Classic car insurance is specialist motor coverage for vehicles of historical, collectible, or enthusiast value. The most important distinction from standard car insurance is the agreed value settlement — in a total loss, your insurer pays the value you agreed at inception, not the depreciated market value at the time of the claim. Most classic car policies use limited mileage (typically 3,000–7,500 miles per year) in exchange for significantly lower premiums. Classic car insurance is not available through standard comparison sites and requires specialist insurers including Hagerty, Adrian Flux, Footman James, and Lancaster Insurance.

Why Classic Cars Need Different Insurance — the Three Core Differences

Standard car insurance is designed for modern vehicles used as daily transport. The underwriting assumptions — high annual mileage, vehicle depreciation, repair through franchised dealer networks, market value settlement — do not apply to classic and collectible vehicles.

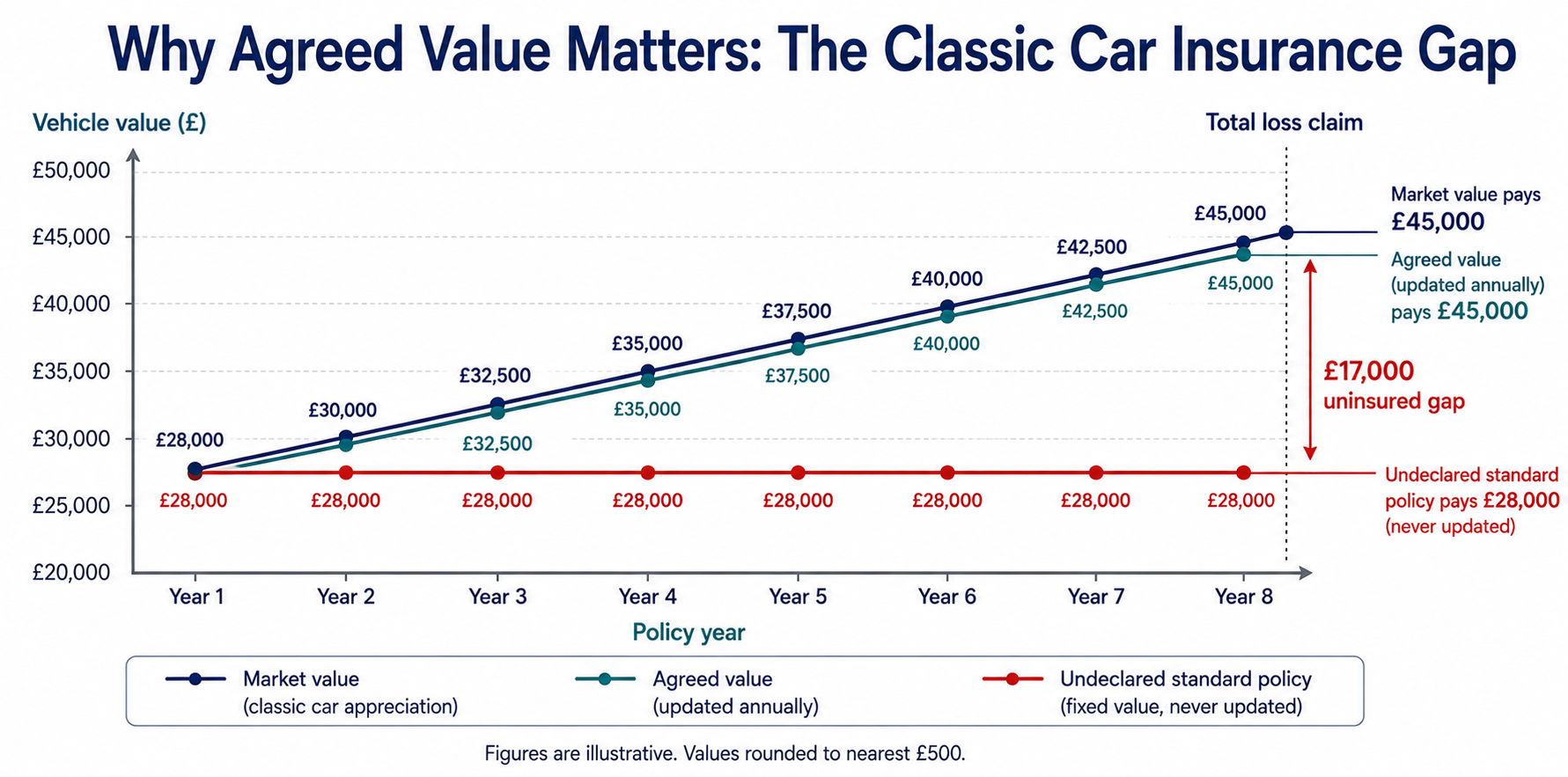

Difference 1 — Agreed value, not market value

Standard comprehensive car insurance settles total loss claims at market value at the time of the loss — what the vehicle would have sold for on the open market the day before it was destroyed. For modern vehicles that depreciate steadily, this is a fair and predictable settlement basis.

Classic cars frequently appreciate in value over time. A 1971 Porsche 911T worth £45,000 in 2020 may be worth £65,000 in 2026. A standard comprehensive policy taken out in 2020 at £45,000 declared value and not updated would pay only £45,000 in a 2026 total loss — leaving a £20,000 gap against the actual market replacement cost.

Classic car insurance uses agreed value — the insurer and policyholder agree a specific value at inception, documented in the policy schedule. In a total loss, the agreed value is paid in full, without negotiation or dispute. The agreed value should be reviewed and updated at every annual renewal to reflect appreciation in the classic car market.

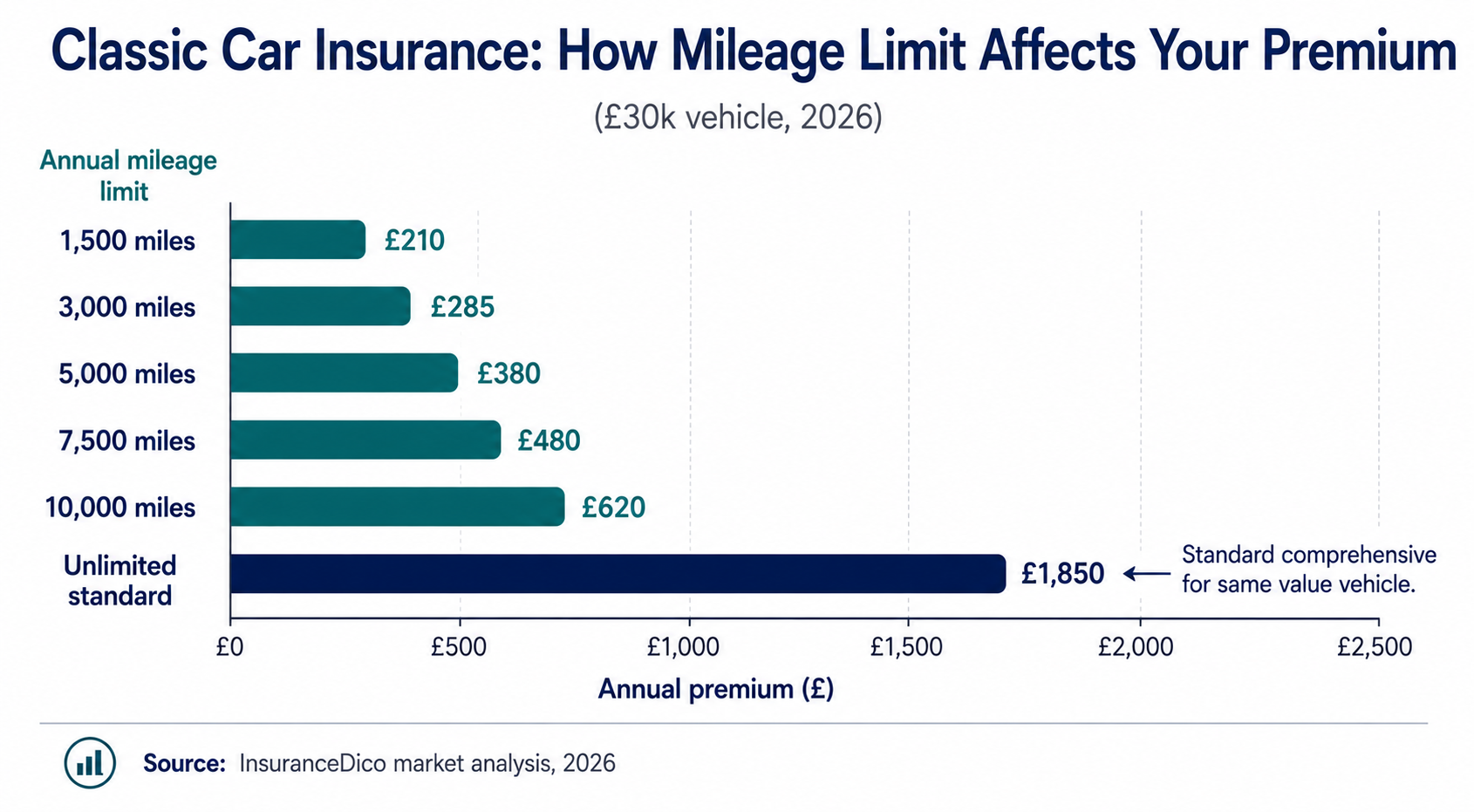

Difference 2 — Limited mileage, lower premium

Classic vehicles are typically driven significantly fewer miles per year than modern daily drivers. A classic used for summer weekend driving, rallies, and shows may cover 3,000–5,000 miles annually. Standard motor insurance rates assume much higher usage.

Classic car policies are written with a maximum annual mileage — typically 3,000, 5,000, or 7,500 miles. In exchange, premiums are substantially lower than equivalent standard comprehensive policies. A classic car worth £30,000 can often be insured for £300–£600 per year on a limited mileage basis — a fraction of what standard comprehensive would cost on a vehicle of this value.

Difference 3 — Specialist repair network

Modern vehicles are repaired through franchised dealer networks with access to standardised parts. Classic vehicle repair requires specialist knowledge, period-correct or new old stock parts, and craftspeople with skills in coachwork, mechanical restoration, and authentic materials.

Classic car insurance policies recognise this by allowing repairs at specialist classic car workshops rather than requiring use of approved modern repair centres. The labour rates and parts costs for classic vehicles differ significantly from modern repair, and insurers in this market have the underwriting experience to assess these costs appropriately.

What Qualifies as a Classic Car for Insurance Purposes

There is no single universally applied definition. The relevant reference points:

DVLA Vehicle Excise Duty (free road tax): Vehicles manufactured 40 or more years before the current tax year are exempt from vehicle excise duty — the rolling "historic vehicle" classification. This is an administrative definition only, not an insurance definition.

Insurer definitions: Each specialist classic car insurer applies its own criteria. Broadly, a vehicle qualifies as a classic for insurance purposes when:

- It is at least 15–30 years old (varies by insurer — some apply a 15-year threshold, others 20 or 25 years)

- It is maintained in a condition consistent with its age and historical significance (not a daily driver in deteriorating condition)

- Its use is limited — not a primary transport vehicle used for commuting or daily shopping

- The owner has a clean or near-clean driving record and a modern daily driver (most specialist classic car insurers require the policyholder to have a separate standard vehicle for everyday use)

| Category | Description | Typical Insurance Approach |

|---|---|---|

| Pre-war vehicles (pre-1940) | Veteran and vintage | Specialist Lloyd's syndicates, very limited mileage |

| Classic (1945–1985) | The core classic car market | Specialist insurers, agreed value standard |

| Modern classic (1985–2005) | Growing collector interest | Some specialist, some standard insurers |

| Performance/supercar (any era) | High value regardless of age | Specialist placement, often Lloyd's |

2026 Classic Car Insurance Premiums — What to Expect

Classic car insurance premiums are significantly lower than standard comprehensive premiums for vehicles of equivalent value, reflecting the lower annual mileage, more careful use, and statistically lower accident frequency among classic car owners.

| Vehicle Type | Agreed Value | Annual Mileage Limit | Indicative Annual Premium |

|---|---|---|---|

| Post-war British classic (1950s–60s) | £15,000–£25,000 | 3,000–5,000 | £220–£380 |

| British sports car (1960s–70s) | £20,000–£45,000 | 3,000–5,000 | £280–£520 |

| Classic German/Italian (1960s–70s) | £35,000–£80,000 | 3,000–5,000 | £380–£780 |

| Modern classic (1985–2000) | £8,000–£20,000 | 5,000–7,500 | £180–£340 |

| High-value post-war (Ferrari, Porsche pre-1975) | £80,000–£300,000+ | 2,000–3,000 | £900–£3,500+ |

| American muscle (1960s–70s) | £25,000–£60,000 | 3,000–5,000 | £320–£680 |

Factors that increase classic car premiums

- Modification from original specification (supercharger conversions, engine swaps, bodywork changes) — each modification must be declared

- Track day use (standard classic policies exclude circuit driving — a track day extension is available at additional cost)

- Commercial use (film and television appearances, commercial photography)

- Storage risk (storing in a shared lock-up rather than a dedicated private garage)

- Claims history on any vehicle in the past five years

The Mileage Limit — What Happens If You Exceed It

Classic car policies specify a maximum annual mileage as a condition of coverage. The standard options are 3,000, 5,000, 7,500, or occasionally 10,000 miles per year.

If you exceed your agreed mileage: Exceeding the mileage limit is a material change to the risk that your insurer expects to be notified of. Technically, driving over your stated mileage limit without notifying the insurer may allow the insurer to reduce a claim settlement on a proportional basis.

The practical insurer approach: Most specialist classic car insurers deal pragmatically with modest mileage overruns. A policyholder who drives 5,800 miles against a 5,000 limit is unlikely to face a proportional claim reduction — but should notify the insurer and arrange a mid-term adjustment to the mileage allowance. An insurer discovering a substantial overrun (8,000 miles driven against a 3,000 limit) at the point of a claim has stronger grounds to dispute the settlement.

The correct approach: Choose a mileage limit that realistically reflects your intended usage — with modest headroom. Adjusting the limit upward mid-policy typically costs a modest additional premium and eliminates the material change risk.

Agreed Value — How to Establish the Right Figure

The agreed value is the central financial element of classic car insurance. Getting it right protects you in a total loss claim. Getting it wrong in either direction has consequences:

Too low: In a total loss, you receive less than the vehicle's market value — a gap you fund personally.

Too high (material overstatement): Insurers reserve the right to reduce a total loss settlement to the true market value if the agreed value was materially overstated. Intentional overstatement constitutes fraud.

How to establish the correct agreed value

- Specialist auction house results: Recent sales of comparable vehicles at established classic car auctions (RM Sotheby's, Bonhams, Silverstone Auctions, H&H Classics) provide the most reliable market data for significant vehicles.

- Published price guides: Classic Cars magazine, Practical Classics, and the Hagerty Price Guide (free online) publish current market values by model, year, and condition grade. These are used as reference by specialist insurers.

- Independent specialist valuation: A written valuation from a marque specialist or established classic car dealer provides a documented basis for the agreed value that both insurer and policyholder can reference.

| Grade | Description | Value Impact |

|---|---|---|

| Concours | Show-winning, perfectly restored or maintained | Premium above guide price |

| Excellent | Fully sorted, presentable at any event | Guide price |

| Good | Running well, minor cosmetic imperfections | 80–90% of guide price |

| Driver | Reliable driver, presentable but not immaculate | 60–75% of guide price |

| Project | Requires restoration, may not be running | 25–50% of guide price |

The Main Classic Car Insurance Specialists

Hagerty: The UK's largest specialist classic car insurer by policy count. Originally a US company, now a major UK market presence. Strong agreed value methodology, market data from their own Price Guide, and a membership community. Available through their own website and specialist brokers.

Adrian Flux: Specialist motor insurer with a dedicated classic car division. Broad appetite including modified classics, hot rods, American vehicles, and kit cars. Competitive for unusual or modified vehicles.

Footman James: Dedicated classic and specialist vehicle insurer with long market history. Strong for UK classics and prestige vehicles. Available through specialist brokers.

Lancaster Insurance: Specialist classic and prestige vehicle insurer. Competitive premiums, strong reputation for claims handling on significant vehicle losses.

Sureterm Direct: Online-focused specialist insurer covering classics, performance vehicles, and kit cars. Competitive pricing for modern classics and vehicles in the 15–25 year age bracket.

“Classic car insurance uses an agreed value settlement basis — the insurer and policyholder agree a specific value at inception, and in a total loss that value is paid in full without dispute.”