Life insurance with pre-existing medical conditions is available in the UK for the majority of conditions, including type 2 diabetes, treated hypertension, depression, most cancers in remission and many heart conditions. The underwriting outcome is one of three: standard terms (no loading), rated terms (a higher premium reflecting the additional risk), or a specific exclusion. Only a small minority of serious or unstable conditions result in a decline. The key is applying through the right channel, the standard comparison-site market does not access Lloyd's or specialist impaired-life underwriters.

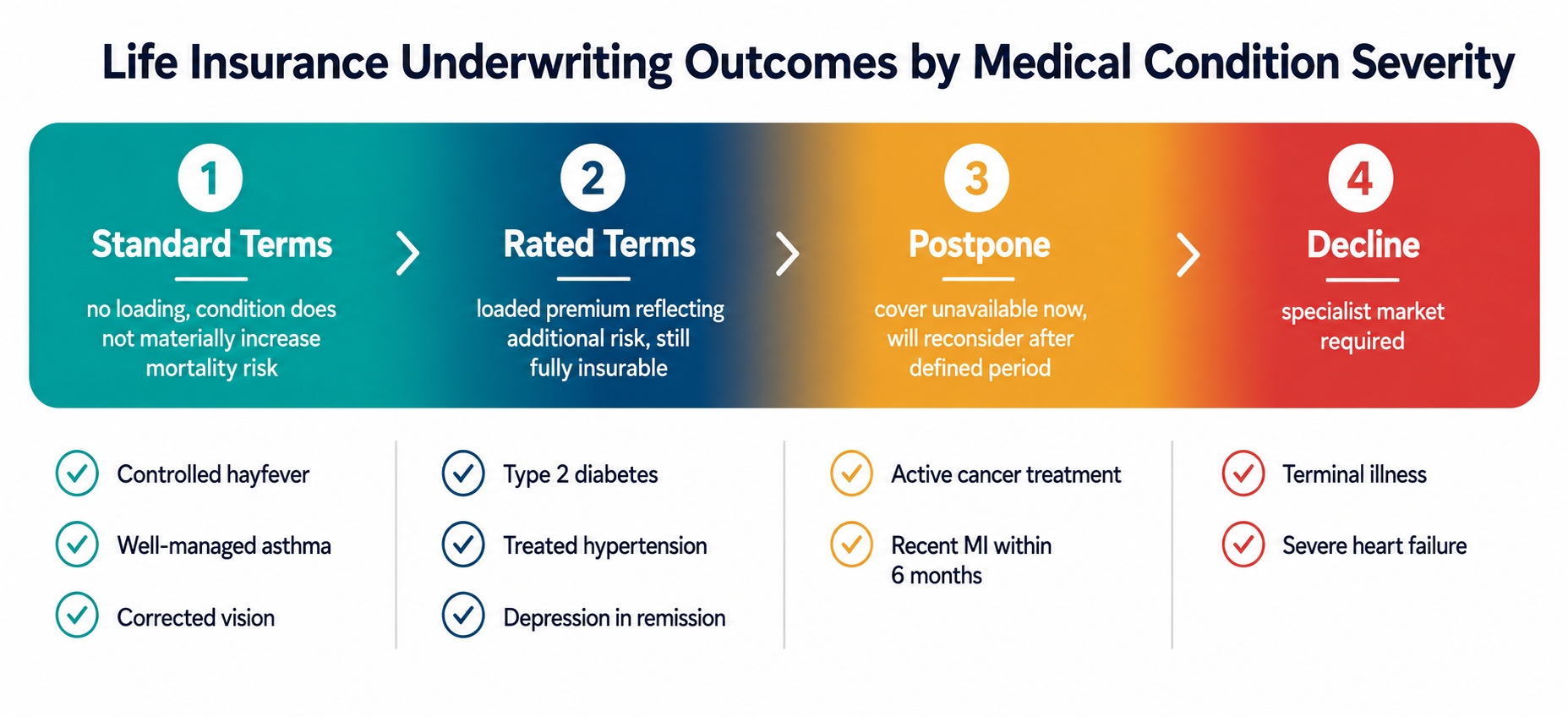

Life insurance pre existing conditions underwriting is the UK insurer process that assesses any medical condition diagnosed before application and assigns one of four outcomes, standard terms, rated (loaded) terms, postpone, or decline, based on severity, current status, treatment and time since diagnosis.

Most Conditions Do Not Prevent You Getting Life Insurance

The most damaging belief about life insurance with pre-existing conditions is binary: either you have a condition and cannot get cover, or you do not and can. This is incorrect. The realistic picture is a spectrum of five outcomes.

Standard terms: Your condition is well-managed, stable, and does not significantly alter your statistical mortality risk relative to the general population. Premiums are at standard rates.

Rated terms (loaded premium): Your condition increases your statistical mortality risk above the standard population. The insurer offers cover at a higher premium, the loading reflects the additional risk they are accepting. Most common conditions that require medical management fall here.

Exclusion: Cover is offered, but death caused by the specific condition is excluded. More common in critical illness underwriting than life insurance, life insurance exclusions of specific causes of death are less common than premium loadings.

Postpone: The insurer will not offer terms immediately but will reconsider after a defined period, typically after a cancer treatment course is complete or after a cardiac event has been stable for 12–24 months.

Decline: Cover is refused at this time. Less common than most applicants fear. A decline from a standard insurer does not mean cover is unavailable, specialist impaired-life markets exist specifically for declined risks.

How Life Insurance Underwriting Assesses Medical Conditions

When you apply for life insurance and disclose a medical condition, the underwriter assesses four factors:

Severity and current status: Is the condition active, managed, or in remission? An active cancer is treated differently from a cancer in 10-year remission. Controlled hypertension is treated differently from hypertension with end-organ damage.

Treatment and compliance: Are you following prescribed treatment? Is the condition well-managed? HbA1c levels for diabetics, blood pressure readings for hypertensive applicants, and psychiatric medication compliance for mental health applicants all inform the underwriting decision.

Time since diagnosis or treatment: Many conditions are loadable at diagnosis but become insurable at standard or loaded terms after a defined period of stability. Time since a cardiac event, time since cancer treatment, and time since a mental health episode all reduce the underwriting loading as risk diminishes with time.

Family history: Some conditions have hereditary components that affect underwriting even before personal diagnosis, particularly cardiovascular disease and certain cancers.

Condition-by-Condition Guide, What to Expect at Underwriting

Type 2 Diabetes

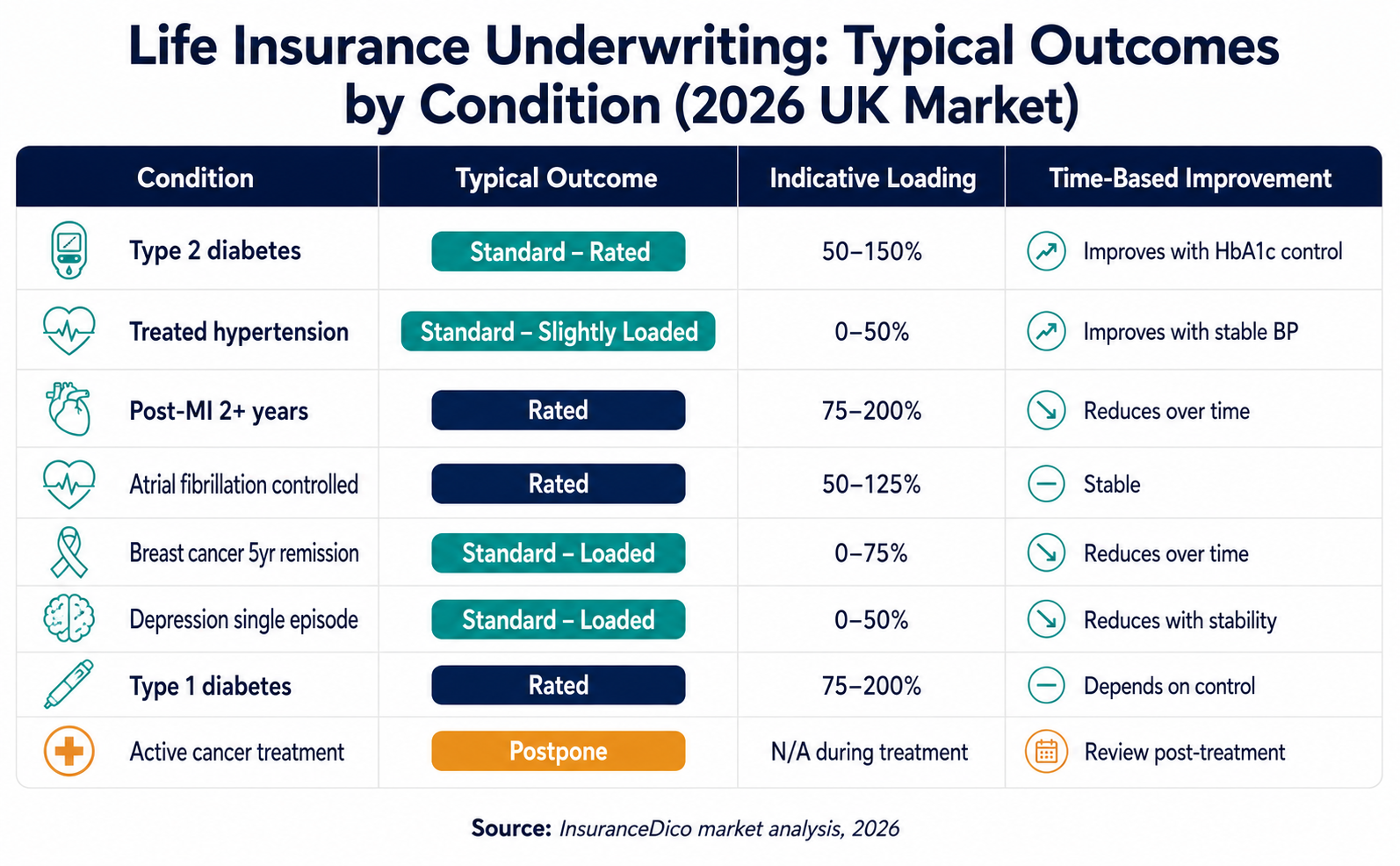

Type 2 diabetes is one of the most commonly disclosed conditions in UK life insurance applications, approximately 4.4 million people in the UK are diagnosed with diabetes.

Standard terms: Rarely. Well-controlled type 2 diabetes with an HbA1c below 6.5% and no complications may achieve standard terms at some insurers.

Rated terms: The most common outcome. Premium loadings depend on age at diagnosis (younger diagnosis = higher loading, reflecting longer duration of risk), HbA1c control (values above 8.5% typically produce larger loadings), presence of complications (neuropathy, retinopathy, nephropathy each increase the loading materially) and BMI (obesity combined with diabetes produces compounding loadings).

Indicative loading range for well-managed type 2 diabetes: 50–150% above standard premium depending on age, HbA1c and complication profile.

What improves your outcome: Evidence of active management, regular GP reviews, HbA1c within target, medication compliance, and no diabetes-related hospital admissions in recent years.

Cardiovascular Conditions, Heart Attack, Angina, Atrial Fibrillation

Heart attack (myocardial infarction): Applications within 6–12 months of a heart attack are typically postponed. Applications 12–24 months post-MI where recovery is complete and cardiac function has returned to near-normal may be accepted at significant loadings. Applications 5+ years post-MI with good cardiac function often attract moderate loadings only.

Angina: Well-controlled stable angina with current medication typically attracts a moderate loading. Unstable angina or angina requiring recent revascularisation (stent, bypass) is more heavily loaded or postponed.

Atrial fibrillation: AF that is rate-controlled or rhythm-controlled with anticoagulation and without additional cardiovascular risk factors typically attracts a moderate loading. AF with associated heart failure or stroke history produces higher loadings.

Hypertension

Treated hypertension with blood pressure controlled to within normal range (typically below 140/90 mmHg) on medication is insurable at standard or modestly loaded terms at most insurers. The BP reading on application date matters, applications with elevated readings on the day attract more scrutiny.

Untreated hypertension, or hypertension with evidence of end-organ damage (hypertensive nephropathy, LV hypertrophy, retinopathy), produces heavier loadings.

Cancer

Cancer underwriting is the area of greatest complexity and most significant variation between insurers.

Cancers typically insurable at standard or loaded terms after remission: Breast cancer (typically insurable after 2–5 years of remission depending on stage and treatment), bowel cancer (typically insurable after 5 years of remission for stage I–II), cervical cancer stage I (often insurable after 2–3 years), thyroid cancer well-differentiated (often insurable at standard terms after treatment), and basal cell carcinoma (usually standard terms immediately after treatment).

Cancers with longer postponement or higher loadings: Melanoma (insurable after 5+ years remission, loading depends on staging), breast cancer stage III (typically 5+ years remission before terms offered), Hodgkin's lymphoma (typically 5+ years remission, often at standard terms), and lung cancer (rarely insurable in the standard market within 10 years of treatment).

The critical variable: Time since treatment completion and absence of recurrence. Every 12 months of recurrence-free status moves the underwriting outcome toward more favourable terms.

Mental Health Conditions

Mental health underwriting is the area most feared and most misunderstood.

Depression and anxiety (single or limited episodes, currently well): One episode of depression or anxiety with full recovery and no current medication typically achieves standard or modestly loaded terms.

Recurrent depression (multiple episodes, managed with medication): This is where outcomes diverge between insurers. Some will offer loaded terms reflecting the statistical mortality impact of recurrent depression (including elevated suicide risk in actuarial data). Others will postpone pending a defined period of stability. The loading range is wide, 25–200% above standard.

Severe or treatment-resistant mental illness: Bipolar disorder, schizophrenia, and psychotic conditions are the most challenging to insure in the standard market. Specialist Lloyd's-based underwriters have developed products for these conditions, premiums are high but cover is available.

The disclosure approach that matters: Accurate, specific and evidence-backed disclosure is the most important factor in achieving the best possible mental health underwriting outcome. Vague or defensive disclosure, "occasional low mood", is less useful than specific disclosure, "one episode of major depressive disorder in 2019, treated with sertraline for 8 months, discharged from therapy in 2020, no recurrence, no current medication."

The Specialist Market, What to Do If You Are Declined

A decline by a standard comparison-site insurer does not mean life insurance is unavailable. The standard comparison-site market accesses approximately 15–20 UK life insurers. The specialist impaired-life market, accessed through specialist brokers with Lloyd's connections, covers substantially more.

Who the specialist market serves

- Applicants declined by two or more standard market insurers.

- Conditions that standard insurers do not underwrite (severe mental illness, multiple chronic conditions, very recent serious illness).

- HIV-positive applicants, the specialist market has developed dedicated products here.

- High-risk occupations or extreme activities that affect life insurance terms.

How to access the specialist market

The British Insurance Brokers Association (BIBA) operates a signposting service for consumers who have been declined by the standard market. Specialist impaired-life brokers, including Cura Financial Services, LifeSearch and ActiveQuote's specialist division, have dedicated underwriting relationships with Lloyd's syndicates that provide impaired-life cover.

What to expect in the specialist market: Premium loadings are higher than the standard market, sometimes significantly so. Some specialist products provide lower sums insured at the outset, increasing over time as the condition demonstrates stability. Some use a modified death benefit, paying less in the early policy years and the full sum insured later.