Black box insurance — also called telematics insurance — installs a device in your car or uses a smartphone app to monitor your driving behaviour. The data collected (speed, braking, cornering, time of day, and mileage) is used to price your renewal and may adjust premiums mid-policy for safe or unsafe driving. For young drivers aged 17–25, black box policies typically save 20–30% on standard market rates and provide the fastest route to building a meaningful claims history. The main restrictions to understand before purchasing are night-time driving rules, mileage caps on some products, and what happens when the system records a bad event.

Black box car insurance is a UK motor insurance product that uses real driving behaviour data — captured by a vehicle-installed device or smartphone app — rather than demographic proxies to price the premium and adjust it at renewal.

What Black Box Insurance Is and How the Technology Works

Black box insurance is a motor insurance product where the insurer uses real driving behaviour data — rather than demographic and statistical proxies — to price the risk. The name refers to the telematics device originally installed in vehicles, though smartphone-based telematics (using the phone's GPS, accelerometer, and gyroscope) are now equally common.

The Three Delivery Methods

- Hardwired telematics device: A small device permanently installed in your vehicle, typically connected to the OBD-II (On-Board Diagnostics) port or hardwired by an approved installer. Records speed, GPS location, acceleration, braking force, and cornering forces in real time. Continuous monitoring with no reliance on the driver to activate anything.

- Self-fitted plug-in device: A device the policyholder inserts into the OBD-II port themselves (no installer required). Less robust than hardwired devices but quicker and cheaper to deploy. Subject to tampering risk — some policies require the device to remain connected as a policy condition.

- Smartphone telematics (app-based): Uses the policyholder's existing smartphone to capture driving data via the phone's sensors. The app must be running and the phone in the car during every drive. Advantages: no device cost, no installation, easy for multiple vehicles or when changing cars. Disadvantages: relies on driver compliance, phone battery life, and consistent connectivity.

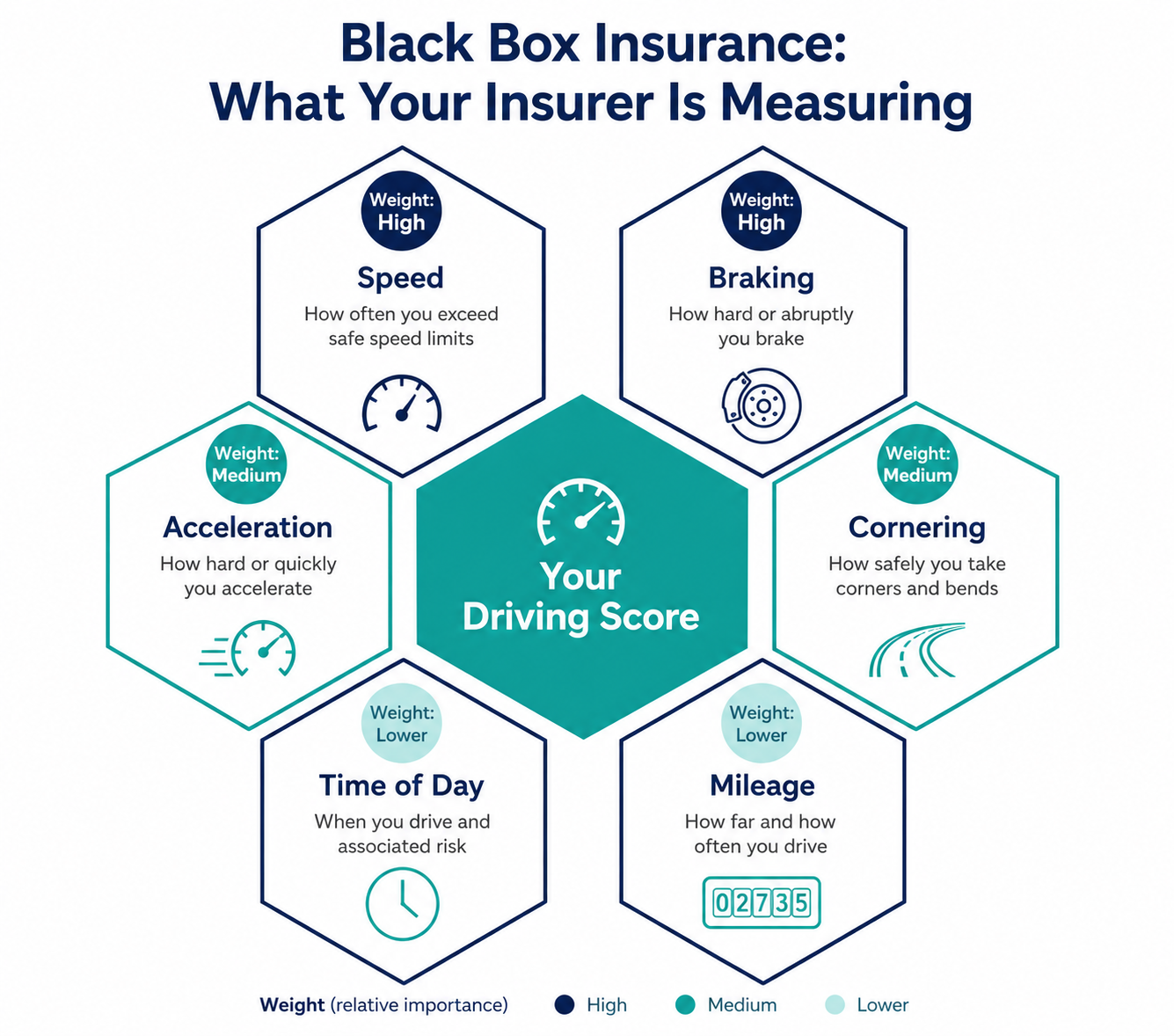

What the System Measures — the Six Data Points

- Speed: Absolute speed compared to GPS-determined speed limits on the road being driven. Consistently driving at or above the speed limit on 30mph roads produces worse scores than on motorways — urban speeds are weighted more heavily in accident risk models.

- Acceleration: How sharply the vehicle accelerates from stationary or low speed. Harsh acceleration (wheel spin, rapid throttle input) suggests aggressive or inexperienced driving.

- Braking: Force applied when slowing the vehicle. Emergency braking events — brake pedal applications producing deceleration above a defined g-force threshold — are recorded as individual incidents and reviewed. Smooth, progressive braking scores well.

- Cornering: Lateral g-forces during turns. Taking corners at excessive speed, changing lanes aggressively, or rounding roundabouts too quickly produces harsh cornering scores.

- Time of day: Driving between midnight and 5am is weighted as significantly higher risk than equivalent driving during daytime hours. This is actuarially sound — accident rates per mile are 3–4 times higher during night-time hours. Some policies apply explicit night-time surcharges or curfews; others include time of day in the overall driving score calculation.

- Mileage: Higher annual mileage increases accident exposure. Some black box policies cap annual mileage — exceeding the cap may trigger a premium increase or policy review.

How Black Box Insurance Affects Your Premium

Initial Pricing

At policy inception, the black box insurer prices the policy using a combination of standard rating factors (age, vehicle, postcode, driving experience) and the fact that you have opted into telematics monitoring — which statistically correlates with lower risk behaviour, providing an initial discount versus the standard market. For a 19-year-old driver, this initial discount is typically 20–30% below the equivalent standard comprehensive premium.

Mid-Term Adjustments

- Score-based adjustment: After an initial assessment period (typically 1–3 months), the insurer reviews your driving score. If you are consistently scoring above a defined threshold, a mid-term discount is applied. Poor scores may result in a premium increase or a warning letter.

- Fixed-term reviews: Some products review driving data at defined intervals (monthly or quarterly) and adjust the premium or provide cashback based on performance.

- Warning and policy action triggers: Specific behaviours — speeding above a defined threshold, driving during a curfew period, or a serious road incident — may trigger a formal warning. Repeated violations can result in policy cancellation in the most serious cases.

Renewal Pricing

The most significant financial impact of black box data is at renewal. A full year of driving data replaces the statistical demographic proxy (young driver statistics) with your actual driving record. A 20-year-old who has driven safely for 12 months — no incidents, good scores — typically receives a renewal quote significantly below the first-year premium, accelerating their journey to standard market rates.

Night-Time Restrictions — the Policy Feature That Affects Life Most

The night-time driving restriction is the most practically significant feature of black box policies for young drivers. Different products handle this differently:

- Curfew policies: Some black box products impose a hard curfew — typically midnight to 5am — during which the vehicle cannot be driven without incurring a per-journey surcharge (typically £3–£5 per curfew breach) or triggering a policy review. Persistent night driving generates escalating charges that can eliminate the initial premium saving.

- Score-weighted policies: Other products do not impose a curfew but heavily weight night driving in the overall score. Regularly driving between midnight and 5am reduces the overall score and produces higher renewal premiums.

- No restriction policies: A smaller number of black box products monitor all driving without applying specific time restrictions — they use the aggregate data for scoring rather than isolating night hours.

Which Black Box Insurance Providers Are Best in 2026

Each provider uses a different scoring methodology, device type, and pricing structure. The key variables when comparing:

| Entity | Attribute | Value | Source |

|---|---|---|---|

| Marmalade | Profile | Established specialist in under-25 telematics. App feedback. No curfew on newer products. Available for learners, new drivers, and named-driver add-ons. | Marmalade product literature, 2026 |

| ingenie | Profile | Pure telematics specialist. Strong score transparency and weekly feedback via app. Night-time weighted in score but no hard curfew. Good for regular night drivers. | ingenie product literature, 2026 |

| Hastings Direct SmartMiles | Profile | Mileage-based pricing with telematics monitoring. Pay per mile rather than fixed premium. Best for drivers covering fewer than 6,000 miles per year. | Hastings Direct SmartMiles, 2026 |

| Admiral LittleBox | Profile | App and box options. Regular score updates. Night-time curfew on some products — check the specific product terms at the time of purchase. | Admiral product literature, 2026 |

| Vitality Drive | Profile | Rewards-based telematics tied to the Vitality ecosystem. Safe driving earns rewards and discounts across the Vitality partner network. | Vitality Drive, 2026 |

Building Your NCB on a Black Box Policy

No-claims bonus accrues on black box policies in the same way as standard policies — one year of claim-free driving builds one year of NCB. There is no disadvantage to black box insurance in terms of NCB accumulation.

The practical advantage: NCB accumulated during a black box policy period is portable. When you transition to a standard market policy — typically after 2–3 years of telematics driving — your NCB follows you. A 21-year-old with three years of black box driving and 3 years NCB accesses standard market premiums meaningfully lower than a 21-year-old entering the standard market with no driving history. The transition path is the key benefit of black box insurance beyond the immediate premium saving.

2026 Premium Data — Black Box vs Standard Market

The following comparison uses the same driver profile and vehicle to illustrate the typical saving from telematics insurance. Profile: 19-year-old driver, 1-year provisional licence, 2020 Vauxhall Corsa, urban postcode, 5,000 miles per year.

| Policy Type | Annual Premium | Monthly |

|---|---|---|

| Standard comprehensive (no telematics) | £2,180–£2,840 | £182–£237 |

| Black box — standard scoring | £1,520–£2,040 | £127–£170 |

| Black box — excellent score maintained | £1,320–£1,780 | £110–£148 |

| Potential renewal premium (year 2, clean record) | £1,100–£1,600 | £92–£133 |

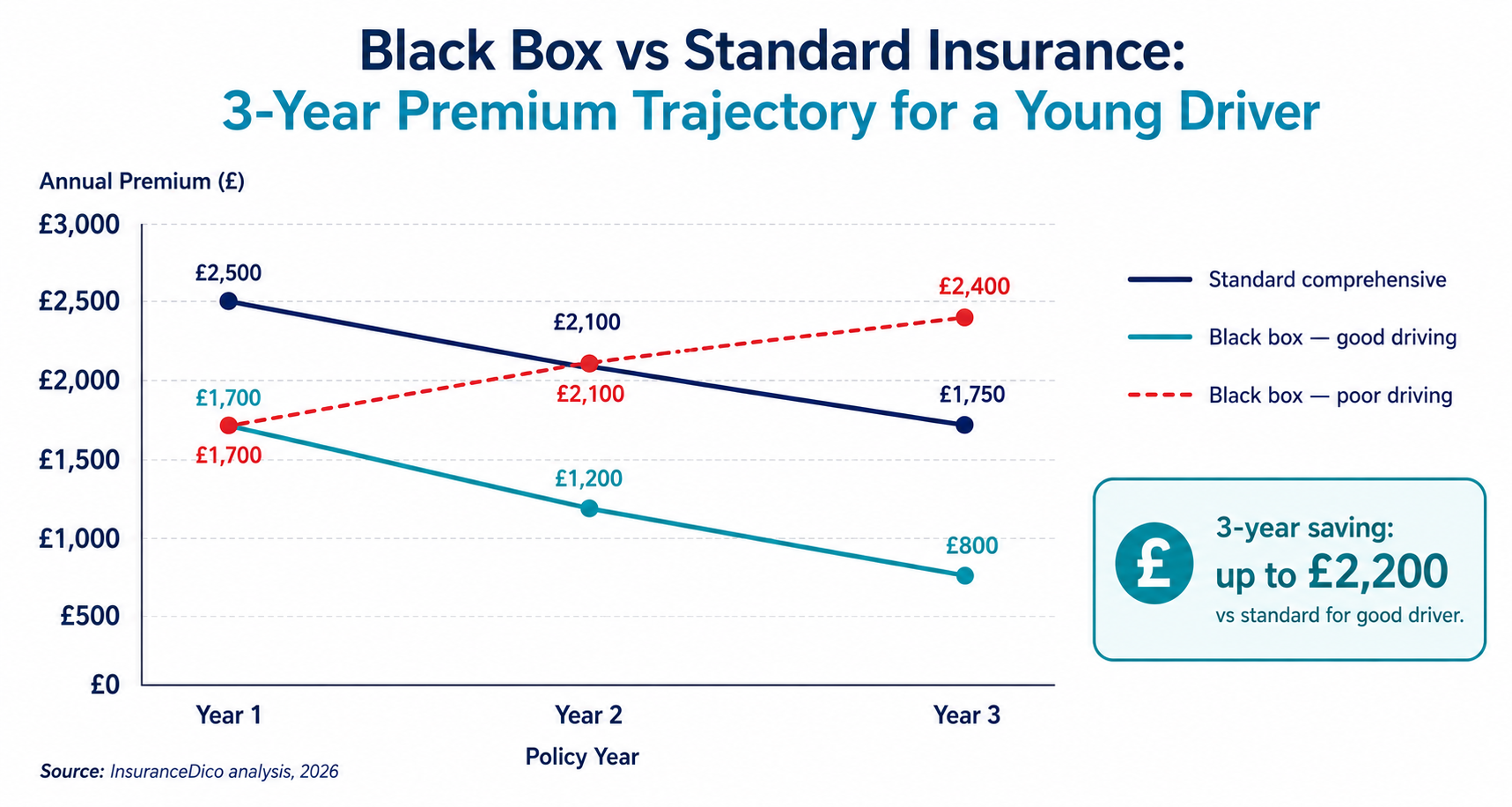

The trajectory over three years: A young driver who starts on a standard policy at £2,500 and drives without telematics for three years might pay £2,500 → £2,100 → £1,750. A young driver on black box who drives well pays £1,700 → £1,200 → £800. The three-year saving can exceed £2,000 in favourable scenarios.

Data Privacy — What Your Black Box Records and Who Sees It

Black box data is personal data under UK GDPR. Insurers are required to handle it in compliance with data protection law.

- What is collected: Your driving data (speed, location, acceleration, braking) is collected in real time during every drive. GPS data records your routes — your insurer knows where you drive, not only how you drive.

- Who has access: Your insurer. In the event of a serious road incident or legal investigation, data may be requested by police or courts under a legal process. Data may also be shared with third-party claims handlers during a claims investigation.

- Retention period: Most insurers retain black box data for the duration of the policy and a defined period afterward (typically 3–7 years, consistent with claims limitation periods).

- The portability right: You have the right to request a copy of your personal data held by your insurer under UK GDPR Article 15. If you believe your driving score has been calculated incorrectly, the underlying data should be available on request.

“Night-time driving — typically defined as midnight to 5am — is the highest-risk driving period per mile and is either subject to surcharges under curfew-based black box policies or heavily weighted in score-based systems. The practical implication of night-time driving restrictions should be assessed before selecting a telematics product.”

Frequently Asked Questions

Key takeaways

- Black box car insurance prices premiums on real driving behaviour rather than demographic proxies.

- Black box car insurance saves UK drivers aged 17–25 typically 20–30% on first-year premiums.

- Black box car insurance penalises night-time driving and harsh events — check policy terms first.