The gap between the cheapest and most expensive public liability insurance for UK businesses is not small and it is not arbitrary. A remote freelance designer pays £62 per year. A construction contractor with five employees pays £650. Both hold £2m of PLI. The tenfold difference reflects the underwriter's actuarial assessment of the probability and potential severity of a claim from each business type. Understanding what drives that assessment tells you where your business sits in the range, and what levers you can pull to influence it.

2026 Public Liability Insurance Premiums by Business Type

Professional Services and Office-Based Businesses

| Business Type | £1m Cover | £2m Cover | £5m Cover |

|---|---|---|---|

| Freelance copywriter / content writer | £58–£92 | £78–£125 | £105–£172 |

| Graphic designer | £62–£98 | £82–£135 | £110–£185 |

| Web developer (remote) | £65–£105 | £86–£142 | £115–£195 |

| IT contractor (on-site client visits) | £92–£160 | £122–£215 | £163–£295 |

| Business coach / trainer | £82–£138 | £108–£185 | £145–£252 |

| Management consultant | £88–£148 | £116–£198 | £155–£272 |

| HR consultant | £75–£122 | £99–£162 | £132–£222 |

| Accountant / bookkeeper | £70–£115 | £92–£155 | £123–£212 |

Retail, Hospitality and Personal Services

| Business Type | £1m Cover | £2m Cover | £5m Cover |

|---|---|---|---|

| Small retail shop (under £200k turnover) | £110–£188 | £145–£252 | £193–£345 |

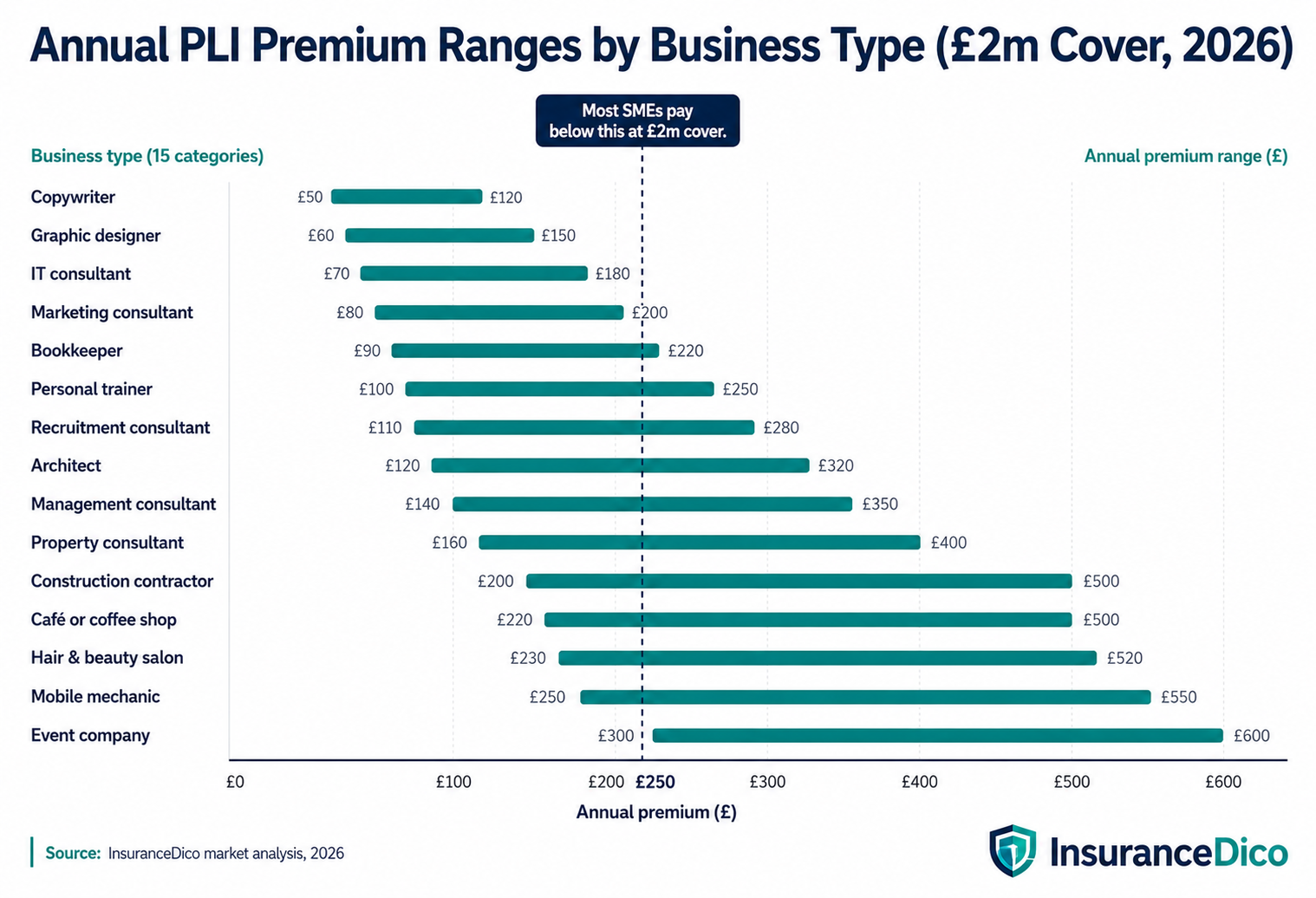

| Café or coffee shop | £128–£218 | £168–£290 | £225–£398 |

| Hair salon or barbershop | £105–£180 | £138–£240 | £185–£330 |

| Beauty salon (treatments) | £118–£200 | £155–£268 | £208–£368 |

| Personal trainer (outdoor / home visits) | £118–£202 | £155–£270 | £208–£370 |

| Market trader / craft fair | £105–£178 | £138–£238 | £185–£328 |

| Mobile caterer | £132–£225 | £174–£300 | £232–£412 |

Trades and Construction

| Business Type | £1m Cover | £2m Cover | £5m Cover |

|---|---|---|---|

| Painter and decorator | £118–£200 | £155–£268 | £208–£368 |

| Carpenter / joiner | £128–£215 | £168–£288 | £225–£395 |

| Plumber (domestic) | £148–£250 | £195–£335 | £260–£458 |

| Electrician (domestic) | £158–£265 | £208–£355 | £278–£485 |

| Landscaper / gardener | £130–£220 | £170–£295 | £228–£405 |

| General builder (domestic) | £188–£318 | £248–£428 | £330–£585 |

| Roofer | £215–£365 | £282–£488 | £378–£668 |

| Event company | £202–£385 | £265–£515 | £355–£705 |

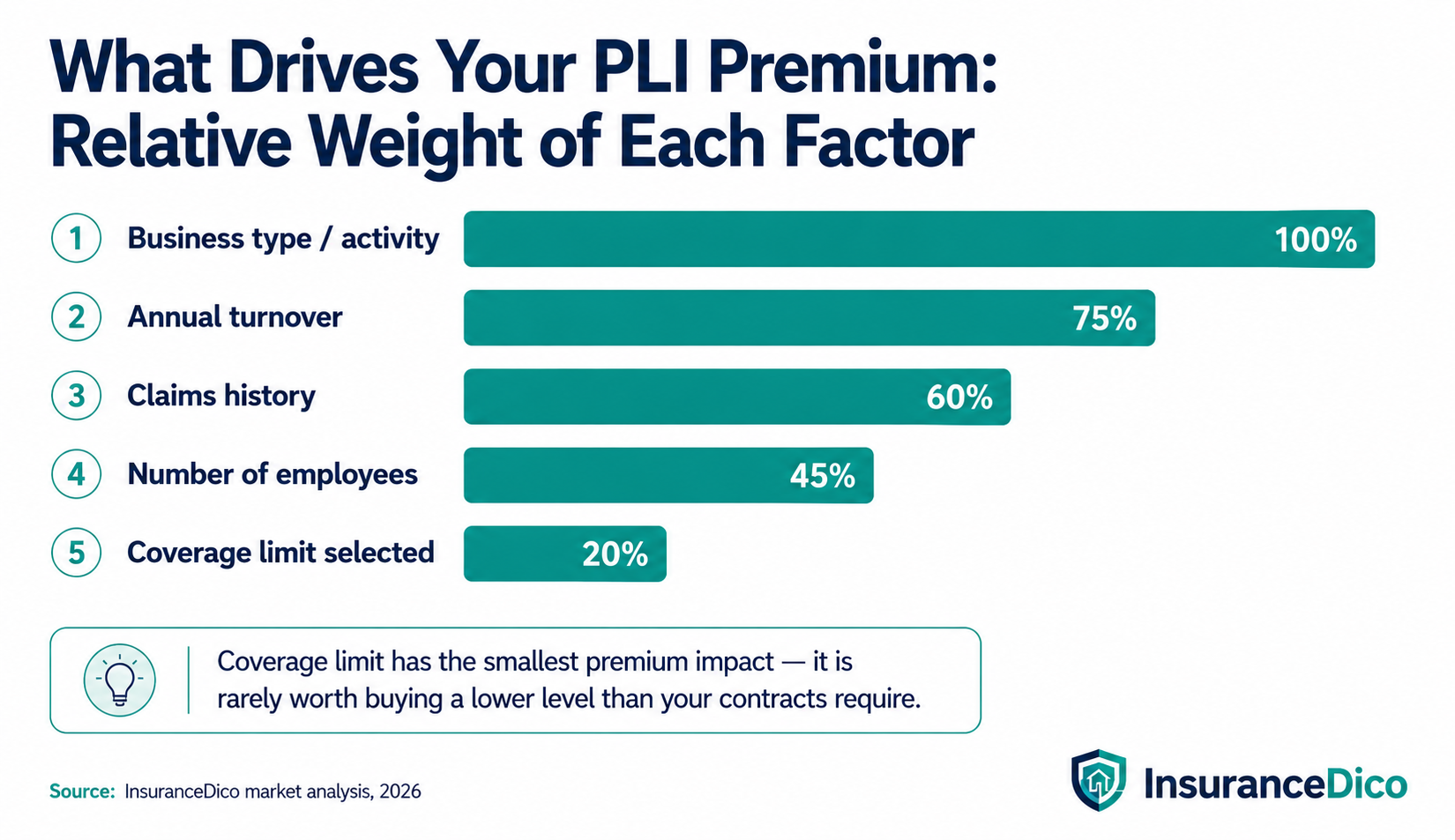

The Five Factors That Determine Your Premium

Factor 1, Business Type and Activity Classification (Highest Weight)

The nature of what your business does, and specifically the activities you declare at application, is the largest single driver of your PLI premium. Underwriters classify businesses into risk tiers based on the probability of a third-party incident. The hierarchy runs from lowest to highest risk:

- Remote professional services (no physical client interaction)

- Client-facing professional services (meetings, presentations, site visits)

- Retail and hospitality with public premises

- On-site trade work in client properties (plumbing, electrical, decorating)

- High-risk trade work (roofing, scaffolding, demolition, work at height)

- Events, crowds, and public assembly

Your declared activities must accurately reflect what your business actually does. An IT contractor who primarily works remotely but occasionally visits client offices should not declare "remote IT consultancy only." Undisclosed activities are not covered, if the incident arises from an activity you did not declare, the policy may not respond.

Factor 2, Annual Turnover (Second Highest Weight)

Turnover acts as a proxy for exposure scale. A cleaning business with £40,000 annual turnover operates fewer sites with fewer staff than one with £200,000 turnover. More operations mean more opportunities for a third-party incident. Most insurers tier premiums by turnover bracket:

- Under £50,000

- £50,001–£100,000

- £100,001–£250,000

- £250,001–£500,000

- Above £500,000

The premium step between turnover brackets is typically 15–30% for the same business type and coverage level. Declaring your turnover accurately at application and at renewal is essential, understating turnover to reduce premiums is material non-disclosure.

Factor 3, Coverage Limit (Small Relative Impact)

The premium difference between coverage levels is smaller than most buyers expect, reflecting the low statistical probability that any single claim will approach the coverage limit:

- £1m to £2m: approximately £20–£50 additional per year for most business types

- £2m to £5m: approximately £50–£120 additional per year

- £5m to £10m: approximately £80–£200 additional per year

Given how modest the incremental premium is, businesses pursuing commercial or public sector contracts should buy at the level their clients require, not at the cheapest available level.

Factor 4, Claims History (Loaded Specifically)

All claims in the past five years are disclosed at application and checked against the Claims and Underwriting Exchange (CUE) database. Claims that were not paid out (groundless claims, claims withdrawn by the claimant) still appear on CUE and must be disclosed.

| Claims Scenario | Typical Premium Loading |

|---|---|

| No claims in past 5 years | Standard rate |

| 1 small claim (under £5,000) settled | 20–45% loading for 3 years |

| 1 medium claim (£5,000–£25,000) | 40–80% loading for 4–5 years |

| 1 large claim (above £25,000) | 60–150% loading, possible referral to specialist market |

| Multiple claims in 5 years | Specialist market placement likely required |

Factor 5, Number of Employees and Subcontractors

Each employee or regular subcontractor is an additional source of third-party exposure. Premium bands typically distinguish between:

- Sole trader (no staff)

- 1–3 employees

- 4–9 employees

- 10+ employees

Adding employees increases your declared headcount and triggers a higher premium band. The increase is proportionally smaller at lower headcounts (adding a second employee has more impact than adding a tenth) because the base risk already assumes some public interaction.

How to Reduce Your PLI Premium Without Reducing Coverage

Increase Your Voluntary Excess

Your total excess is the amount you pay toward each claim before the insurer contributes. Increasing from a £250 total excess to £500 reduces premiums by 10–18% at most insurers. Increasing to £1,000 can save 20–30%.

Set your excess at the highest level your business can absorb from readily accessible cash flow. An excess that would cause cash flow problems if a claim arose negates the purpose of holding insurance. For most small businesses, £500 is a manageable excess that produces meaningful premium savings.

Bundle Policies

Purchasing PLI as part of a combined business insurance package, alongside professional indemnity and employers liability, reduces the combined premium by 15–25% versus purchasing each policy separately.

All major UK business insurers (Hiscox, AXA Business, Aviva, Simply Business, Zurich) offer combined SME packages with a single renewal date and policy schedule. For businesses that need more than one type of cover, bundling is the most straightforward cost reduction available.

Pay Annually

Monthly payment plans embed an implicit interest charge, typically 15–25% APR equivalent built into the instalment structure. A £180 annual premium paid monthly typically costs £200–£220 over 12 months. Annual payment avoids this cost entirely.

Maintain a Claims-Free Record

Five consecutive years without a fault claim earns no-claims discounts at most insurers, typically 20–35% below standard rates. Avoid making small claims where the net benefit (claim amount minus excess) is marginal and the three-to-five-year premium loading would exceed the net benefit.

For a claim where the payout net of excess is £250–£400, calculate the loading over three years before deciding whether to claim. In most cases, self-funding small incidents and preserving your no-claims record produces better financial outcomes over a three-year horizon.

Review Declared Turnover Annually

If your business has experienced a revenue decline, ensure your declared turnover at renewal reflects your current trading, not a historical peak. Overpaying a premium based on outdated higher turnover figures is wasted cost. Most insurers allow mid-term adjustments if turnover falls materially during a policy year.