There is a widespread assumption that public liability insurance (PLI) for freelancers is simply a box-ticking exercise, something clients demand, but not something a remote copywriter or developer actually needs. That assumption conflates two distinct questions: do I legally need it, and will I lose work without it? For UK freelancers in 2026, the second question is the one that decides the purchase.

Most freelancers in professional service roles face low physical third-party liability risk, but most commercial clients require £1m–£2m PLI as a contractual condition of engagement. Typical annual cost: £60–£150 for professional categories, £100–£250 for trades and on-site work.

The Two Separate Reasons a Freelancer Needs PLI, and Why Both Matter

Question 1, Do I legally need it? For most freelancers: no. PLI is not legally required for the self-employed unless you operate in a regulated sector with specific mandatory requirements (SIA security licence holders, Gas Safe engineers, certain childcare and healthcare roles).

Question 2, Will I lose work without it? Almost certainly yes if you work with commercial clients, agencies, platforms, or event organisers. This is the practical reality that makes PLI non-optional regardless of how low your physical risk is.

The two reasons operate independently. A fully remote developer with zero client contact may have genuine physical liability risk close to zero, but still needs PLI to win the clients whose contracts require it. A personal trainer who works in client homes faces both genuine physical risk and contractual requirement. Understanding which applies to your situation determines the right coverage level, not whether to buy it.

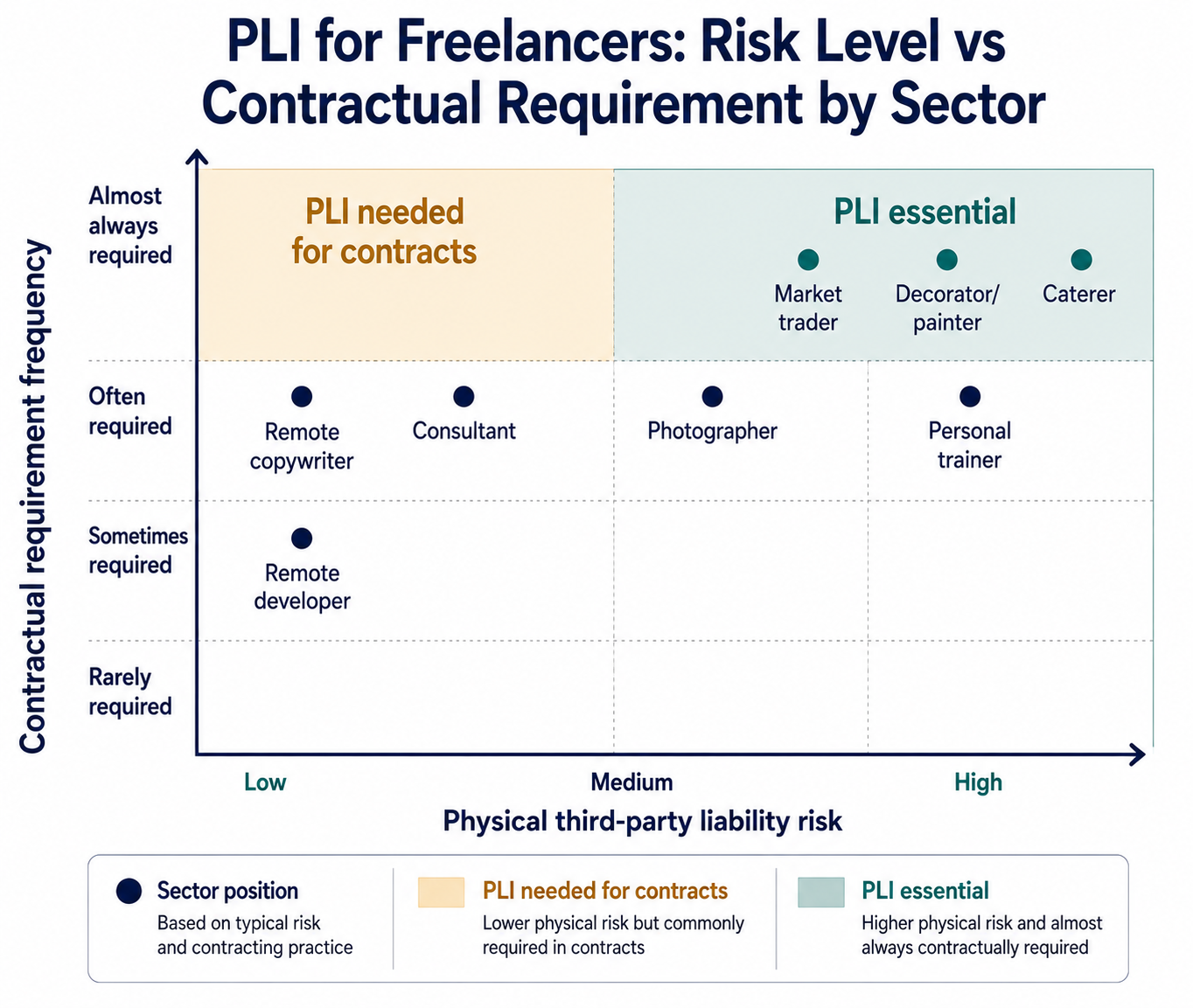

Freelance Sectors, Who Faces Real Physical Risk vs Contractual Requirement

High Physical Risk, PLI Responds to Genuine Incidents

Personal trainers and fitness instructors: Working in client homes, gyms, or outdoor spaces creates multiple third-party injury scenarios. A client injures themselves during an exercise you prescribed and supervised. A piece of equipment you brought to a session damages a client's flooring. A client's child is hurt by equipment you left unattended. These are genuine PLI scenarios that occur regularly in the fitness industry.

Photographers and videographers: On-location shoots in client premises, public spaces, and events create physical liability through equipment placement, tripods, lighting rigs, cables, backdrops. A guest at a wedding trips over a camera cable. A lighting stand falls and damages a client's artwork. These are among the most common claims against creative freelancers.

Makeup artists and beauty therapists: Working in clients' homes means working in their personal space with their belongings. A product reaction causing injury, a spillage damaging furniture, or a client tripping over a bag you left in a doorway are all PLI claims. Most clients booking these services for events now expect evidence of PLI before the booking is confirmed.

Builders, decorators, and tradespeople operating as sole traders: The highest physical risk freelance category. Working on clients' properties, using tools and materials that can cause damage, and operating in environments where third-party injuries (to the client, household members, or other workers) are a genuine ongoing exposure.

Market traders, caterers, and food businesses: Operating in public spaces with members of the public present throughout. Trip hazards from equipment and displays, food-related claims, and property damage to adjacent traders are all PLI exposures.

Low Physical Risk, Contractual Requirement Drives the Purchase

Copywriters and content creators: Working entirely remotely with no client visits and no client site visits, the physical third-party liability risk is essentially zero. However, most agency contracts and many direct client agreements include an insurance clause requiring PLI. A copywriter without PLI cannot fulfil the terms of these contracts.

Web developers and software developers (remote): The same pattern. Zero physical third-party risk when working remotely. Contractual requirement from agencies, marketplaces (Toptal, Andela, some Upwork enterprise clients), and direct corporate clients who include standard supplier insurance clauses in their purchase orders.

Business coaches and consultants (remote): Similar position. The risk of advice causing financial loss is a professional indemnity matter. The risk of physical injury to a third party is minimal for fully remote workers. Contractual requirement drives the purchase decision.

Graphic designers and brand designers: Entirely remote with no client contact means physical liability is negligible. Contractual requirement is common, particularly with agency clients who hold their own PLI at £2m or £5m and require matching coverage from all contractors on their roster.

How Much PLI Costs for Different Freelance Categories (2026)

Freelance PLI premiums are among the lowest in the UK market, sole traders in professional services with no employees and low public exposure represent minimal risk to insurers. Premiums scale upward where work involves physical activity, client premises, or members of the public.

| Freelance Category | £1m Cover | £2m Cover | Notes |

|---|---|---|---|

| Remote copywriter / writer | £58–£92 | £78–£125 | Lowest risk category |

| Graphic designer / brand designer | £62–£98 | £82–£135 | Remote only |

| Web developer (remote) | £65–£105 | £86–£142 | Client visits increase premium |

| Business consultant / coach | £70–£115 | £92–£155 | Advisory risk is PI, not PLI |

| Photographer / videographer | £95–£155 | £125–£205 | On-location exposure |

| Personal trainer / fitness instructor | £120–£200 | £158–£265 | Physical activity risk |

| Makeup artist / hair stylist (mobile) | £110–£185 | £145–£245 | Client premises exposure |

| Market trader | £105–£180 | £138–£240 | Public footfall risk |

| Decorator / painter | £120–£200 | £158–£265 | Client property risk |

Paying for the coverage your clients actually require: The most common mistake freelancers make is purchasing the cheapest available policy, typically £1m, when their clients' contracts require £2m. The premium difference between £1m and £2m is £20–£50 per year. The consequence of having insufficient coverage is being in breach of contract or being unable to begin work pending evidence of compliant insurance. Always check contract requirements before selecting a coverage level.

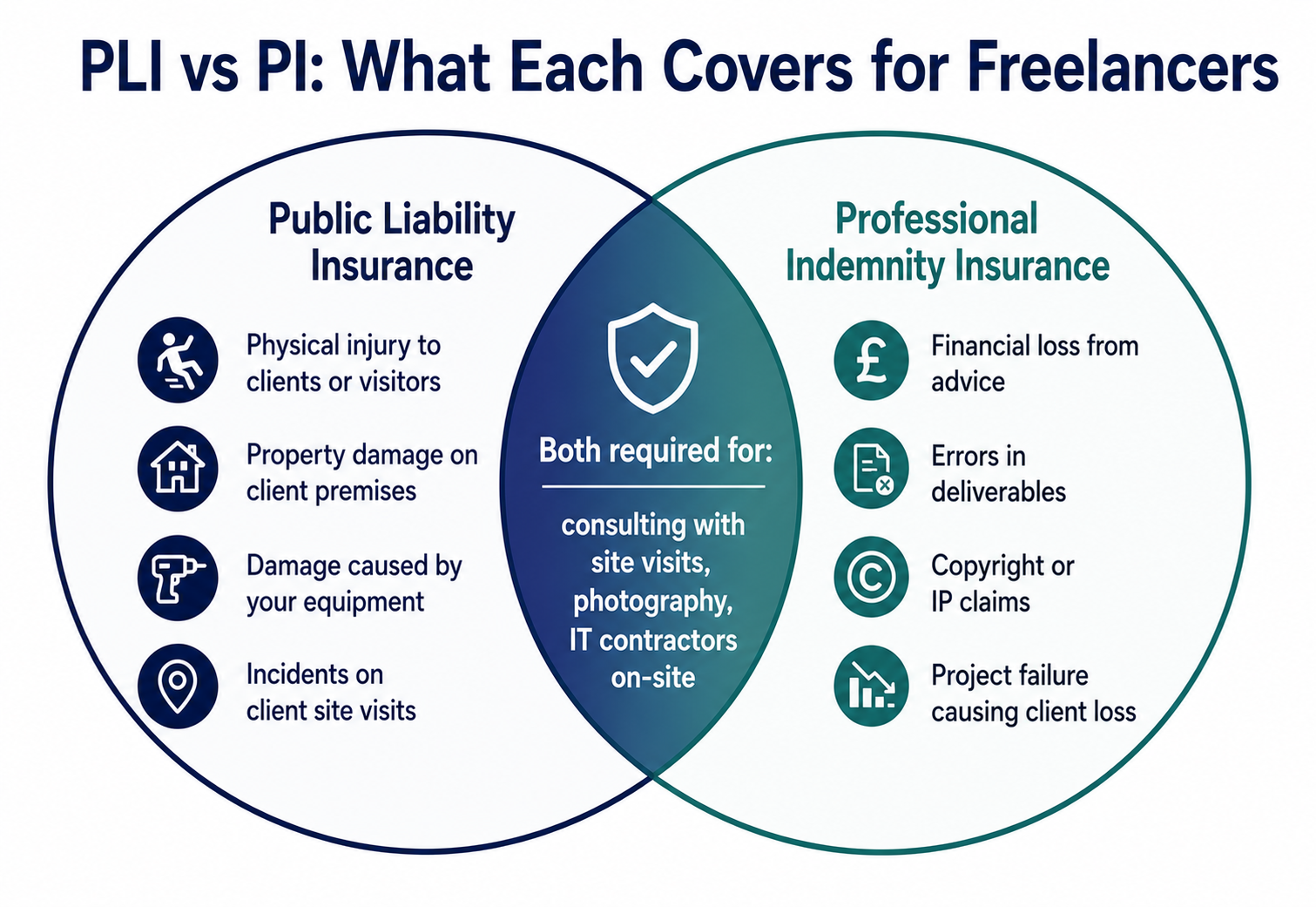

What PLI Covers and What It Doesn't for Freelancers

What Your PLI Policy Responds To

Third-party bodily injury caused by your activities: A client you are training at their home slips on a mat you placed on a wet floor and fractures their wrist. Your PLI insurer pays the legal defence costs and any compensation awarded.

Damage to third-party property caused by your activities: During a photography shoot, your assistant knocks a client's antique mirror off a shelf. The mirror is worth £800. Your PLI insurer pays.

Third-party claims arising from your presence on their premises: A visitor to the office where you are working trips over your laptop bag left in a corridor. Your PLI insurer defends the claim.

What Your PLI Policy Does Not Respond To

Professional errors or bad advice: If a client suffers financial loss because your copywriting was inaccurate, your branding strategy failed, or your consulting advice proved wrong, these are professional indemnity claims, not public liability claims. Freelancers who provide any form of advice, strategy, or professional output need professional indemnity insurance in addition to PLI.

Damage to property in your care: Equipment a client has handed to you for work, a camera body you are repairing, a device you are developing for, is in your care. Damage to that specific equipment while in your possession is excluded under the standard care, custody, and control exclusion.

Your own equipment: Your laptop, camera, portable hard drives, and work tools are not covered by PLI. These require business equipment insurance or a business contents extension on your home insurance.

Do Freelancers Need PLI and Professional Indemnity?

Most freelancers who provide professional services need both PLI and professional indemnity insurance, they cover fundamentally different risks. PLI covers physical harm to third parties and physical damage to their property. Professional Indemnity (PI) covers financial loss to clients arising from your professional errors, omissions, or advice.

The freelancer who needs both: A consultant who both visits client premises (PLI risk) and provides strategic advice that clients act on (PI risk). A web developer who attends client offices for briefings (PLI) and whose code may contain defects causing client financial loss (PI).

The freelancer who may need only PLI: A market trader or event caterer who provides physical goods and services with no advisory element. Physical liability only; no professional output being relied upon.

The freelancer who may need only PI: A fully remote writer, analyst, or consultant who has no client visits and no physical interaction with third parties. Their risk is financial harm from their output, not physical harm from their presence.

A combined PLI and PI policy from a business insurance provider is typically 10–20% cheaper than purchasing both separately and covers both risks with a single renewal date and policy document.

Where Freelancers Buy PLI, the Fastest Route

Online specialist platforms: Simply Business, Hiscox Direct, AXA Business, and Policy Bee all offer instant PLI quotes for freelancers with same-day policy certificates. For most freelance categories, a policy is in place and the certificate emailed within 30 minutes of payment.

Freelance platform requirements: Some freelance marketplaces (PeoplePerHour, Bark.com, Checkatrade) display insurance badges and some verify certificates before allowing bids on certain work categories. Uploading your PLI certificate to your marketplace profile strengthens client trust and can unlock premium listing tiers.

Checking your existing coverage: If you already hold a combined personal and business insurance product, such as a home-office policy, check whether PLI is already included before purchasing separately. Some home-business policies include up to £1m PLI for business visitors and business activities conducted from the home address.

Key takeaways

- PLI is rarely a legal requirement for freelancers but is a contractual requirement from most agencies, platforms, and commercial clients.

- Most professional freelancers pay £60–£150 a year for £1m–£2m cover; trades and on-site freelancers pay £100–£265.

- PLI covers physical injury and property damage to third parties, professional errors, your own kit, and business visitors to a home not declared as a business address are not covered.