Critical illness cover pays a tax-free lump sum if you are diagnosed with one of the serious illnesses specified in your policy. You do not have to die — you receive the payout on diagnosis and survival. UK insurers paid 91.2% of critical illness claims in 2023 according to the ABI, with cancer accounting for 61% of all claims. The average payout was £69,300. The most important variable when comparing policies is not the premium — it is the breadth of the definition of each covered condition and whether the insurer uses ABI model definitions or enhanced definitions.

Critical illness cover is a UK protection policy that pays a tax-free lump sum on diagnosis and survival of one of a specified list of serious illnesses defined in the policy wording — most commonly cancer, heart attack, and stroke.

What Critical Illness Cover Does — and Why It Is Not a Substitute for Life Insurance

Critical illness cover and life insurance serve different financial risks and must not be confused as alternatives. Life insurance pays on death, protecting your family against the permanent loss of your income. Critical illness cover pays if you are diagnosed with a specified serious illness and survive — its purpose is to protect your financial position during the period of treatment, recovery, and potential long-term incapacity, when you are alive but unable to work normally.

The financial needs they address are different:

- If you die, your family needs replacement income and mortgage protection — life insurance addresses this

- If you survive cancer surgery but cannot return to work for 18 months, your family needs a lump sum to cover the mortgage, treatment costs, home adaptations, and lost income — critical illness cover addresses this

For most families with a mortgage and dependants, both are needed. They are not substitutes — they are complements covering adjacent risks.

What Critical Illness Cover Pays — the Conditions List

The ABI Model Minimum — Seven Core Conditions

All ABI member insurers must cover at least these seven conditions using standardised definitions:

| Condition | ABI Model Definition Summary |

|---|---|

| Cancer | Definite diagnosis of a malignancy characterised by uncontrolled growth and spread of malignant cells, with a specified list of exclusions |

| Heart attack | Definite diagnosis of death of heart muscle with specific ECG, enzyme, and symptomatic criteria |

| Stroke | Defined neurological deficit persisting beyond 24 hours resulting from brain infarction or haemorrhage |

| Coronary artery bypass grafts | Undergoing surgery requiring median sternotomy for bypass grafting of two or more coronary arteries |

| Kidney failure | Permanent and irreversible failure of both kidneys requiring permanent renal dialysis or transplant |

| Major organ transplant | Undergoing transplantation as recipient of heart, lung, liver, pancreas, kidney, or bone marrow |

| Multiple sclerosis | Definite diagnosis with confirmation by a consultant neurologist and permanent neurological deficits |

Enhanced Definitions — Where Policies Differentiate

Beyond the ABI minimum, insurers compete by covering more conditions and by using broader ("enhanced") definitions of core conditions. The significance is direct: a narrower cancer definition might exclude certain early-stage cancers that a broader definition covers.

Conditions commonly added beyond the ABI minimum (varies by insurer): aorta graft surgery, blindness, coma, deafness, heart valve replacement or repair, loss of hands or feet, loss of speech, Parkinson's disease (under 65 at time of diagnosis in many policies), motor neurone disease, Alzheimer's disease (under 65), third-degree burns covering a defined body surface area, total permanent disability, HIV contracted during medical treatment, and traumatic head injury.

The definitions gap that matters most in practice: cancer is the most claimed condition — 61% of all CI claims. The cancer definition in your policy determines whether certain common cancer presentations are covered:

- Early-stage prostate cancer: Many standard policies exclude prostate cancer at an early stage (typically Gleason score below 6 or T1a/T1b staging). Enhanced definitions include lower-stage diagnoses.

- Early-stage thyroid cancer: Often excluded at T1 staging under standard definitions. Enhanced definitions include T1.

- Early-stage bladder cancer: Non-invasive (Ta/T1 grade 1) often excluded by standard definitions.

- DCIS (ductal carcinoma in situ) of the breast: Not covered as cancer by most standard definitions — though some enhanced policies pay a partial benefit.

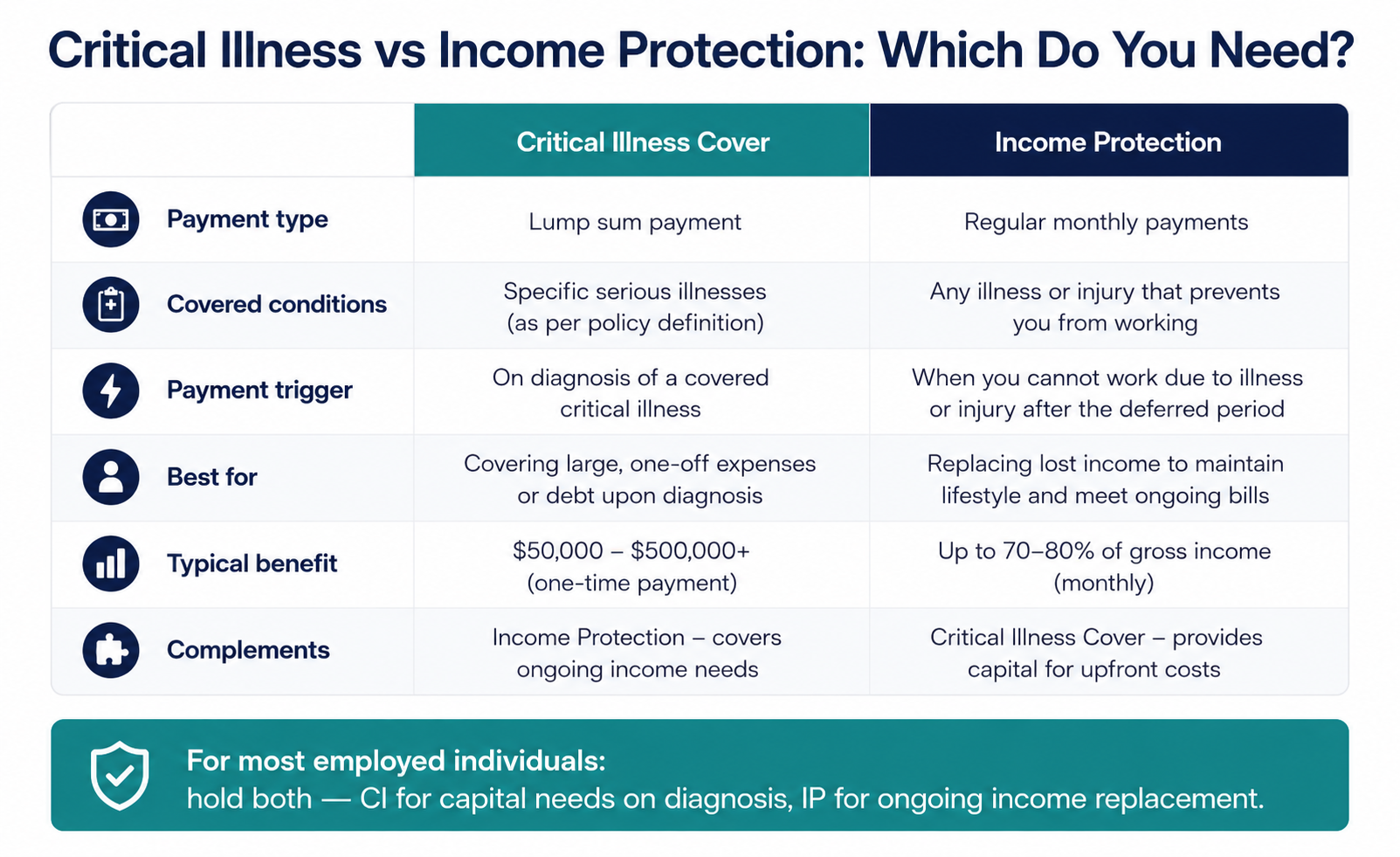

Critical Illness Cover vs Income Protection — the Decision Framework

The most common question when considering critical illness cover is whether it is better than income protection insurance. The answer depends on your financial situation.

The structural difference: Critical illness cover pays a lump sum on diagnosis of a specified condition. Income protection pays a monthly income (typically 50–70% of gross earnings) throughout the period you cannot work due to any illness or injury.

When a Lump Sum (CI) Is More Useful

- You have a mortgage you want to pay off entirely on diagnosis, eliminating the monthly payment permanently rather than covering it month by month

- You face likely treatment costs (private appointments, specialist drugs, home modifications) that are specific and quantifiable

- You want to provide for a defined financial goal — school fees for three years, repaying a specific debt — that a lump sum matches more naturally than a monthly income

When Monthly Income (IP) Is More Useful

- Your primary concern is replacing your earned income throughout a long recovery period — cancer treatment can span 18–36 months; a monthly income across this period is a better match than a single lump sum that may be spent long before recovery is complete

- You have no specific large-sum financial need — your household costs are monthly obligations, not capital requirements

- You want protection against any condition that prevents you working — not only the specific conditions on the CI list

The coverage gap in CI that IP does not have: critical illness cover only pays for conditions on the covered list. Income protection covers any illness or injury that prevents you from performing your occupation — depression, chronic back pain, recovery from minor surgery, anxiety disorders — none of which would typically trigger a CI claim.

The most common recommendation for employed individuals: hold CI cover at approximately 3–5 times annual salary to address capital needs (mortgage payoff or treatment costs) on a serious diagnosis, and hold income protection with a deferred period matching your sick pay entitlement to address ongoing income replacement. For most households these are complementary purchases that address different aspects of the same underlying risk.

2026 Critical Illness Cover Premiums

Critical illness insurance is priced using the same underwriting factors as life insurance (age, health, smoking status, occupation) with the additional dimension of which conditions are covered and how broadly they are defined.

| Age at Application | Non-Smoker | Smoker |

|---|---|---|

| 30 | £28–£52 | £52–£98 |

| 35 | £38–£72 | £72–£136 |

| 40 | £58–£110 | £110–£208 |

| 45 | £88–£168 | £166–£318 |

| 50 | £140–£268 | £265–£507 |

Why the range within an age band is wide: the premium difference within a single age band reflects the breadth of conditions covered and the definitions used. A policy with ABI minimum definitions and seven conditions costs significantly less than one covering 35+ conditions with enhanced definitions including early-stage cancers. The cheaper policy is not better value if you are diagnosed with an early-stage cancer it does not cover.

Combined life and CI cover: most individuals purchase CI cover on a "life or earlier critical illness" basis — the policy pays out either on a CI diagnosis or on death, whichever occurs first. This combined product is the standard market offering and is typically 15–25% cheaper than purchasing life and CI separately.

What Critical Illness Cover Does Not Pay — the Exclusions

Conditions not on the covered list: the policy pays only for listed and defined conditions. Chronic back pain, mental health conditions (depression, anxiety, PTSD), chronic fatigue syndrome, and musculoskeletal disorders are not typically on CI condition lists — despite being among the most common reasons people cannot work. For comprehensive disability income protection, income protection insurance is the appropriate product.

Conditions meeting a narrower definition than you experienced: a cancer diagnosis is not automatically a CI claim — the specific type and stage must meet the policy definition. Prostate cancer at an early stage, some skin cancers, and non-invasive presentations are frequently outside standard CI definitions.

Pre-existing conditions: any condition present before the policy starts — or for which you received treatment, medication, or investigation within a defined lookback period — may be excluded. The specific exclusion scope depends on underwriting outcome at application.

Survival requirement: most UK CI policies require survival for 10–14 days after diagnosis before the payout is made. If the policyholder dies within this survival period, the CI policy does not pay — but the life insurance element of a combined policy would.

Self-inflicted conditions: illness or injury directly resulting from self-inflicted harm, alcohol or drug abuse, or criminal activity are standard CI exclusions.