Whole of life insurance provides permanent coverage with a guaranteed payout whenever you die — there is no fixed term and the policy does not expire. This certainty of payout makes it more expensive than term life: a 40-year-old taking out £200,000 of whole of life cover pays approximately £120–£200 per month versus £21–£35 per month for 25-year term cover. The financial case for whole of life is strongest for inheritance tax planning — policies written in trust sit outside the estate, are not subject to the 40% IHT charge, and provide beneficiaries with funds to settle an IHT bill without selling assets. For straightforward mortgage and income protection, term life is almost always better value.

Whole of life insurance is a permanent UK protection policy that pays a guaranteed sum on death whenever it occurs, with no fixed term and no expiry date, in exchange for premiums paid for life or to a defined age.

What Whole of Life Insurance Is — the Structural Difference From Term

The defining characteristic of whole of life insurance is permanence. Unlike term life, which expires at the end of a fixed period and pays only if death occurs within that period, whole of life insurance:

- Has no expiry date — the policy remains in force for your entire life

- Pays a guaranteed sum whenever you die — at 55 or at 95

- Requires premiums to be paid for life (or to a defined age, typically 85–90)

- Does not build a cash surrender value under most modern UK whole of life products

What this means financially: the insurer is not pricing for a probability that you might die within a defined window. They are pricing for the certainty that you will die eventually and the policy will pay. This actuarial certainty — the claim will happen — is why premiums are significantly higher than equivalent term life coverage.

The Two Types of Whole of Life Policy in the UK Market

Guaranteed sum assured: the payout is fixed at the policy start and does not change. Premiums are typically guaranteed (will not be reviewed or increased by the insurer). This is the most predictable and administratively simple form.

Reviewable (unit-linked or with-profits) whole of life: the payout is linked to investment performance within the policy. The policy includes a "sum at risk" element (the insurer's exposure) and an "accumulation" element (the investment fund). At periodic review points — typically every 10 years — premiums may be increased if the investment fund has underperformed, or reduced if it has outperformed. These policies were widely sold in the 1980s and 1990s and generated significant consumer complaints when reviews produced large premium increases. Most mainstream UK insurers now focus on guaranteed sum assured products.

When Whole of Life Insurance Makes Financial Sense

The fundamental question with whole of life insurance is: do you need a guaranteed payout regardless of when you die, or do you need protection during a defined period of financial vulnerability? If the answer is a defined period — a mortgage, the years your children are dependent — term life almost always delivers more protection per pound of premium. If the answer is a guaranteed payout regardless of timing, whole of life is the appropriate product.

Scenario 1 — Inheritance Tax Planning

The UK inheritance tax (IHT) threshold is £325,000 for individuals (the nil-rate band), plus a further £175,000 residence nil-rate band where a primary residence passes to direct descendants. Estates above these thresholds are subject to 40% IHT on the excess.

For individuals or couples with estates above the IHT threshold — typically those with property, investments, pension wealth, and business interests combined — a whole of life policy written in trust provides a specific solution.

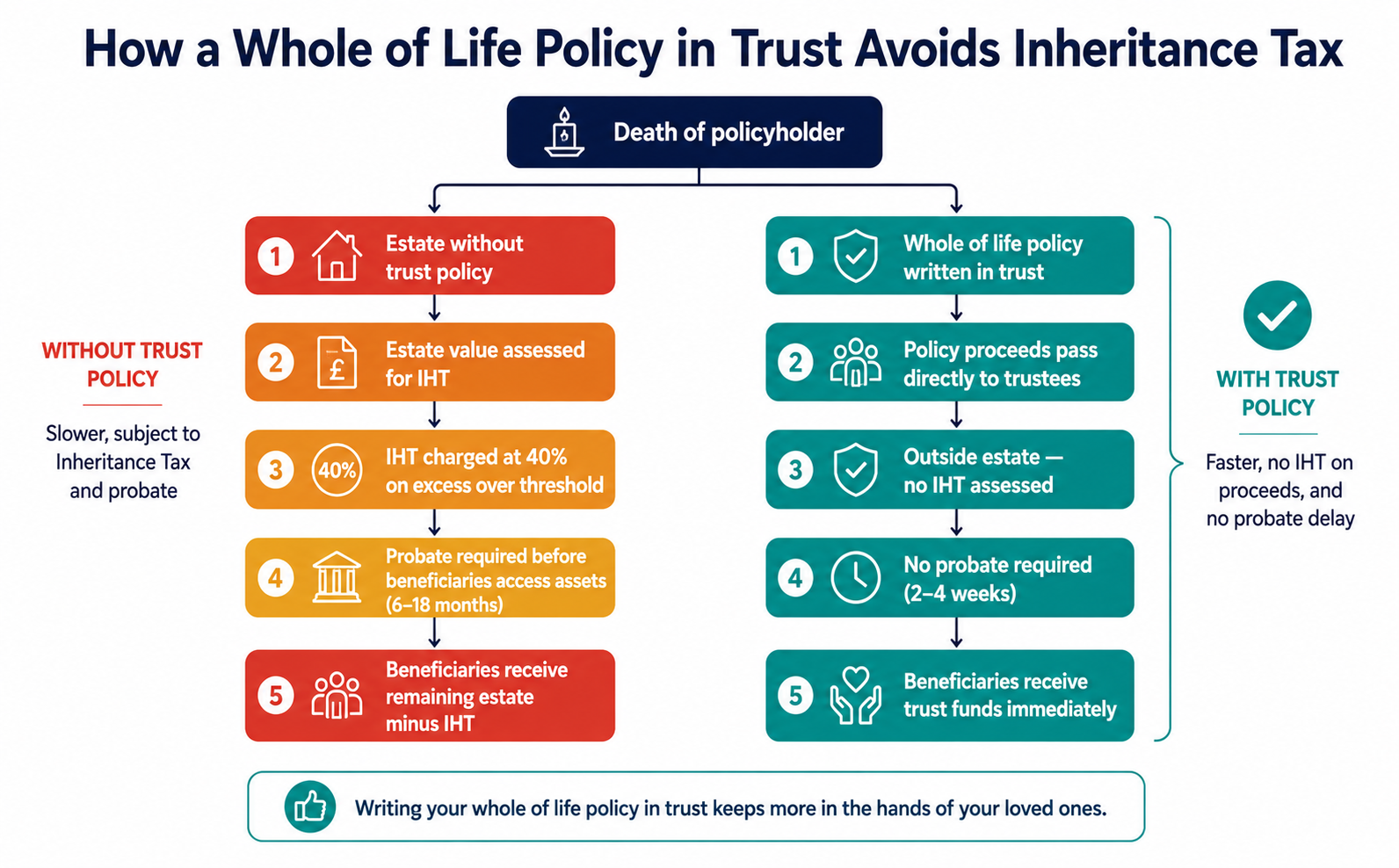

The mechanism: the policy pays a defined sum on death. Because it is written in trust, the proceeds sit outside the estate — they are not added to the estate value, are not subject to IHT, and do not require probate. The beneficiaries receive the funds quickly (typically 2–4 weeks after notification versus 6–18 months for estate administration) and can use them to pay the IHT bill without liquidating other estate assets.

The alternative without insurance: beneficiaries of a large estate must pay IHT before probate is granted. This means they cannot access estate assets to fund the IHT payment. They may need to sell property — often the family home — or borrow to fund the IHT bill. A whole of life policy in trust avoids this forced asset sale.

The sizing calculation: the policy sum should cover the expected IHT liability. For a couple with a joint estate of £1.2m and a combined nil-rate allowance of £1m, the expected IHT is £80,000 (40% of the £200,000 excess). A joint whole of life policy written in trust for £80,000 covers this liability.

Scenario 2 — Guaranteed Funeral Cost Provision

A whole of life policy with a sum insured of £10,000–£20,000 provides a guaranteed fund for funeral expenses regardless of when death occurs — without the waiting period or breakeven concerns that affect over-50s plans. Unlike over-50s plans, which have a 12–24 month waiting period, a whole of life policy written on full medical underwriting pays from day one.

The cost comparison: a 50-year-old in good health taking out £15,000 of whole of life cover (guaranteed sum, guaranteed premiums) pays approximately £35–£55 per month. An over-50s plan for the same sum for a 50-year-old costs approximately £25–£40 per month — cheaper in the near term but with a waiting period and less certainty on the total lifetime premium.

Scenario 3 — Leaving a Guaranteed Financial Gift

For individuals who want to guarantee a specific financial amount passes to named beneficiaries — a grandchild's inheritance, a charitable donation, a gift to a non-dependent family member — whole of life insurance in trust provides certainty that term life does not. Term life only pays if death occurs within the term. Whole of life pays unconditionally.

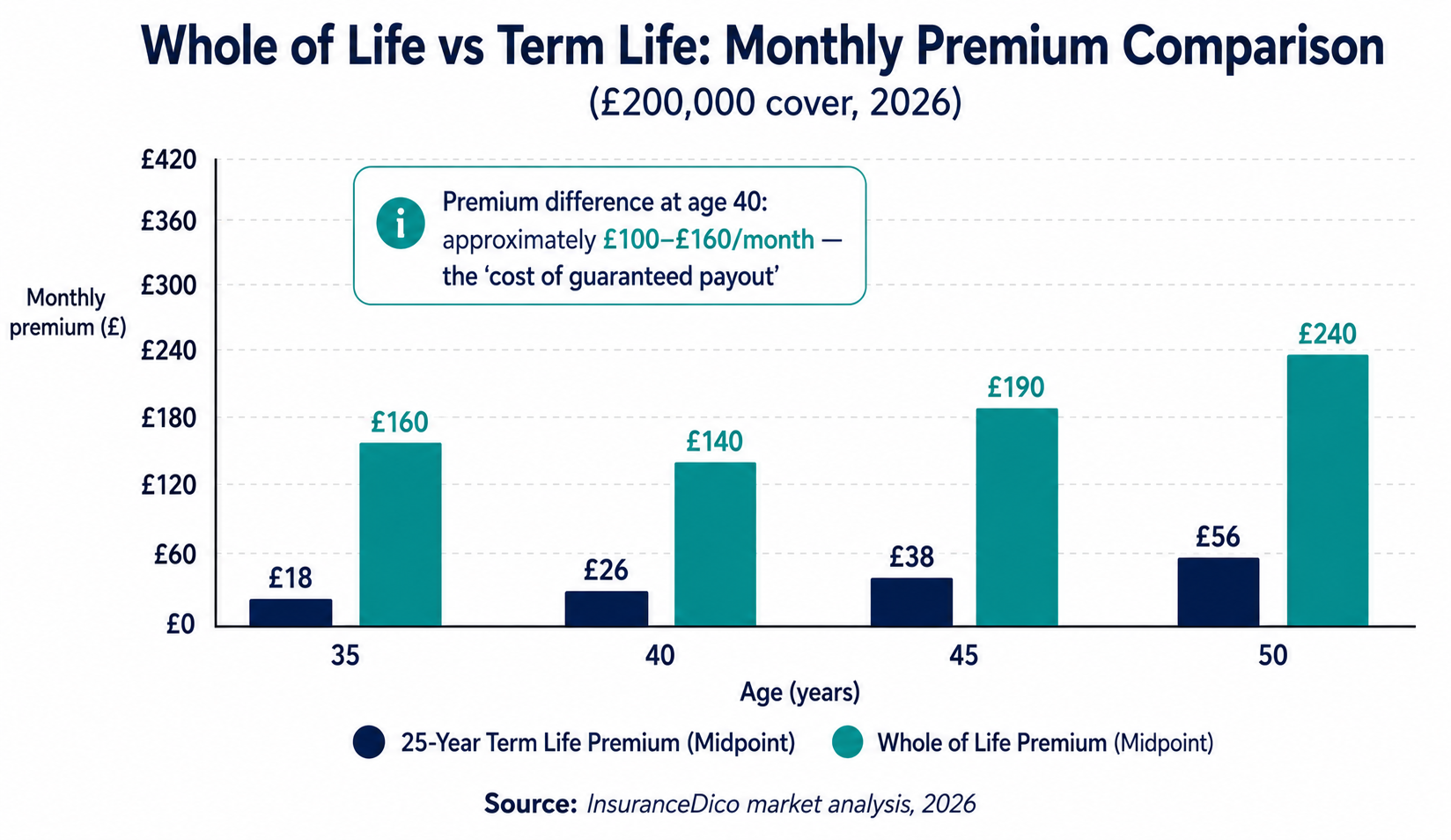

Whole of Life vs Term Life — the Financial Comparison

The premium gap between whole of life and term life is substantial and should be evaluated as a deliberate financial trade-off, not a quality difference.

| Age | £200,000 Term Life (25 years) | £200,000 Whole of Life (guaranteed) |

|---|---|---|

| 35 | £13–£22/month | £85–£140/month |

| 40 | £21–£35/month | £118–£195/month |

| 45 | £33–£57/month | £165–£280/month |

| 50 | £54–£94/month | £235–£400/month |

The "buy term and invest the difference" argument: the standard financial planning argument against whole of life insurance is that a higher-premium whole of life policy could be replaced by a lower-premium term life policy plus an investment of the premium difference. If the investment delivers adequate returns, the investment pot plus the term policy provides equivalent or better financial outcomes.

This argument is valid in isolation. Its limitations:

- It assumes discipline in investing the premium difference — many people do not

- It does not address the guaranteed payout characteristic needed for IHT planning

- It is more complex to manage across a lifetime than a simple insurance contract

- It does not provide the trust structure that keeps the payout outside the estate

For IHT planning specifically, the investment alternative does not replicate the trust mechanism that protects proceeds from IHT assessment.

The Trust Question — Why It Almost Always Applies to Whole of Life

Most whole of life insurance is taken out for IHT planning or legacy purposes — and in both cases, writing the policy in trust is the correct structure.

Without a trust: the policy payout forms part of your estate on death. It is assessed for IHT and must go through probate before beneficiaries receive it. This defeats much of the purpose of using whole of life for IHT planning.

With a trust: the policy sits outside your estate. On death, the trustees receive the payout directly without probate. Beneficiaries receive funds quickly and without IHT.

Types of Trust Used for Whole of Life Policies

Discretionary Trust: trustees have discretion over who among a class of beneficiaries receives the funds and in what proportion. Flexible and suitable where family circumstances may change. The most commonly recommended trust type for whole of life policies used in IHT planning.

Absolute (Bare) Trust: beneficiaries are named at outset and cannot be changed. Simpler but inflexible.

Most insurers provide a free trust document at the time of policy application. Completing the trust at inception costs nothing — completing it later requires legal assistance and may be more complex. Never postpone the trust.

What Whole of Life Insurance Does Not Cover

Death before premiums start being paid: in the extremely rare scenario where a policyholder dies within days of application but before the first premium is paid, coverage may not yet be in force. Confirm the specific inception date with your insurer.

Death from excluded causes in the early policy period: some whole of life policies include suicide exclusions for an initial period (typically 12 months) — consistent with standard practice across life insurance products.

Reviewable policies where the fund is insufficient: in reviewable (unit-linked) policies, if the investment fund underperforms significantly, the insurer may require substantially higher premiums to maintain the guaranteed sum. In extreme cases, policies have been cancelled by the insurer when policyholders could not afford the increased premiums. Guaranteed sum assured policies (where the premium is fixed) do not carry this risk.