Lender concern if the key person was a condition of a business loan covenant

Key man insurance provides a lump sum that gives the business financial breathing room — to fund recruitment, absorb the revenue shortfall, service debts, and stabilise without making crisis-driven decisions.

Who Qualifies as a "Key Person" for Insurance Purposes

There is no regulatory definition of a key person. For insurance purposes, the question is: whose death or serious incapacity would cause measurable financial loss to the business?

The financial materiality test: Not every valuable employee qualifies as a key person for insurance purposes. The coverage must be linked to a quantifiable financial impact. Insurers expect you to articulate:

- What revenue or gross profit is directly attributable to this individual

- What the estimated cost of replacement or business disruption would be

- What loan or credit covenants are linked to this individual's involvement

Roles that typically qualify:

- Company founders and co-founders whose client relationships and reputation drive the majority of business revenue

- Managing directors and CEOs of SMEs where the individual is the primary commercial face of the business

- Top-performing sales directors or account managers responsible for a material proportion of turnover

- Specialist technical professionals whose qualifications are legally required for the business to operate (e.g. the Responsible Person in a pharmacy, the Health and Safety Director in a licensed contractor)

- The individual named in a lender's personal guarantee or covenant clause

- Lead clinicians or professionals in a practice where the principal holds the CQC registration or key professional licence

Roles that typically do not qualify for dedicated key man cover: Roles that can be reasonably replaced within three to four months through recruitment without material business disruption — experienced middle management, departmental heads in larger businesses, roles with no unique client or commercial relationships attached.

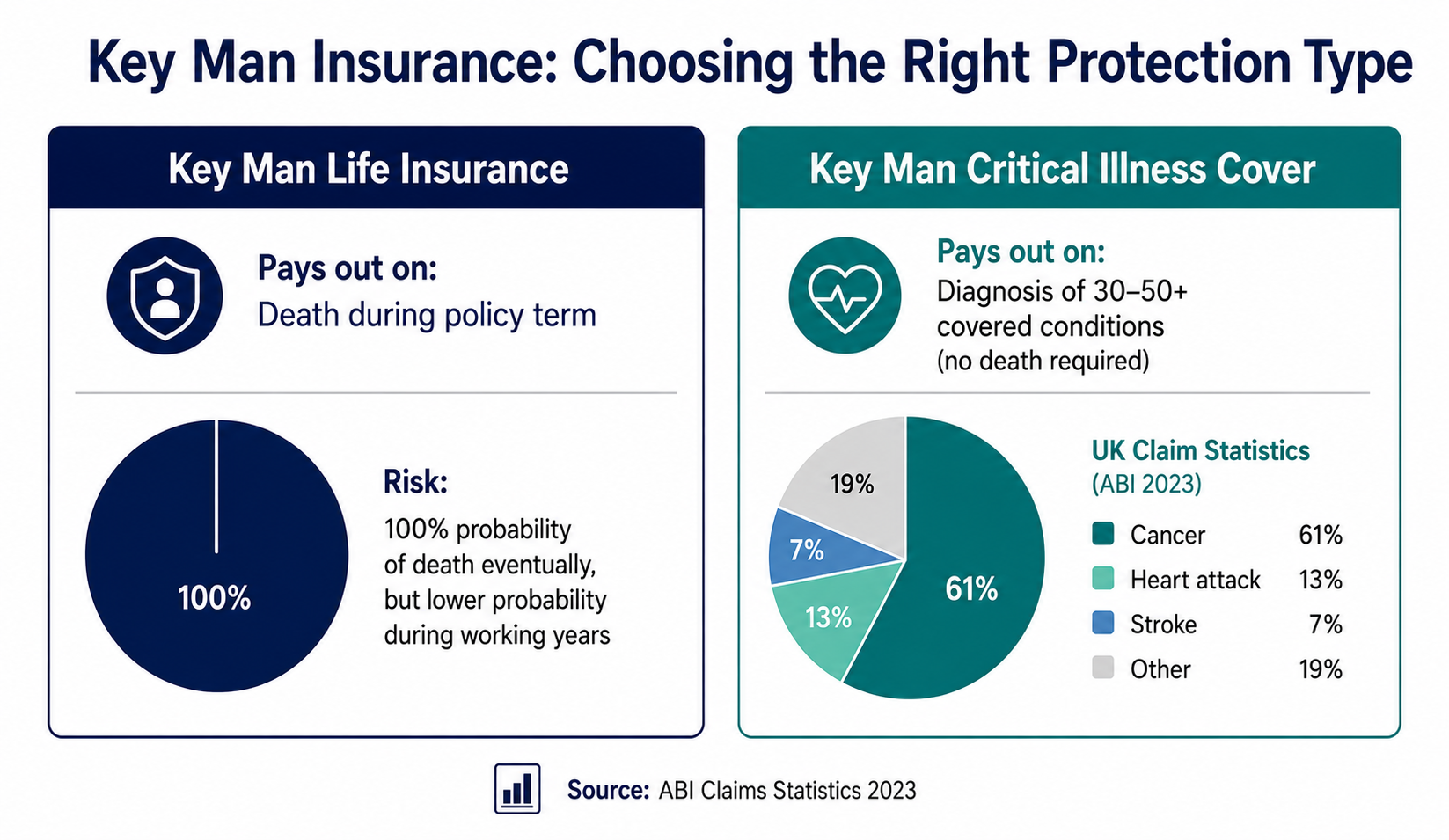

Key Man Life Insurance vs Key Man Critical Illness Cover

Key man insurance is available in two protection forms, and most businesses that take it seriously buy both.

Key Man Life Insurance

Pays a lump sum to the business if the key person dies during the policy term. Structured identically to personal term life insurance in underwriting terms — the insurer assesses the key person's age, health, smoking status, and coverage amount. The business is the policy owner and beneficiary throughout.

Appropriate when: The primary financial risk is the permanent loss of the individual — revenue generated, client relationships, contracts in progress.

Key Man Critical Illness Cover

Pays a lump sum to the business if the key person is diagnosed with a specified serious illness (cancer, heart attack, stroke, and typically 30–50+ further conditions depending on the policy). The individual does not have to die — a diagnosis of a covered condition triggers the payment.

Appropriate when: The business is more exposed to the extended absence or reduced capacity of the key person than to their death. A managing director who suffers a heart attack and is unable to work for 12–18 months creates the same financial disruption as death — but without triggering a life policy.

The combined approach: Most key man strategies use a combination: life coverage for the full calculated exposure plus critical illness coverage for the same or a reduced amount. The critical illness payout is used to fund the recovery period. The life insurance payout addresses permanent loss.

The Tax Treatment of Key Man Insurance — the HMRC Position

The tax treatment of key man insurance premiums and payouts is one of the most frequently misunderstood aspects of the product. The position differs depending on the type of coverage and its stated purpose.

When Premiums Are NOT Corporation Tax Deductible

A pure key man life insurance policy — one that provides a lump sum only on death during the term — is treated by HMRC as a capital asset of the business. Premiums for capital protection are not allowable deductions against corporation tax (HMRC Business Income Manual BIM45530).

The corresponding benefit: Because the premium was not deductible, the payout on death is not treated as a trading receipt — it is received tax-free by the company as a capital receipt.

When Premiums MAY Be Corporation Tax Deductible

HMRC accepts that key man insurance premiums can be treated as an allowable revenue expense (and therefore CT deductible) where all of the following apply:

- The insurance is taken out to protect against loss of profits — not to provide a capital windfall

- The term of the policy is short (typically five years or less) and the policy is not convertible into another form

- The key person is an employee or director (not a shareholder in a capacity that would suggest capital protection)

- There is no element of the policy that builds a surrender value

The corresponding consequence: Where premiums are CT deductible, the payout is treated as a trading receipt and subject to corporation tax in the year received.

The Relevant Life Policy — a Tax-Efficient Alternative for Directors

A relevant life policy is a separate product — a single-person death-in-service arrangement structured through the business — that provides personal life insurance for an employee or director in a tax-efficient way.

Under a relevant life policy:

- The business pays the premium

- The premium is typically allowable against corporation tax

- The premium does not count as a benefit in kind (P11D) for the employee

- The payout on death goes directly to the employee's family, held in a trust outside the company

It is distinct from key man insurance — the purpose is the employee's personal protection, not the business's protection against financial loss. Many limited company directors benefit from holding both: a relevant life policy (personal protection via the company) and being subject to key man cover (business protection for the company).

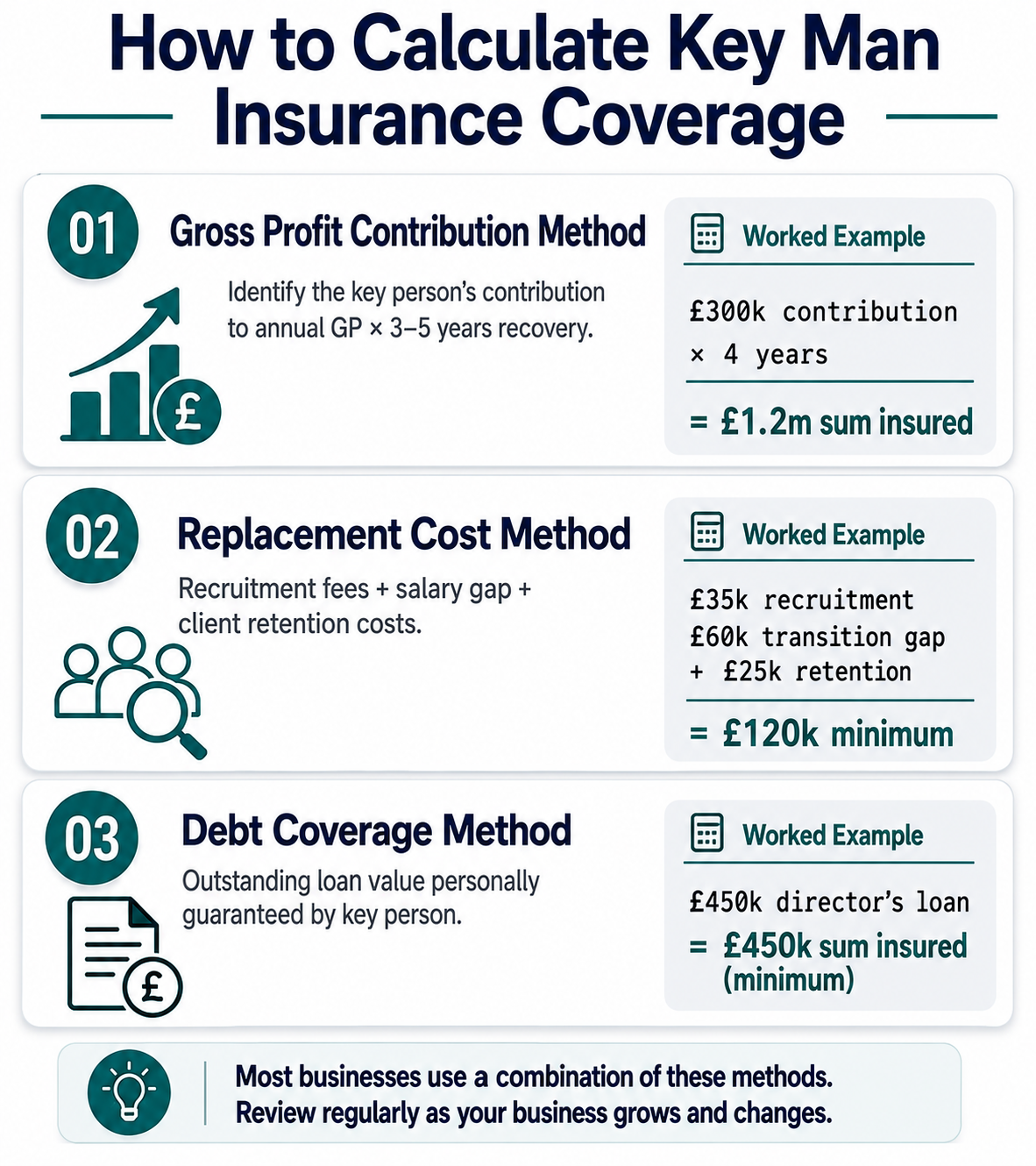

How Much Key Man Insurance Coverage Is Needed

The sum insured for key man insurance is calculated from the financial exposure the business faces — not from the individual's personal life insurance needs.

Method 1 — Multiple of Gross Profit Contribution

Identify the proportion of business gross profit directly attributable to the key person. Multiply by three to five years (the estimated recovery period). This is the most commonly used approach and the one insurers most readily accept.

Method 2 — Replacement Cost

Calculate the total cost of finding, recruiting, and onboarding a replacement to the same level of effectiveness — including recruitment fees (typically 20–30% of annual salary for senior roles), signing bonuses, the cost of a transition period where the replacement is not fully effective, and the cost of any client retention initiatives during the gap.

Method 3 — Loan or Debt Coverage

Where the business has loans with personal guarantee clauses tied to the key person, or where lender covenants reference the individual's involvement, the outstanding loan balance is a direct and specific coverage need.

Typical Coverage Amounts by Business Type

| Business Type / Role | Typical Coverage Range |

|---|---|

| Sole founder, professional practice (£200k revenue) | £300,000–£750,000 |

| MD / CEO, SME (£1m–£3m revenue) | £500,000–£1,500,000 |

| Top sales director (40% of new business) | £200,000–£600,000 |

| Technical specialist (essential regulatory qualification) | £150,000–£400,000 |

| Co-founder, funded startup | £250,000–£1,000,000 |

What Key Man Insurance Costs in 2026

Key man insurance is priced identically to personal life insurance — because it is personal life insurance, rated on the individual being covered. The key person's age, health, and smoking status are the primary underwriting inputs. The only structural difference is the policy owner (the business) and the beneficiary (the business).

| Individual Profile | £500k Life (10yr) | £500k Critical Illness (10yr) | Combined |

|---|---|---|---|

| Age 35, non-smoker, good health | £28–£45/mo | £55–£85/mo | £83–£130/mo |

| Age 40, non-smoker, good health | £38–£62/mo | £78–£120/mo | £116–£182/mo |

| Age 45, non-smoker, good health | £58–£95/mo | £118–£185/mo | £176–£280/mo |

| Age 50, non-smoker, good health | £95–£158/mo | £195–£310/mo | £290–£468/mo |

| Age 40, smoker | £75–£125/mo | £155–£245/mo | £230–£370/mo |