Contractor PLI, the Specific Risks That Make Construction Different

Contracting, particularly in construction, trades, and civil engineering, creates a category of PLI exposure that is genuinely more complex than most other business sectors. Several factors combine to make contractor PLI both more important and more nuanced than the equivalent product for office-based businesses.

Physical risk is constant and high: Construction and trades work involves tools, equipment, vehicles, and materials in environments where third parties (clients, neighbouring properties, the public) are regularly present. The probability of a third-party incident is orders of magnitude higher than for a desk-based business.

Contract values are large: When a contractor causes damage to a client's premises during a commercial refurbishment project, the claim is not against a domestic property, it is against a commercial property with a rebuild cost potentially in the hundreds of thousands. Coverage limits that are adequate for a cleaning company are inadequate for a major contractor.

Principal and subcontractor relationships create layered liability: Most significant construction projects involve a principal contractor and multiple subcontractors. Who is liable when a subcontractor causes a third-party incident depends on the contract structure, and in many cases the principal contractor bears residual liability even when they did not directly cause the incident.

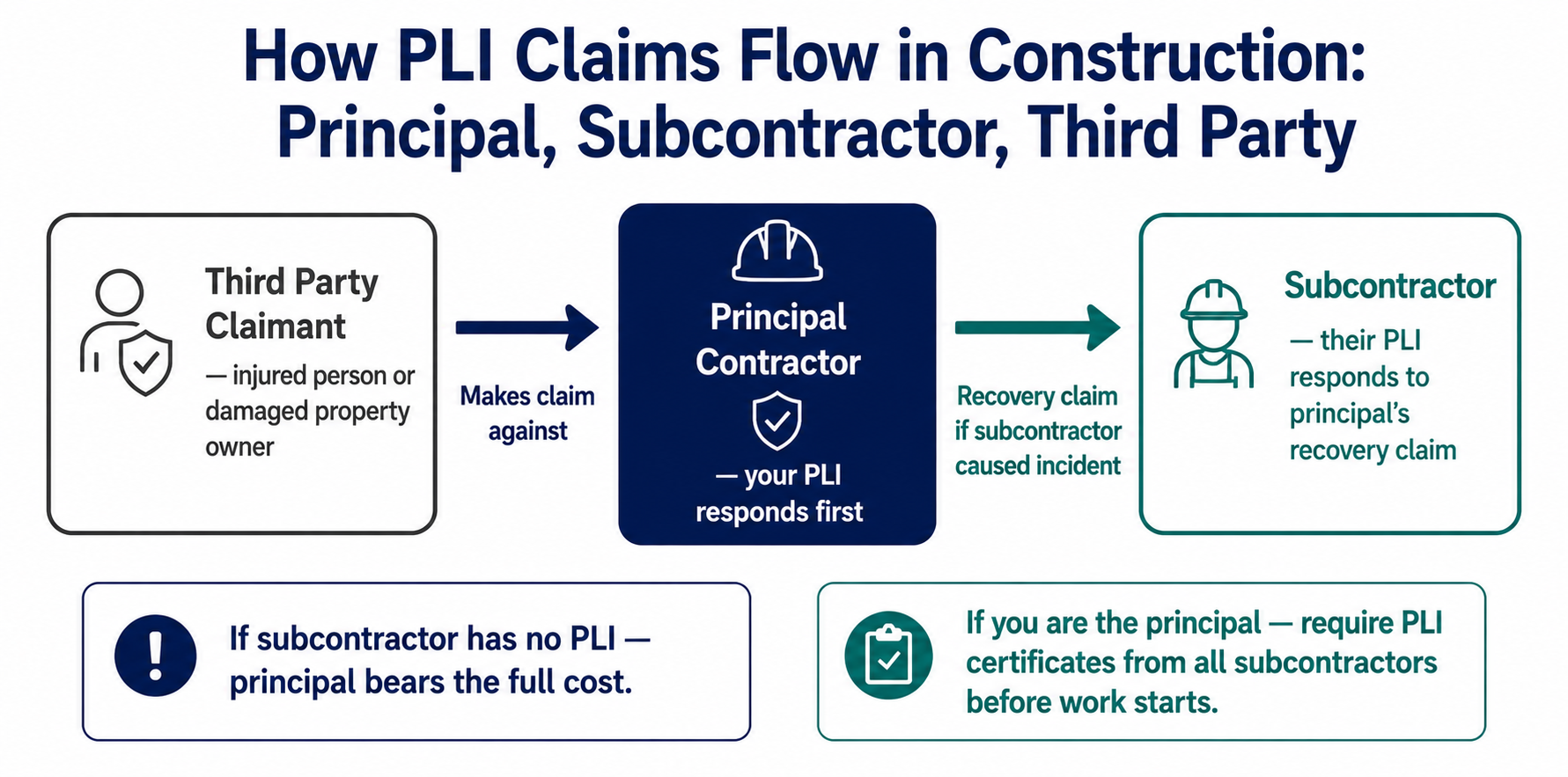

Principal Contractor vs Subcontractor, Who Owes What to Whom

This is the most poorly understood aspect of contractor PLI and the one most likely to produce an uninsured claim.

When You Are the Principal Contractor

As the principal contractor, you have contracted directly with the client to deliver a project. You engage subcontractors to perform specific elements. Your contractual relationship with the client makes you their point of contact for all project-related claims.

The liability flow: If a subcontractor you engaged causes a third-party incident during your project, a bricklayer damages a neighbouring property's boundary wall, a plumber floods the floor below, the injured party (the neighbour, the property below) typically pursues the claim against the principal contractor. You are the party the client hired and the party named in the planning permission and building contract.

Your PLI position: Your PLI policy must cover principal contractor liability. Standard PLI policies cover your own activities, check specifically whether your policy extends to claims arising from subcontractors working under your engagement.

The correct approach to subcontractors:

- Require every subcontractor to hold their own valid PLI at a specified minimum level

- Collect their PLI certificates before they begin work and check the expiry dates

- Confirm your own PLI covers residual principal contractor liability for subcontractor activities on your projects

When You Are a Subcontractor

As a subcontractor, your direct client is typically the principal contractor, not the building owner. Your PLI needs to cover your specific trade activities on the project.

Who the claim follows: If you cause a third-party incident as a subcontractor, the claim will initially go to the principal contractor (from the third party) and the principal contractor will then seek to recover from you (as the party whose activity caused the incident). Your PLI responds to the recovery claim from the principal, not directly to the original third party.

The specific coverage requirement: Your PLI must cover your trade activities on third-party premises (the construction site). If your policy was priced for "office visits to clients" rather than "on-site construction work," your activities may not be covered. Activity description accuracy is critical for subcontractors.

⚠️ Warning: If you are a subcontractor engaged by a principal contractor who then makes a recovery claim against you for a third-party incident you caused, but your PLI excludes the specific activity involved, you face the recovery claim personally. A subcontractor who is an electrician but whose PLI was declared for "domestic property visits" may find the policy excludes commercial site work. Declare your actual activities accurately at application, and update the insurer if your work type changes.

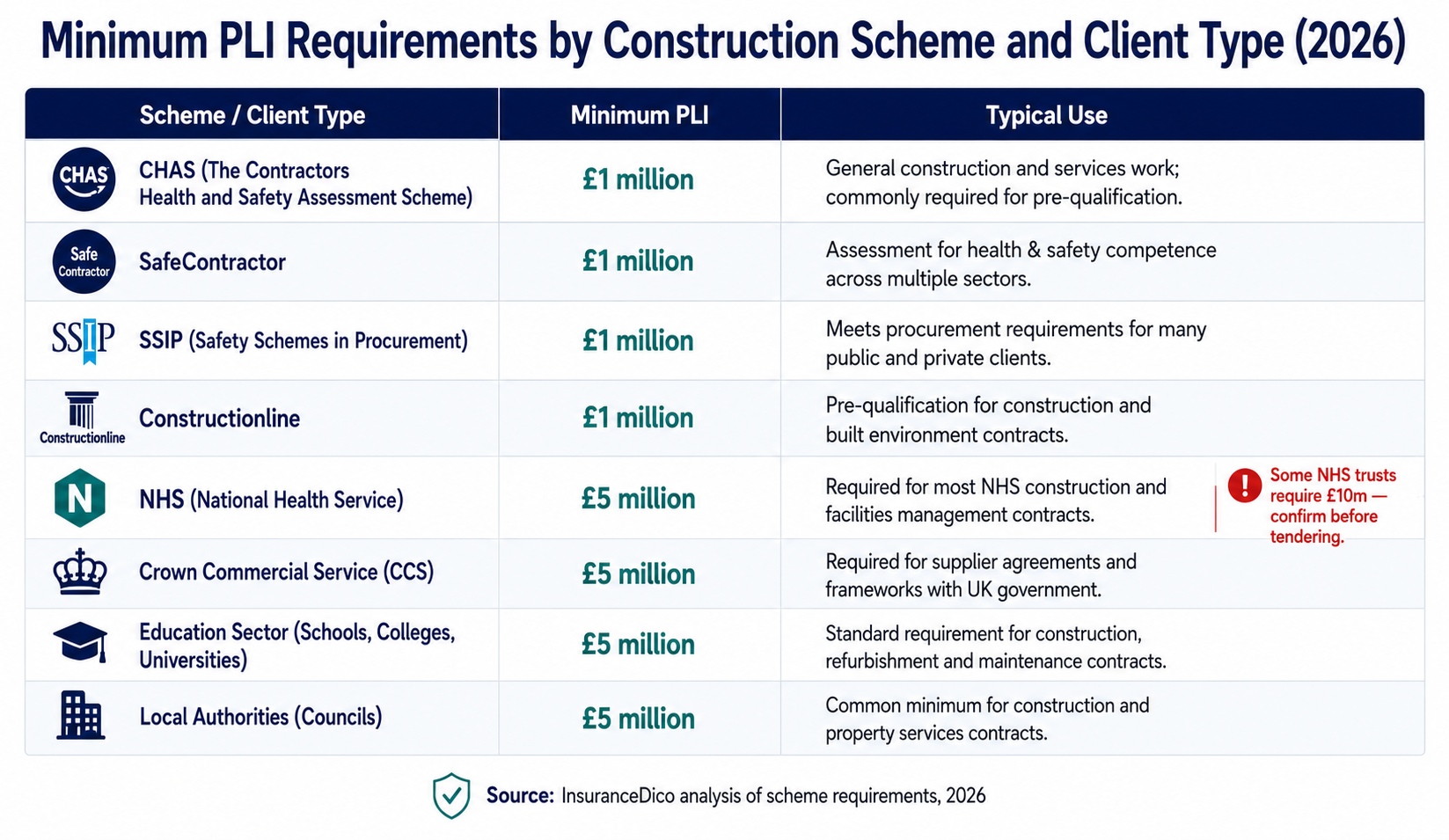

The Minimum PLI Coverage Levels Required on UK Construction Projects

Coverage minimums for contractor PLI vary significantly by project type, client type, and scheme membership. The following are the standard minimums you will encounter:

| Framework / Scheme | Minimum PLI Required | Notes |

|---|---|---|

| Constructionline Standard | £1m–£2m | Minimum for scheme entry |

| Constructionline Gold | £5m | Required for government framework |

| CHAS (Contractors Health & Safety) | £5m | Standard for local authority work |

| SafeContractor | £5m | Required for supply chain accreditation |

| NICEIC (electricians) | £2m minimum | Part of registration conditions |

| Gas Safe Register | £2m minimum | Part of licensing conditions |

| NHS construction projects | £10m | Often above standard £5m floor |

| HS2 and major infrastructure | £10m–£50m+ | Specialist placement required |

| Standard residential client contract | £1m–£2m | Home renovation, domestic work |

The practical takeaway: Any contractor pursuing commercial work, public sector work, or accreditation scheme membership needs a minimum of £5m PLI. Buying £2m because it is cheaper eliminates access to the frameworks and contracts that make commercial contracting viable.

2026 PLI Premiums for Contractors by Trade

Contractor PLI premiums reflect the physical risk level of the specific trade and the scale of operations. The following ranges apply to sole traders or small contractors with 1–4 employees and no prior claims.

Domestic Trades (Primarily Residential Work)

| Trade | £2m Cover | £5m Cover |

|---|---|---|

| General builder | £215–£358 | £295–£492 |

| Electrician (domestic) | £215–£358 | £295–£492 |

| Plumber / gas engineer | £205–£345 | £282–£475 |

| Plasterer | £185–£312 | £255–£428 |

| Carpenter / joiner | £190–£318 | £262–£438 |

| Painter and decorator | £170–£288 | £234–£395 |

| Tiler | £178–£300 | £245–£412 |

| Kitchen fitter | £198–£332 | £272–£458 |

Commercial and Specialist Trades

| Trade | £2m Cover | £5m Cover |

|---|---|---|

| Commercial electrician | £265–£445 | £365–£610 |

| Mechanical / HVAC contractor | £278–£468 | £382–£645 |

| Groundworks contractor | £285–£478 | £392–£658 |

| Steel erector | £325–£545 | £448–£750 |

| Scaffolder | £380–£638 | £522–£878 |

| Roofer | £290–£488 | £398–£672 |

| Demolition contractor | £420–£705 | £578–£972 |

Source: InsuranceDico 2026 market analysis. Sole trader or 1–4 employees, UK only, no prior claims, standard risk activities.

Why height and demolition attract the highest premiums: Work at height (roofing, scaffolding) and work involving structural removal (demolition) create the highest-severity third-party claim scenarios, falling debris, structural collapse, heavy plant operation near third-party property. Insurers load these trades accordingly, and many standard PLI policies exclude work at heights above three metres without a specific high-risk extension.

The Exclusions That Catch Contractors Out Most Often

Height Work Above the Policy Limit

Standard PLI policies commonly exclude or restrict claims arising from work above a defined height threshold, often three metres. Roofers, scaffolders, and window cleaners above ground floor level need a policy that explicitly covers height work, not a standard policy that may exclude it.

Check your policy for height restrictions before starting any above-ground work. Ask the insurer specifically: "Does this policy cover work on a roof at [X] metres height?" Get the answer in writing if it affects a significant contract.

Subcontractors Not Listed or Not Holding Their Own PLI

As discussed, your policy may exclude claims arising from subcontractors who are not listed on your policy or who do not hold their own valid PLI. This exclusion can make the difference between a covered claim and a personal financial liability on a significant project.

Contract Works, Physical Damage to the Project Itself

PLI covers third-party property damage, damage to property that belongs to someone other than you. It does not cover damage to the work itself, the structure you are building or renovating. If a fire damages a building you are working on, the damage to the existing structure may be a PLI claim; damage to the newly built element is a contract works (or contractors all-risk) insurance claim.

Contract works insurance is a separate product that contractors on significant build projects should hold. It is often arranged by the principal contractor to cover all parties on a project under a single policy.

Professional Design Errors

If you perform design-and-build work and the design element contains an error that causes physical damage or financial loss, this may fall outside PLI into professional indemnity territory. Contractors who design as well as build, design-and-build firms, specialist contractors producing structural drawings, need professional indemnity insurance in addition to PLI.