Term life insurance pays a tax-free lump sum to your chosen beneficiaries if you die within a fixed period — typically 10 to 40 years. Premiums are locked at the rate agreed when the policy starts and do not increase with age. A healthy non-smoking 30-year-old can cover £200,000 for 25 years for approximately £9–£14 per month. The ABI reported that 98.2% of UK life insurance claims were paid in 2023. The most critical decisions are how much coverage you need — not a rule of thumb but a calculation — and whether level term or decreasing term is appropriate for your specific situation.

Term life insurance is a fixed-period UK life policy that pays a tax-free lump sum to nominated beneficiaries if the insured dies within the policy term — with premiums locked at outset, no cash value, and no payout if the insured survives the term.

What Term Life Insurance Is — and What It Is Not

Term life insurance is the simplest and most cost-efficient form of life insurance available in the UK. The policy structure has three elements:

The term: A fixed period during which the policy is in force — 10, 15, 20, 25, or 30 years are the most common options. If you die within the term, the policy pays. If you survive the term, the policy ends with no payout and no cash value.

The sum insured: The lump sum your beneficiaries receive on a valid claim. This amount is agreed at the policy start and is paid in full if the claim is valid. It is free of income tax and capital gains tax.

The premium: A fixed monthly or annual payment that does not change for the duration of the policy. A premium agreed at age 30 remains at that level at age 50, regardless of changes in your health.

What term life insurance is not: It is not an investment. It builds no cash value, earns no return, and cannot be cashed in before it expires. If you want a life insurance product that builds cash value, that is whole of life insurance — a different and more expensive product. The absence of a savings component is what makes term life affordable. It is pure protection.

Level Term vs Decreasing Term — the Decision That Determines Your Premium

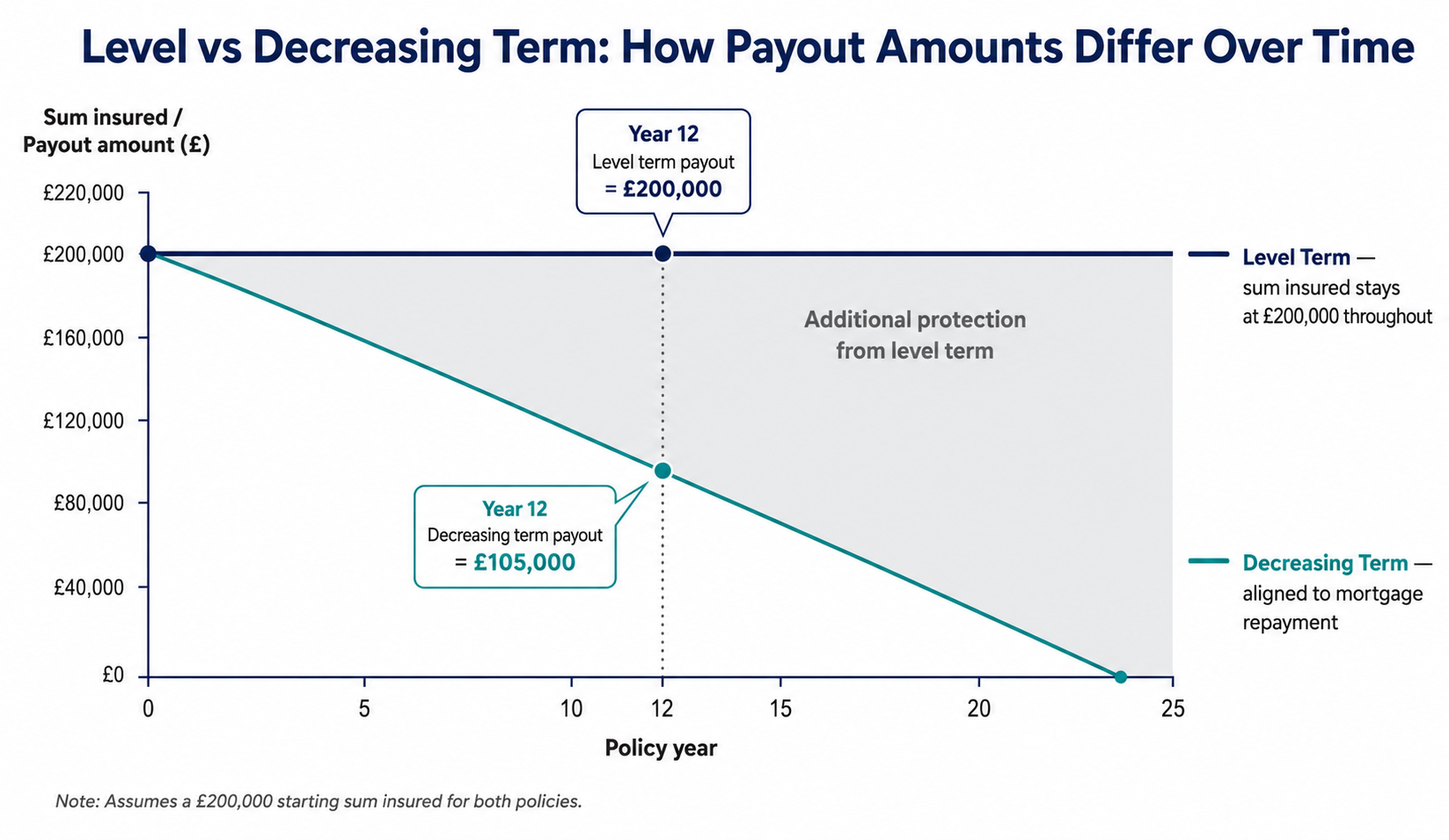

The single most consequential decision within term life insurance is whether to buy a level or a decreasing policy.

Level Term Life Insurance

The sum insured stays constant throughout the policy. If you die in year one, your beneficiaries receive the full sum insured. If you die in year 24 of a 25-year policy, they receive the same amount.

When level term is the right choice:

- When the primary purpose is income replacement for dependants — your family needs the same amount of money regardless of when you die

- When you have interest-only mortgage debt that does not reduce over time

- When you want to leave a specific financial amount to beneficiaries regardless of timing

- When you have non-mortgage debt that does not reduce (personal loans, business debts you have personally guaranteed)

Decreasing Term Life Insurance

The sum insured reduces throughout the policy — typically aligned to an outstanding repayment mortgage balance. The payout at year 10 of a 25-year policy is lower than at year one, reflecting the fact that the mortgage has been partially repaid.

When decreasing term is the right choice:

- When the primary purpose is mortgage protection on a capital repayment mortgage

- When you want the lowest possible premium for a specific protection need

- When you have other financial assets that grow over time and reduce the need for a large fixed payout in later years

The cost difference: Decreasing term is typically 20–35% cheaper than level term for the same starting sum insured and policy term. For a 30-year-old taking out £200,000 of 25-year cover: level term costs approximately £9–£14 per month; decreasing term costs approximately £6–£10 per month.

The hybrid strategy: Many financial planners recommend combining both types: a decreasing term policy aligned to the mortgage (protecting the property for the family) plus a smaller level term policy for income replacement (protecting the family's living costs). The total premium is often lower than a single large level term policy while providing more appropriate coverage for each specific need.

How Much Term Life Insurance Do You Actually Need?

The "10 times your salary" shorthand is a starting point that frequently produces the wrong answer. Two people on identical salaries can need dramatically different coverage depending on their mortgage, their dependants, and their household income structure.

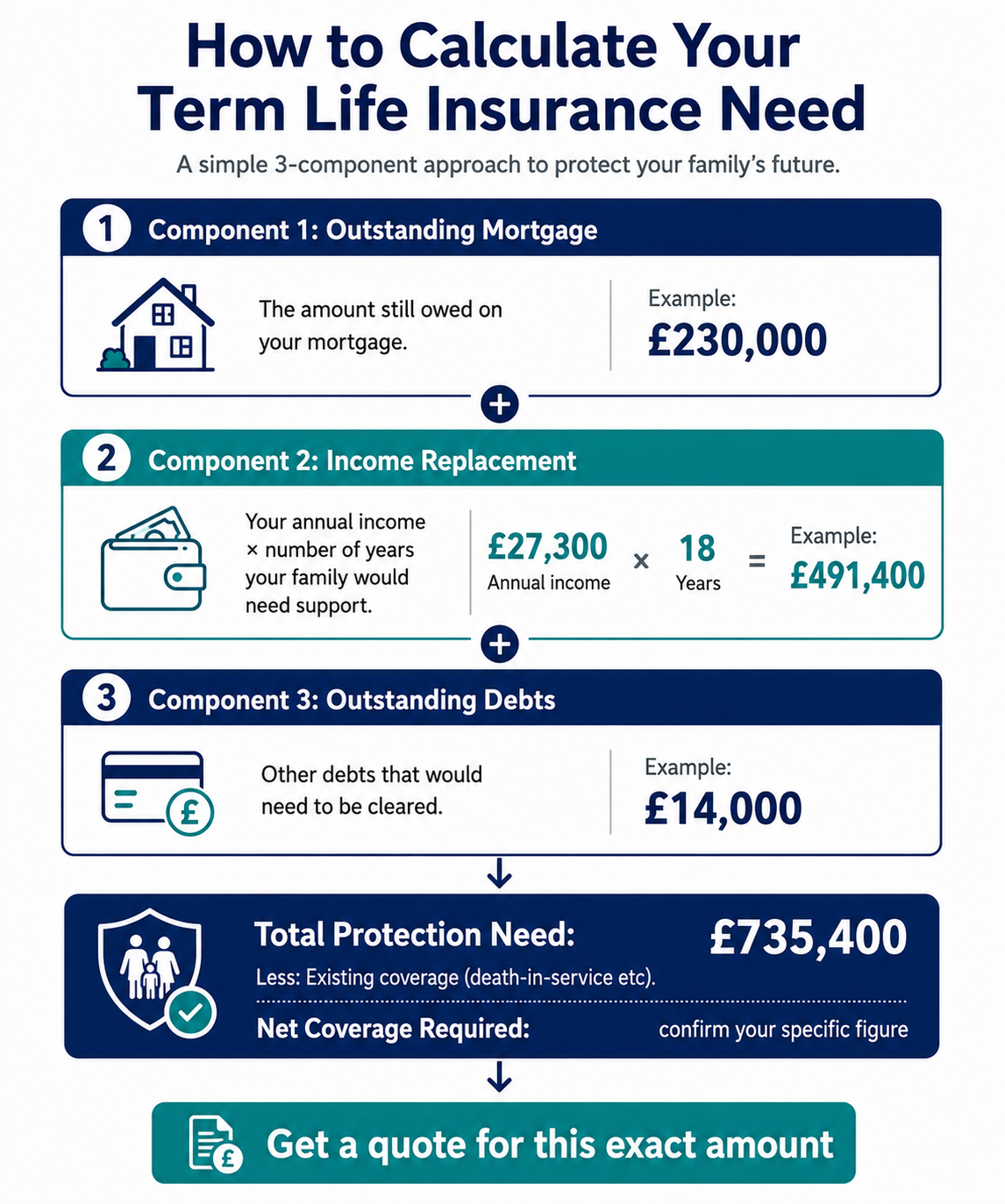

The Three-Component Calculation

Component 1 — Outstanding mortgage balance: What is your outstanding mortgage? This is the most straightforward component. Your family needs enough money to pay off the mortgage entirely, or enough coverage to continue servicing it if the surviving partner earns sufficient income to do so alone. For most single-income households with a large mortgage, the full balance is the target.

Component 2 — Income replacement for dependants: How many years until your youngest child is financially independent (age 21–25 is the standard assumption)? What annual income would your family need to maintain their standard of living? Typically 60–70% of your current gross income is used as the replacement rate — covering essential costs without replicating every discretionary expense.

Calculation: £38,000 annual income × 65% replacement rate × 20 years until youngest child is independent = £494,000 in today's values.

Component 3 — Outstanding unsecured debts: Personal loans, car finance, business debts with personal guarantees. These do not disappear on death — they become claims against the estate.

Add components 1, 2, and 3. Then subtract existing coverage:

- Death-in-service benefit from your employer (typically 4× annual salary — check your employee handbook or HR team)

- Any existing personal life insurance policies

- Readily accessible savings and investments that the family could draw on

The result is your net coverage requirement.

Three Worked Examples

Example 1 — Sole earner with young children: Income: £42,000. Mortgage: £230,000 outstanding. Two children aged 4 and 7. Non-earning partner. No death-in-service. No savings.

- Mortgage: £230,000

- Income replacement: £27,300/yr × 18 years = £491,400

- Car finance: £14,000

- Total required: £735,400. Less existing coverage: £0. Net need: £735,000

Example 2 — Dual income, shared mortgage: Each earns £34,000. Joint mortgage: £195,000. No children. Each has 4× death-in-service (£136,000 each).

- Mortgage: £195,000 (surviving partner could potentially service alone)

- Income replacement: minimal (partner earns independently)

- Total required per partner: £195,000 (mortgage protection). Less DIS: £136,000. Net per partner: approximately £60,000–£80,000

Example 3 — Business owner, complex situation: Income: £85,000. Mortgage: £380,000. Two children. Personal guarantee on business loan: £65,000. No death-in-service.

- Mortgage: £380,000

- Income replacement: £55,250/yr × 20 years = £1,105,000

- Business debt: £65,000

- Total required: £1,550,000. After liquid savings (£80,000): Net need: £1,470,000

2026 Term Life Insurance Premiums — What You Will Pay

Premiums are calculated by actuaries and are driven primarily by four factors: age, health, smoking status, and the combination of sum insured and policy term.

| Age | £150,000, 20 years | £250,000, 25 years | £500,000, 25 years |

|---|---|---|---|

| 25 | £5–£8 | £8–£13 | £14–£22 |

| 30 | £6–£10 | £9–£15 | £16–£26 |

| 35 | £8–£13 | £13–£21 | £24–£40 |

| 40 | £13–£21 | £21–£35 | £38–£65 |

| 45 | £20–£34 | £33–£57 | £62–£108 |

| 50 | £32–£55 | £54–£94 | £103–£180 |

The Smoking Premium — What "Smoker" Means in 2026

Insurers classify you as a smoker if you have used any tobacco or nicotine product in the past 12 months — cigarettes, cigars, pipe tobacco, e-cigarettes, vapes, nicotine patches, or nicotine gum. Vaping is treated as smoking by most UK life insurers as of 2026, regardless of nicotine content.

The smoking loading is typically 100–130% above non-smoker rates — a 35-year-old paying £13/month as a non-smoker pays approximately £26–£30 as a smoker for the same coverage. If you quit smoking and remain smoke-free for 12 consecutive months, most insurers will reclassify you to non-smoker rates on request — providing you declare the change and reapply on revised terms.

How Pre-Existing Conditions Affect Term Life Premiums

Most conditions are insurable at a premium loading. Common conditions and typical outcomes:

| Condition | Typical Outcome | Loading Range |

|---|---|---|

| Treated high blood pressure, controlled | Accepted with loading | +20–60% |

| Type 2 diabetes (HbA1c < 58 mmol/mol) | Accepted with loading | +50–150% |

| BMI 30–35 | Minor loading or standard | +0–30% |

| BMI 35–40 | Loading applied | +30–80% |

| Depression (treated, stable) | Usually accepted | +0–50% |

| Previous cancer (5+ years, complete remission) | Often standard | +0–40% |

| Active cancer treatment | Declined until treatment complete | N/A |

The Policy Decisions Beyond Coverage Amount

Policy term length: The term should cover the period of your greatest financial vulnerability — typically until your youngest child is financially independent and your mortgage is repaid. Setting a term that ends 10 years before your mortgage does leaves the final decade of mortgage exposure uninsured. Extend the term to match your longest financial obligation.

Beneficiary nomination: Nominating your beneficiaries determines who receives the payout. For most people, the answer is their partner or their children. However, for married couples, a payout to the surviving spouse forms part of the estate and may attract inheritance tax. Writing the policy in trust places the payout outside the estate — it passes to beneficiaries without going through probate and is not subject to inheritance tax. Trust writing is a simple administrative step offered by most life insurers at no cost at the time of application.

Waiver of premium: An optional add-on that waives monthly premiums if you become unable to work due to illness or injury. Typically deferred for the first 26 weeks of incapacity and costs approximately 10–15% of the base premium. Most appropriate for sole earners or households without substantial savings that could service insurance premiums during an extended absence from work.

Indexation: Some policies allow the sum insured to increase annually in line with RPI or a fixed percentage, with premiums increasing proportionally. This addresses the inflation risk — £200,000 in 25 years has significantly lower purchasing power than £200,000 today. Indexation closes this gap at the cost of higher premiums over time.