Income protection insurance pays a tax-free monthly income, typically 50–70% of your gross earnings, if illness or injury prevents you from working. Unlike critical illness cover, which pays on specific diagnoses, income protection covers any condition that stops you doing your job, including mental health conditions, back problems, and chronic illness. Statutory sick pay is £116.75 per week for a maximum of 28 weeks. For most UK workers, income protection is the most underowned form of personal insurance relative to the financial exposure it covers.

Income protection insurance is a UK long-term protection policy that pays a regular, tax-free monthly benefit, typically 50–70% of pre-disability gross earnings, after a chosen deferred period, for as long as illness or injury prevents the policyholder from performing their own occupation.

The Financial Gap Income Protection Fills, With Real Numbers

The UK's statutory safety net for illness is narrower than most people realise until they need it.

Statutory sick pay (SSP) 2026: £116.75 per week, payable for a maximum of 28 weeks. After 28 weeks, SSP stops entirely. You are entitled to Universal Credit only if you meet the eligibility criteria.

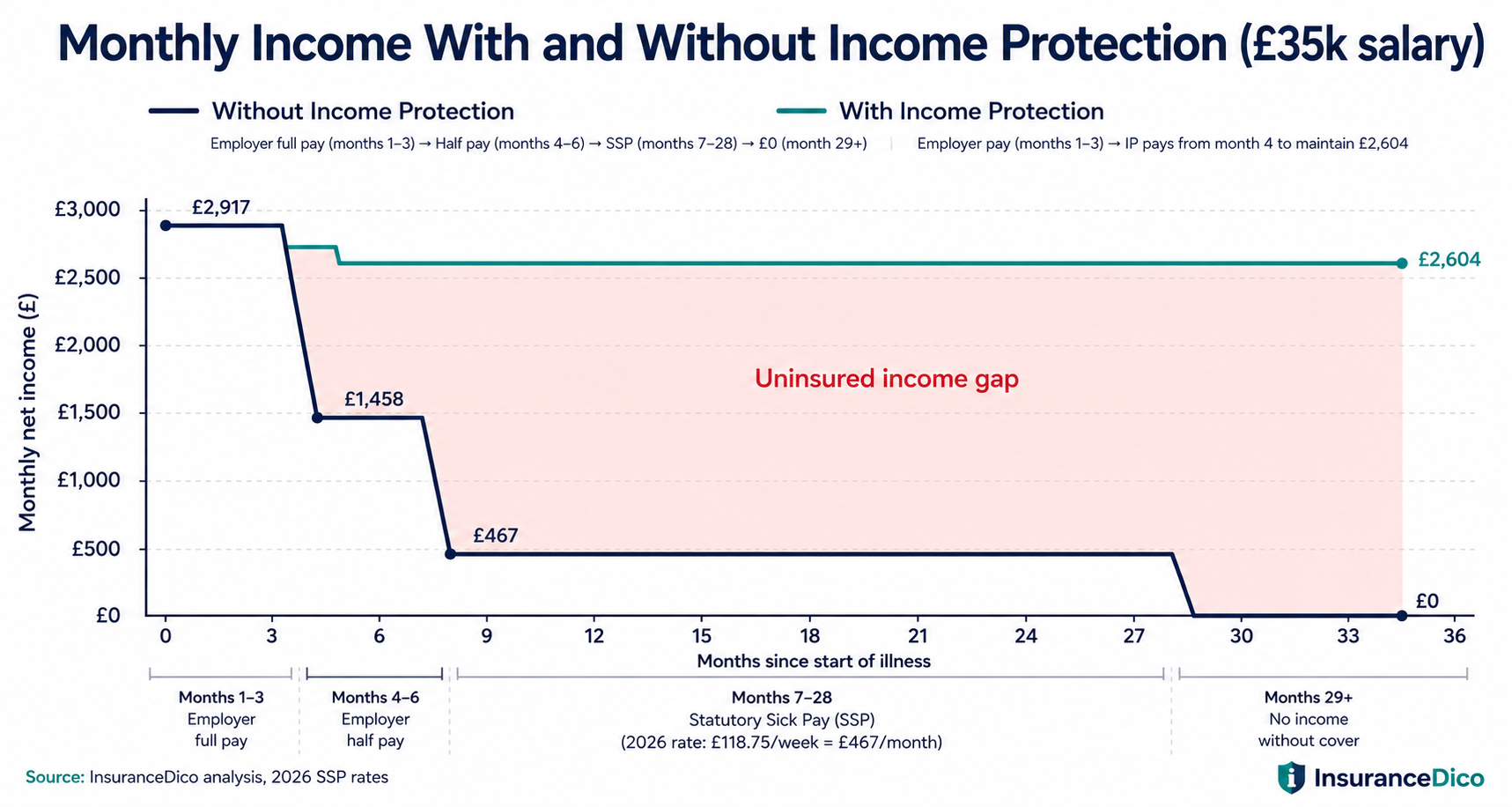

For someone earning £35,000 per year (£2,917 per month), SSP provides £467 per month, 16% of their normal take-home pay. After 28 weeks it falls to zero.

Employer sick pay: Many employers provide enhanced sick pay above SSP, but terms vary significantly. Common patterns include: full pay for 1–3 months, half pay for 3–6 months, then SSP only. After the employer sick pay period ends, most employees drop to SSP only regardless of how long they remain unable to work.

| Scenario | Monthly Income Without IP | Monthly Income With IP |

|---|---|---|

| Month 1–3 (employer full sick pay) | £2,917 | £2,917 (IP deferred, not yet paying) |

| Month 4–6 (employer half pay) | £1,458 | £2,604 (IP pays £1,146 top-up) |

| Month 7–28 (SSP only) | £467 | £2,604 (IP pays £2,137) |

| Month 29+ (no SSP, no employer pay) | £0 | £2,604 (IP pays in full) |

The gap is most severe for self-employed workers, who are not entitled to SSP at all. A self-employed individual who cannot work has zero statutory income from day one of illness.

How Income Protection Insurance Works, the Four Key Variables

Variable 1, Definition of Incapacity (the Most Important)

The incapacity definition determines what health circumstances trigger the policy to pay. There are three standard definitions, and the difference between them is material:

Own occupation: The policy pays if you cannot perform the specific duties of your own job. A surgeon with a hand tremor who cannot operate but could theoretically do desk work would receive the full income protection benefit under an own occupation policy. This is the broadest and most beneficial definition, and the most expensive.

Suited occupation: The policy pays if you cannot perform work suited to your experience, education, and training. The surgeon with a hand tremor might be expected to perform medical education, consulting, or administrative medical roles under a suited occupation definition, reducing or eliminating the payout.

Any occupation: The policy pays only if you are incapable of performing virtually any work whatsoever. In practice, this definition pays only in severe cases of total incapacity. For most conditions that prevent someone doing their actual job but leave them capable of some activity, this definition does not pay.

The correct choice for most buyers: Own occupation provides the coverage that reflects the practical reality of illness, it pays when you cannot do your job, not when you are incapable of any human activity. Suited and any occupation definitions are significantly cheaper but provide coverage that is much narrower than the headline suggests.

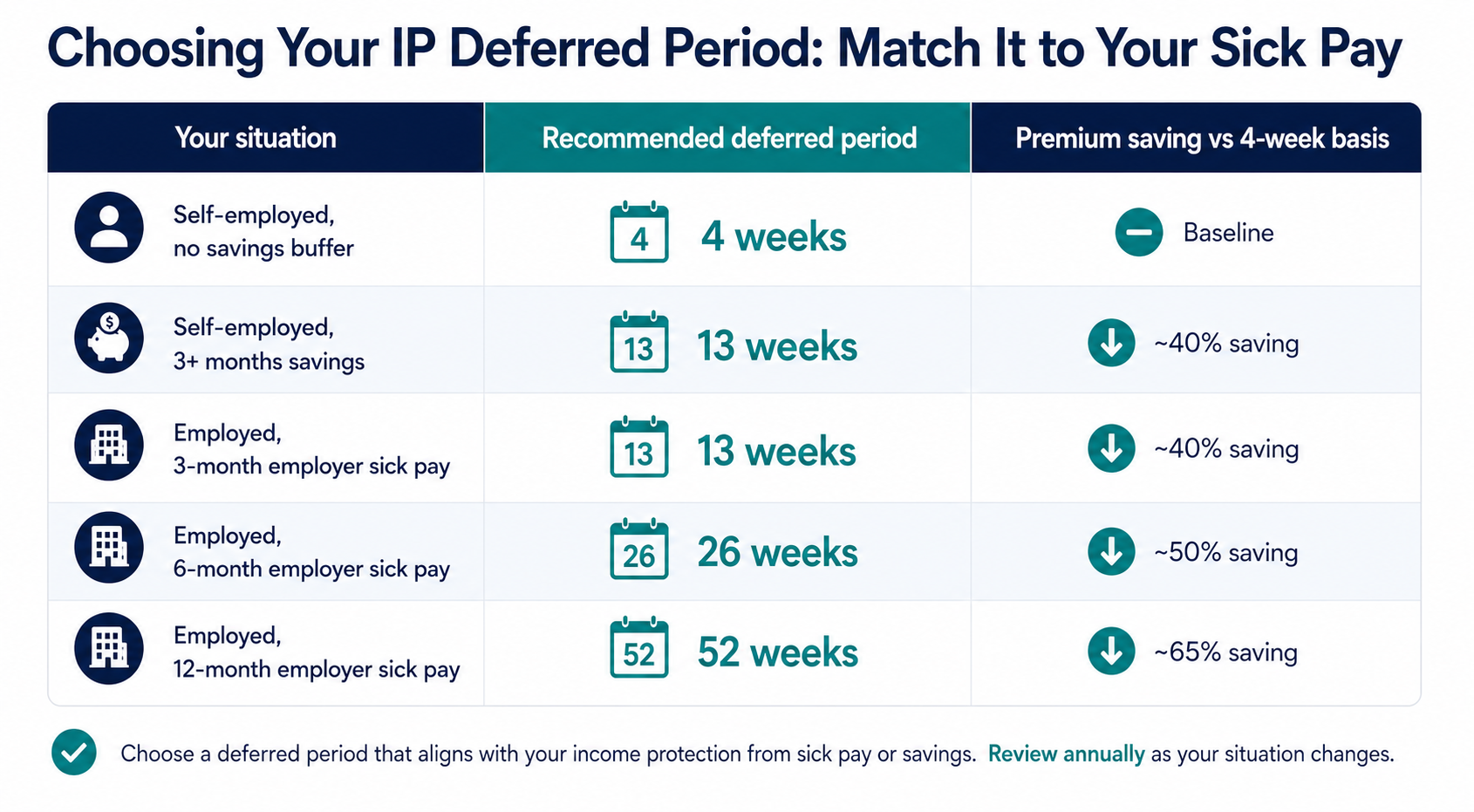

Variable 2, The Deferred Period

The deferred period is the waiting time between becoming unable to work and the first income protection payment. Standard options are: 4 weeks, 13 weeks, 26 weeks, and 52 weeks.

The deferred period should be set to match your financial runway, the period for which employer sick pay, savings, or other income can sustain your household without IP support.

| Deferred Period | Relative Premium vs 4-Week Basis | Best Matched To |

|---|---|---|

| 4 weeks | 100% (baseline) | No employer sick pay, no savings buffer |

| 13 weeks | Approx. 55–65% | Employer pays full salary 3 months, then stops |

| 26 weeks | Approx. 40–50% | Employer pays enhanced sick pay 6 months |

| 52 weeks | Approx. 30–38% | Employer pays full or enhanced sick pay 12 months |

A 26-week deferred period cuts the IP premium by approximately 50% versus a 4-week deferred period for the same benefit level. For employed individuals whose employer provides 6 months of full or enhanced sick pay, a 26-week deferred period is the economically optimal choice, it avoids the duplication of receiving both employer sick pay and IP in the first 6 months.

Variable 3, Benefit Level and Basis

Income protection pays a percentage of pre-disability earnings. HMRC-compliant IP policies pay a maximum of approximately 70% of gross earnings, this is the regulatory ceiling that prevents income protection paying more than working (which would remove the financial incentive to return to work).

Individual IP: Based on the policyholder's own earnings. Benefit is fixed at application and reviewed only if the policyholder requests indexation. Does not automatically adjust for salary increases without an escalation clause.

Indexed IP (with escalation): Benefit amount increases annually in line with RPI or CPI or by a fixed percentage (commonly 3–5%). This ensures the real value of the benefit does not erode through inflation during a long claim. Particularly important for long-term conditions, a claim lasting 7 years at a fixed £2,000 per month has 7 years of inflation eroding its real value.

Short-term IP vs long-term IP: Short-term income protection pays for a maximum of 12 or 24 months per claim. It is significantly cheaper than long-term IP but leaves you without income if a condition prevents work for longer. Long-term income protection pays from the end of the deferred period until you return to work, retire, or die, whichever comes first. The average IP claim lasts 7 years (Legal & General). Short-term IP is not adequate for most serious conditions.

Variable 4, Policy Basis: Guaranteed vs Reviewable Premiums

Guaranteed premiums: Fixed at the start and cannot be increased by the insurer for any reason during the policy term. Provides certainty of cost, your IP premium at 60 is the same as at 30 if you bought the policy at 30.

Reviewable premiums: Start lower but can be increased at defined review intervals based on the insurer's claims experience in the portfolio. Over a 30-year policy, reviewable premiums frequently end up costing more than guaranteed premiums would have, while providing less certainty.

For long-term IP, a policy you intend to hold until retirement, guaranteed premiums are the preferred basis for most buyers.

2026 Income Protection Insurance Cost

IP premiums are driven by: age, occupation (risk of the specific job), deferred period, benefit level, policy term, smoker status, health history, and whether the premium is guaranteed or reviewable.

| Age | Deferred 4 Weeks | Deferred 13 Weeks | Deferred 26 Weeks |

|---|---|---|---|

| 25 | £28–£55 | £16–£32 | £12–£23 |

| 30 | £36–£70 | £20–£41 | £15–£30 |

| 35 | £48–£94 | £27–£55 | £20–£41 |

| 40 | £68–£133 | £38–£78 | £28–£58 |

| 45 | £98–£192 | £55–£112 | £41–£83 |

| 50 | £148–£290 | £83–£169 | £62–£127 |

Occupation classes and their premium impact: Insurers classify occupations by risk category, typically Class 1 (lowest risk, office-based professionals) through Class 4 (highest risk, manual workers in hazardous environments). Some occupations are declined for long-term IP (commercial divers, explosives workers, professional sports players in contact sports). Class 1 and Class 2 occupations attract the most favourable premiums. Manual trades typically attract Class 3 or 4 loadings.

What Income Protection Does Not Cover

Pre-existing conditions: Any condition you had before the policy started may be excluded, either as a blanket exclusion for any related claim, or through specific condition exclusions applied during underwriting. Exclusions can be temporary (excluded for the first two years of the policy) or permanent.

Pregnancy and maternity: Standard IP policies exclude normal pregnancy and maternity, these are not illnesses. Complications of pregnancy that prevent work beyond maternity leave may be covered depending on policy wording.

Unemployment: Income protection covers inability to work due to illness or injury. It does not cover redundancy, resignation, or voluntary cessation of work. Payment protection insurance (PPI), a different and now largely discredited product, was designed for unemployment.

Self-inflicted conditions and substance misuse: Standard exclusions across all IP products.

Conditions arising from hazardous activities: Many IP policies exclude or restrict claims arising from extreme sports, hazardous pastimes, or activities you were not medically fit for. Declare all relevant activities at application.