Why Reading the Exclusions Section Matters More Than Reading the Summary

Every PLI policy features a "What We Cover" summary page, a concise, readable document that describes the policy's coverage in plain terms. This is the page that most buyers read before purchasing. It is not the most important page in the policy document.

The most important section is the exclusions, typically pages 8–22 of the full policy wording. These pages describe when the policy does not pay. Coverage determines whether a broad class of claims is insured. Exclusions determine whether your specific claim is paid.

Most PLI disputes arise not because the incident was outside the policy's core coverage, third-party injury or property damage, but because a specific exclusion clause applied to the circumstances of the incident. Understanding these exclusions before purchase prevents both coverage gaps and post-claim surprises.

The Six Core Exclusions, Standard Across All UK PLI Policies

These exclusions apply to every PLI policy in the UK market. They are not negotiable and cannot be removed. They define the product boundaries.

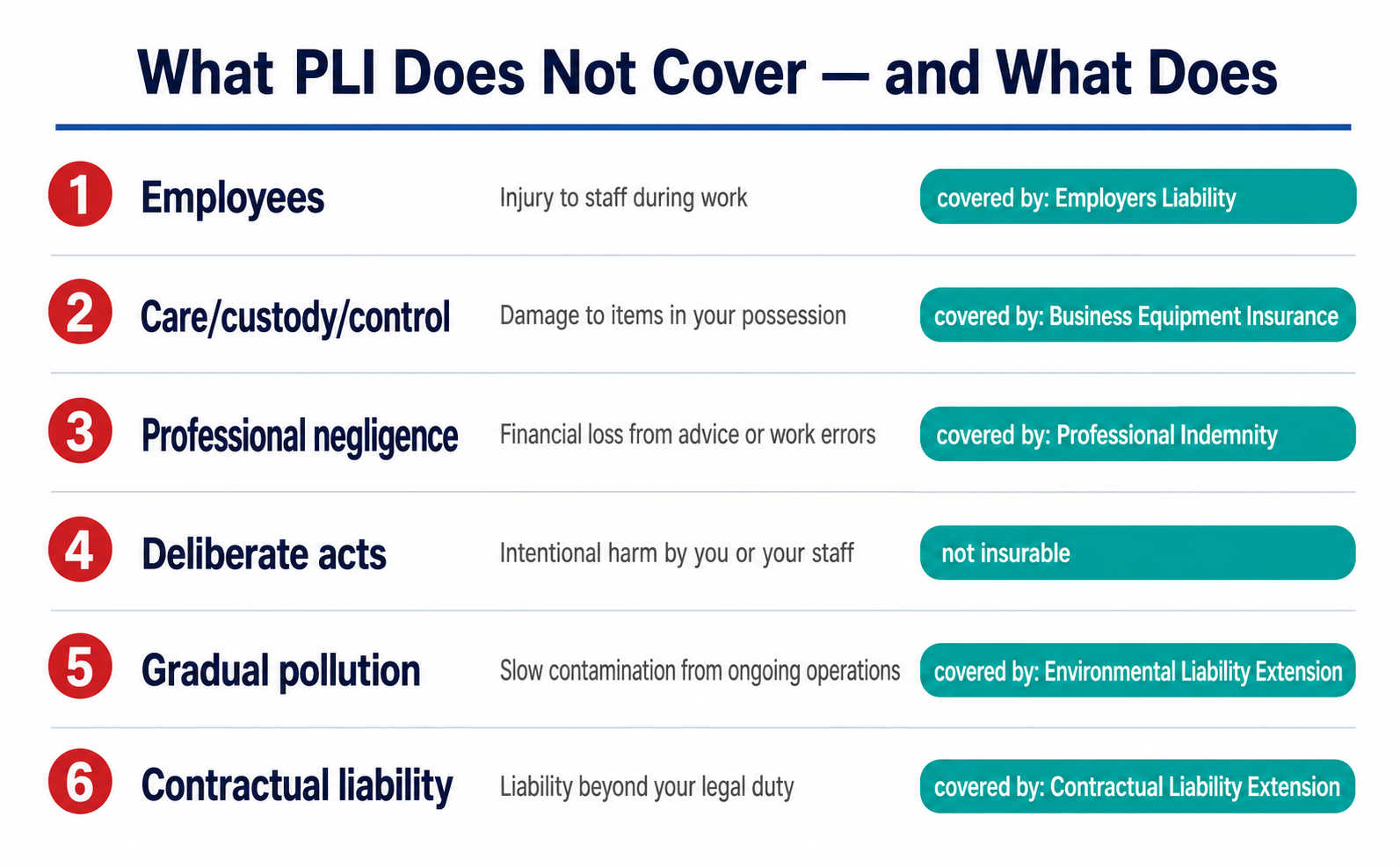

Exclusion 1, Your Own Employees

PLI covers claims from third parties outside your business. Employees are not third parties, they are covered by employers liability insurance, which is a legally separate and mandatory product.

Where this boundary becomes complicated:

The legal definition of "employee" for insurance purposes is broader than most business owners assume. Workers who may be classified as employees despite being paid on a self-employed basis include:

- Labour-only subcontractors (those who supply only their own labour with no materials or equipment of their own)

- Agency workers operating under your day-to-day supervision and direction

- Apprentices and work experience participants under your supervision

- Casual workers paid informally or on a cash basis

If any of these worker types are injured during your business activities, the claim is an employers liability claim, not a PLI claim. Without EL insurance, this claim is entirely uninsured.

⚠️ Warning: A sole trader who engages one labourer for a three-day job, paying cash, using informal arrangements, may be operating as an "employer" for EL insurance purposes. If the labourer is injured during those three days, the PLI policy provides no coverage. The EL policy, which the sole trader probably does not hold, is the required product. When in doubt, treat any worker whose activities you direct as an employee and arrange EL insurance accordingly.

Exclusion 2, Property in Your Care, Custody, or Control

PLI covers damage to third-party property. It does not cover damage to property that is in your physical possession at the time of the damage.

The boundary in practice:

A plumber working on a client's boiler accidentally damages the boiler itself, the specific item he was contracted to work on. This damage is excluded as property in his care. The boiler is in his possession.

The same plumber, while working on the boiler, accidentally knocks a mirror off the wall in the adjacent hallway. The mirror is third-party property not being worked on. This damage is covered by PLI.

The grey zone that most commonly causes disputes:

Equipment, materials, and structures at a worksite that are adjacent to but not directly being worked on. A carpenter fitting a kitchen who damages the kitchen floor tiles while moving units is in a grey area, some policies treat all property at the worksite as "in care," others draw the boundary narrowly at only the specific item being actively worked on.

The extension that addresses this gap:

A "property in care, custody, and control" extension is available from most specialist contractor PLI providers. It extends coverage to third-party property that is in your possession during the course of your work, addressing the grey zone for tradespeople working in client premises with high-value fixtures and fittings.

Exclusion 3, Professional Negligence and Financial Loss

PLI covers physical harm to third parties and physical damage to their property. It does not cover financial loss arising from the quality, accuracy, or suitability of your professional services or advice. That is the territory of professional indemnity insurance.

The distinction between PLI and PI claims:

| Incident | Coverage |

|---|---|

| Architect's structural design is defective → expensive remediation | Professional Indemnity |

| Architect leaves a tripod on stairs → client falls | Public Liability |

| IT developer's code has a security flaw → client data breach | Professional Indemnity |

| IT developer's laptop charger overheats → client's desk damaged | Public Liability |

| Consultant's advice leads to a wrong business decision | Professional Indemnity |

| Consultant's equipment blocks a fire exit → visitor injured | Public Liability |

Businesses that provide professional services and visit or host clients need both PLI and professional indemnity. They cover adjacent but genuinely different risks.

Exclusion 4, Deliberate or Intentional Acts

No insurance policy covers deliberate harm. A claim arising from intentional damage to a third party's property or deliberate injury to a third party is excluded from PLI and may involve police referral.

The employee misconduct grey zone:

Where an employee causes harm through reckless behaviour that was not deliberate, rough handling, aggressive working that was not meant to injure, the claim may still be covered as negligent conduct rather than intentional conduct. Insurers examine the specific circumstances of employee-caused incidents before applying this exclusion.

Exclusion 5, Gradual Pollution and Contamination

Standard PLI covers sudden and accidental pollution events, a chemical spill during transport, a fuel tank rupture affecting a neighbouring property.

It excludes gradual pollution, slow chemical leaching into the ground, persistent effluent seeping into a watercourse, accumulated dust and particulate contamination from ongoing operations.

Who this exclusion affects most: Businesses handling chemicals, solvents, oils, or materials with contamination potential, manufacturers, agricultural businesses, fuel distribution companies, construction sites using hazardous materials. These businesses need a specific environmental liability extension or standalone pollution liability policy.

Exclusion 6, Contractual Liability Beyond Legal Duty

PLI covers liability that exists independently in law, the legal duty of care owed to third parties. It does not automatically cover liability you have accepted contractually by agreeing to terms beyond your standard legal duty.

The practical risk:

A supplier who signs a client contract that includes an unlimited liability clause ("the supplier accepts unlimited liability for all loss or damage caused by its activities") has accepted contractual liability far exceeding its legal duty. A PLI policy covering up to £2m does not automatically cover unlimited contractual liability. The policy covers the underlying legal liability, the contractual excess above legal duty may not be covered.

The correct approach: Review all contracts for unusual liability clauses before signing. Never accept unlimited liability without specific legal advice and insurance that specifically covers contractual liability extension.

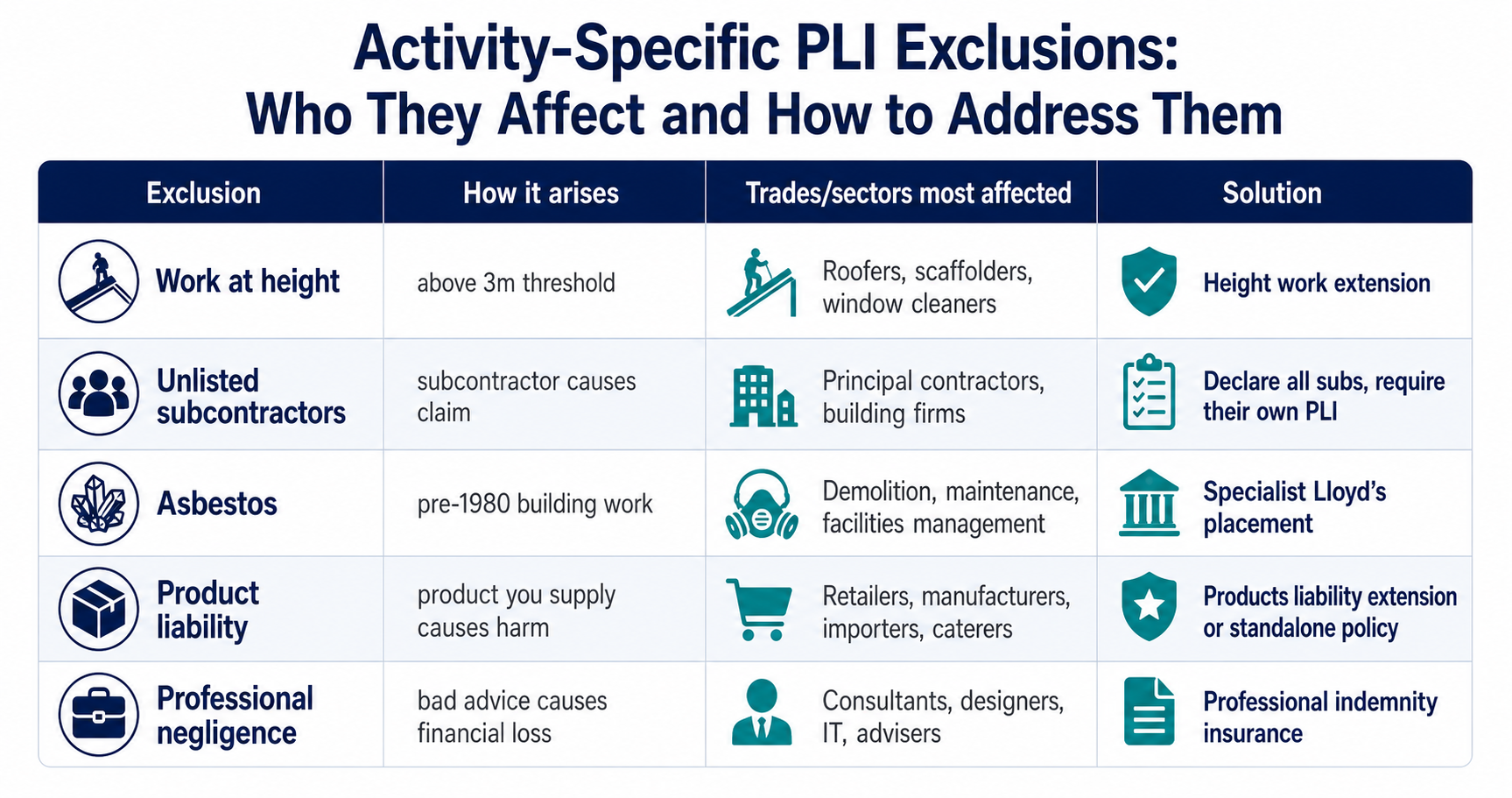

Activity-Specific Exclusions, the Ones That Catch Businesses Off Guard

Beyond the core exclusions, many PLI policies, particularly those at the lower end of the premium range, contain activity-specific exclusions that restrict coverage for certain work types.

Work at Height Above a Defined Threshold

A significant proportion of standard PLI policies exclude or restrict coverage for work performed above a defined height threshold, commonly three metres from ground level.

Who this affects: Roofers, scaffolders, aerial installers, window cleaners working on upper floors, chimney engineers, and any contractor working at elevation.

The data on height-related incidents: The Health and Safety Executive (HSE) reports that falls from height account for approximately 25% of all fatal workplace injuries in the UK. Claims arising from height-related incidents are proportionally more severe, involving serious injury, spinal trauma, and significant compensation awards.

How to address this: Confirm specifically whether your PLI policy covers work at heights above three metres. Ask the insurer directly and get written confirmation if your work regularly involves heights. Specialist contractor insurers provide height work coverage explicitly, it is not an unusual requirement.

Unlisted Subcontractors

Standard PLI policies frequently exclude claims arising from activities of subcontractors who are not listed on the policy or who do not hold their own valid PLI.

The principal contractor risk:

As a principal contractor, when a subcontractor you engaged causes a third-party incident, the third party typically pursues the claim against you. If your PLI excludes the subcontractor's activities, you face the claim personally.

The correct approach:

- Require all subcontractors to hold their own PLI and provide certificates

- Declare all subcontractor engagement at application

- Confirm your policy covers principal contractor liability for subcontractor activities

- Check certificates have not expired before each project begins

Asbestos-Related Claims

Most standard PLI policies contain a blanket asbestos exclusion. This matters for tradespeople working on pre-1980s properties, demolition contractors, and facilities management companies in older building stock. Specialist asbestos liability coverage is available through Lloyd's syndicates and specialist brokers.

Products You Manufacture or Supply

PLI covers your activities and presence. If your business manufactures, imports, or sells physical products that cause harm to a third party, that is product liability, a separate coverage that must be specifically added or purchased as a standalone policy.

Many combined small business PLI policies include product liability as a bundled extension. Check whether "products liability" or "goods supplied" appears in your current policy before assuming you are covered.

What Voids a PLI Policy, the Difference Between Exclusions and Voidance

An exclusion means a specific claim is not covered. Policy voidance is more severe, it means the insurer treats the entire policy as if it never existed, potentially seeking recovery of any claims already paid.

Non-disclosure of material facts: If you fail to disclose information at application that would have affected the insurer's decision to provide cover or the terms they would have applied, the insurer can void the policy. Material facts include: claims history, prior policy cancellations, health and safety convictions or prosecutions, and specific high-risk activities not disclosed in the activity description.

Material change of risk not notified mid-policy: If your business changes significantly during the policy year, substantially higher turnover, expansion into new high-risk activities, a serious incident that has not yet resulted in a formal claim, and you fail to notify the insurer, they may treat the policy as void for claims arising after the material change.

Fraud: Making a fraudulent claim or providing false information to inflate a settlement voids the policy and may result in criminal prosecution. Insurers share fraud data through the Insurance Fraud Bureau (IFB) and the Motor and Non-Motor Insurance Database.

The Five Checks That Prevent Exclusion-Related Claim Disputes

Check 1: List your three highest-risk activities in specific terms. Confirm each is covered by your policy's activity description.

Check 2: Identify any subcontractors you engage. Confirm your policy covers principal contractor liability and require subcontractors to provide their own PLI certificates.

Check 3: Note the highest point above ground at which you work. Confirm whether your policy has a height restriction and whether that threshold applies to your work.

Check 4: Review all client contracts for unusual liability clauses. Confirm your PLI's contractual liability position before signing.

Check 5: Read the exclusions section, pages 8–22 of the policy wording, not just the summary. Spend 15 minutes on exclusions before purchase; this is the most effective single action for avoiding claim disputes.