A public liability insurance claim moves through four distinct stages: evidence at the scene, notification to your insurer, cooperation with their investigation, and either settlement or defence. The decisions you make in the first 48 hours, particularly what you say and who you say it to, usually determine the outcome long before the claims handler sees the file.

The Claims Process, Step by Step

Step 1, At the Scene: Evidence Before Anything Else

The 30 minutes immediately following an incident are the most important for your eventual claim outcome. Evidence gathered at the scene is evidence you control. Evidence assembled later, from memory, from CCTV footage requests, from witness recollections, is less reliable and sometimes unavailable.

What to gather before anything is moved or cleared:

Photography, the single most important action. Photograph the scene from multiple angles before anything is moved, cleaned, or repaired. Photograph the hazard that caused the incident (the wet floor, the trip hazard, the damaged item). Photograph the damage or injury from multiple distances. Photograph the surrounding environment, the location, any relevant signs (or their absence), the weather or lighting conditions. Time-stamped smartphone photos are sufficient and admissible.

The injured person's details. Full name, address, phone number, and if possible email address. You are legally entitled to ask for this information and they are legally entitled to provide it or decline, if they decline, record that they declined.

Witness details. Names and contact numbers of anyone who observed the incident. Independent witnesses are significantly more valuable than employees of either party. Ask witnesses to write a brief factual account while their recollection is fresh.

A written factual record. Write down exactly what happened, where, when, what was occurring immediately before the incident, and what you observed of the injury or damage. This record should describe only what you directly observed, not your interpretation or assessment of cause or fault.

What not to do at the scene:

- Do not say "I'm sorry" or "I apologise", apologies are frequently cited as admissions of liability by claimants' solicitors. You can express concern for a person's welfare ("Are you alright? Is there anything I can do to help?") without accepting liability.

- Do not say "Don't worry, our insurance will cover this", this may be construed as an admission that an insurable incident occurred and that you are responsible.

- Do not agree to pay anything or commit to any financial resolution before speaking to your insurer.

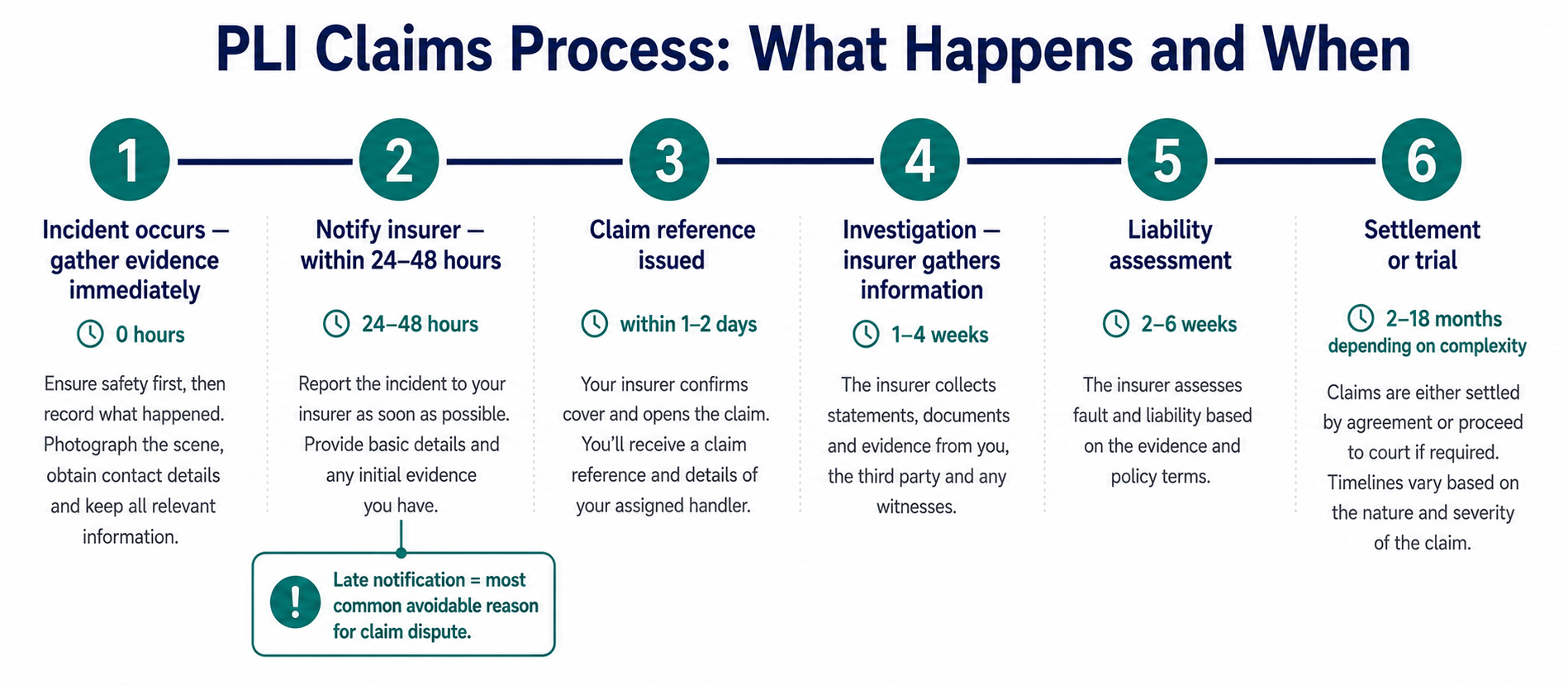

Step 2, Notify Your Insurer Promptly

The notification requirement. Most PLI policies require notification of any incident that might give rise to a claim "as soon as reasonably practicable." In practice, this means within 24–48 hours of the incident for a straightforward claim, and within hours for a serious incident (significant injury, major property damage).

Late notification is one of the three most common reasons PLI claims are disputed. An insurer who is notified weeks after an incident has a legitimate argument that the delay prejudiced their ability to investigate, gather evidence, and manage the claim properly. Most policies allow them to reduce or refuse a settlement in these circumstances.

How to notify. Call your insurer's claims line or your broker's claims notification service. Have the following ready:

- Your policy number

- The date, time, and location of the incident

- A brief description of what happened

- The injured party's or claimant's name and contact details (if you have them)

- Details of any injuries or property damage observed

What happens after notification. Your insurer assigns a claims handler. For smaller claims, this is typically a member of the insurer's in-house claims team. For larger or more complex claims, a specialist loss adjuster may be appointed. You will receive a claim reference number, keep this for all future correspondence.

Step 3, Cooperate With Your Insurer's Investigation

Once notified, your insurer manages the claim. Your role is to cooperate, providing documents, attending meetings, and giving truthful accounts, not to conduct your own investigation or negotiate with the claimant.

Do not communicate directly with the claimant or their solicitors once you have notified your insurer. All communication should be directed to your insurer's claims team. If you receive correspondence directly from the claimant or their solicitors, forward it to your insurer the same day, do not respond yourself.

Documents your insurer may request:

- Your written account of the incident (prepared at the scene)

- Photographs and any video footage

- Relevant business records (maintenance logs, risk assessments, training records)

- Names and statements from employees present

- Contracts or agreements with the claimant where relevant

- Any previous correspondence with the claimant about the hazard or location

Step 4, Settlement or Defence

Settlement. The majority of PLI claims settle before reaching court. Your insurer's legal team assesses whether the claim has merit and at what level. If the claim has merit, the insurer negotiates a settlement at the lowest defensible figure. You pay the agreed excess; the insurer pays the rest up to the policy limit.

Defence. If the claim is without merit, the injury was not caused by your activities, the claimant is exaggerating, or the evidence does not support the claim, your insurer defends the claim to trial. The legal costs of defence are covered by your policy within the legal costs limit.

The excess. You pay the agreed excess at the point of settlement, not at the point of notification. The excess is deducted from the settlement figure paid to the claimant, if the settlement is £8,000 and your excess is £500, the insurer pays £7,500 to the claimant and invoices you for £500.

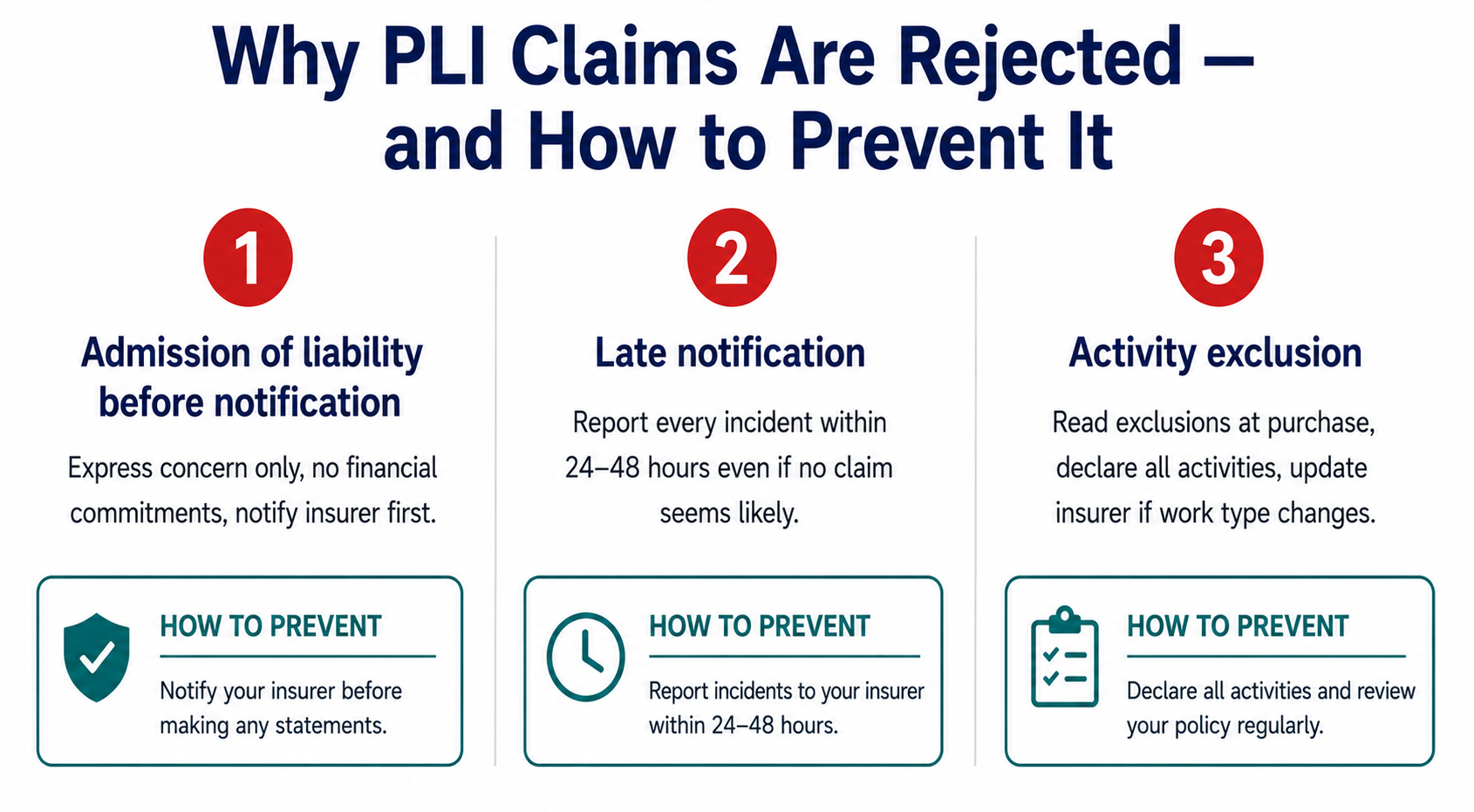

The Three Most Common Reasons PLI Claims Are Rejected

Understanding why claims fail is more useful than knowing how they succeed. The three most frequently cited reasons for PLI claim rejection or reduction are all avoidable with the right approach.

Reason 1, Admission of Liability Before Notification

An apology, a verbal statement accepting responsibility, or a written commitment to pay for damage, any of these made before the insurer is notified gives the claimant grounds to pursue a claim independently of your insurer's assessment.

Insurers reserve the right to manage their own defence of claims. When you admit liability before notification, you remove the insurer's ability to dispute the claim and may allow a settlement that is higher than a properly defended claim would produce. Some policies specifically exclude claims where the policyholder has admitted liability without the insurer's consent.

The correct position. Express concern. Gather evidence. Notify your insurer. Let the insurer assess liability and manage communication from that point.

Reason 2, Late Notification Prejudicing the Insurer's Position

Incidents that are not reported to the insurer until weeks or months later have diminished evidence trails. Witnesses' recollections have faded. Physical evidence has been cleaned up or repaired. CCTV footage has been overwritten. The claimant has had time to instruct solicitors and build a legal case before the insurer can investigate.

Late notification gives the insurer grounds to argue that their ability to defend the claim was prejudiced by the delay. The more prejudiced their position, the stronger their argument for reducing the settlement or declining the claim.

The practice that prevents this. Treat any incident, even one where you believe no claim will follow, as a potential claim and notify your insurer immediately. An incident that produces no claim results in a claim record but no payout. An incident that produces a claim six months later and was never notified is a coverage dispute.

Reason 3, The Incident Falling Within an Exclusion

The claim is valid in principle, a third party was injured or their property was damaged, but the specific circumstances fall within a policy exclusion. Common examples:

- The incident arose from work at heights above the policy's threshold

- The incident was caused by a subcontractor not listed on the policy

- The damage was to property in the policyholder's care, custody, and control

- The incident arose from an activity not disclosed at application

How to avoid this. Read your exclusions section when you purchase the policy, not when you need to claim. Confirm that your specific high-risk activities are covered. Declare all activities accurately. Update the insurer when you take on new types of work.

Typical PLI Claim Timelines

Settlement time depends almost entirely on the nature of the loss. Property damage settles fastest; personal injury claims requiring medical evidence take the longest.

| Claim type | Typical time to settle | Notes |

|---|---|---|

| Minor property damage, undisputed | 4–12 weeks | Settled directly with claimant once liability is agreed |

| Soft-tissue personal injury | 3–9 months | Medical evidence required before a final offer is made |

| Serious personal injury | 12–36 months+ | Rehabilitation, prognosis and loss-of-earnings calculations |

| Disputed liability or litigated | 12–24 months | May proceed to trial if no settlement is reached |

What Happens If Your Claim Is Rejected

If your insurer declines a PLI claim you believe is valid, you have a defined escalation path.

Step 1, Internal complaint. Submit a formal written complaint to the insurer's complaints department. Most insurers are required by FCA rules to acknowledge within 5 working days and provide a final response within 8 weeks.

Step 2, Financial Ombudsman Service (FOS). If the internal complaint does not resolve the dispute, you can escalate to the FOS at no cost. The FOS handles disputes between UK businesses with annual turnover under £6.5m and their insurers. The FOS resolved 66% of insurance complaints in favour of the policyholder or small business in 2023. The FOS decision is binding on the insurer but not on you, you can still pursue legal action if you disagree with the FOS outcome.

Step 3, Legal action. If the FOS is unavailable (your turnover exceeds £6.5m) or you choose not to use it, legal action against the insurer for wrongful rejection of a claim is a civil matter. Given the complexity and cost, most businesses use the FOS route first.