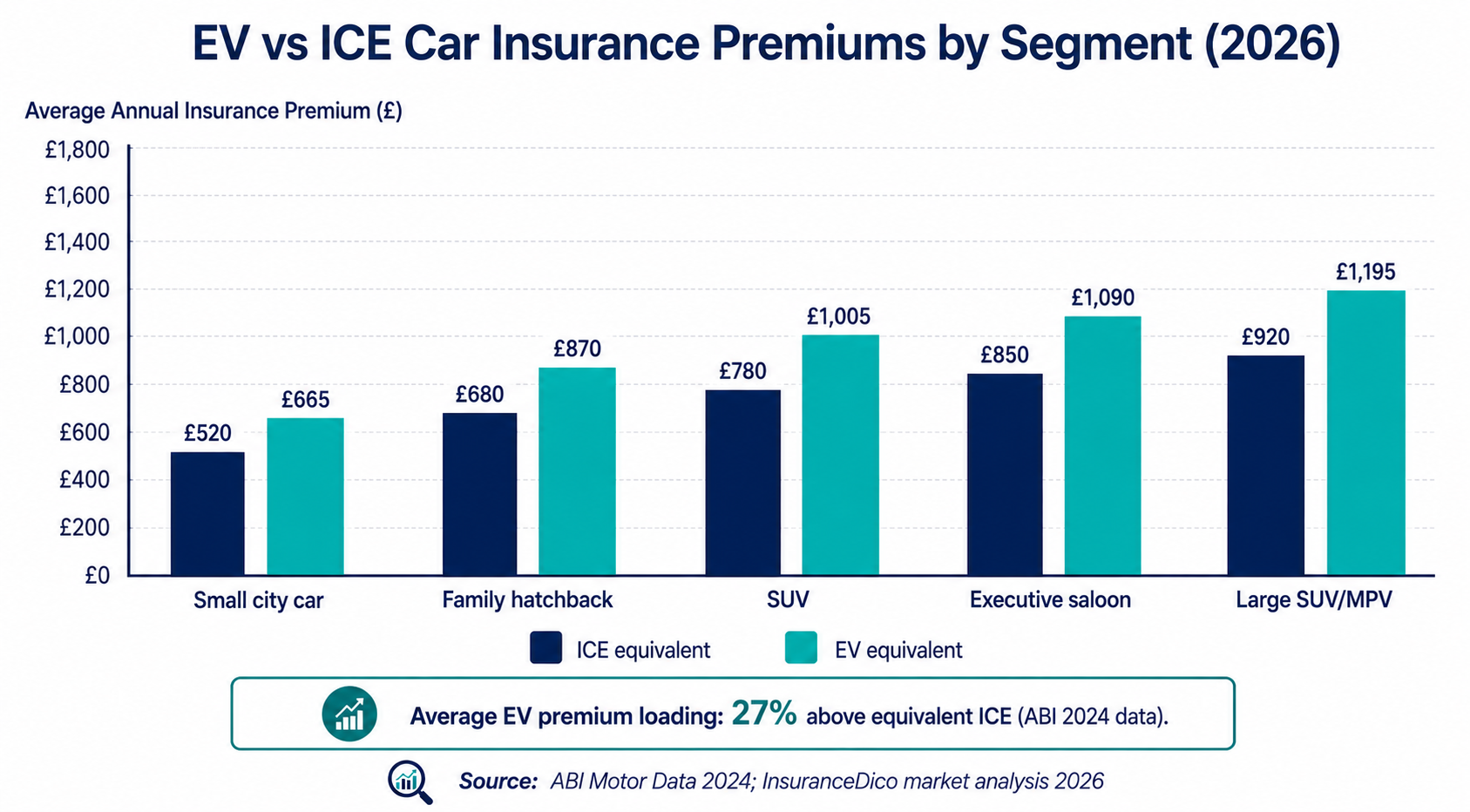

Electric vehicle insurance costs on average 25–30% more than equivalent petrol or diesel models according to ABI data for 2024. The premium gap exists because EV repair costs are higher (specialist high-voltage technicians, longer repair times), battery replacement exposure is significant (£8,000–£18,000 per pack), and EV parts supply chains are less mature than ICE equivalents. The gap is narrowing as battery costs fall and specialist repair networks expand. In 2026, the practical steps to reduce EV insurance include comparison shopping (EV pricing varies significantly between insurers), increasing your excess, and choosing the right insurer for your specific EV model.

Why Electric Vehicle Insurance Costs More — the Actuarial Reasons

The premium gap between EV and ICE insurance is not arbitrary. It reflects three specific structural differences in the cost of insuring and repairing electric vehicles.

Reason 1 — Repair costs and specialist labour requirements

Modern EVs are significantly more complex to repair after a collision than equivalent ICE vehicles. The key cost drivers:

High-voltage battery system assessment: Before any bodywork repair can begin on a vehicle that has sustained a significant impact near the battery pack, the high-voltage system must be assessed and made safe by an accredited high-voltage (HV) technician. This assessment takes 2–4 hours per repair event and must be completed regardless of whether the battery was damaged. It cannot be skipped.

HV-accredited bodyshops: Not all repair facilities are accredited to work on high-voltage vehicles. As of 2026, approximately 35–40% of UK bodyshops have HV accreditation — compared with effectively 100% for ICE vehicles. The restricted approved repair network means longer vehicle transit times to reach an accredited facility, longer repair times, and higher labour costs at facilities where HV skills command a premium.

Sensor-dense structures: Modern EVs — particularly those from 2020 onwards — carry a higher density of cameras, LIDAR sensors, radar units, and ultrasonic sensors embedded in bumpers and body panels than equivalent ICE vehicles. Replacing a sensor-integrated bumper on a 2023 EV costs £800–£1,800 for the sensor alone, before repair labour.

Reason 2 — Battery replacement exposure

The high-voltage traction battery is the most expensive single component of any EV. Replacement costs vary by model and battery size:

| Vehicle Category | Battery Pack Size | Approximate Battery Replacement Cost |

|---|---|---|

| Small city EV (e.g. Nissan Leaf 40kWh) | 40 kWh | £8,000–£12,000 |

| Family hatchback EV (e.g. VW ID.3 Pro) | 58–77 kWh | £12,000–£18,000 |

| Family SUV EV (e.g. Tesla Model Y) | 60–82 kWh | £14,000–£22,000 |

| Premium EV (e.g. BMW iX) | 65–105 kWh | £18,000–£30,000+ |

A battery pack that is significantly damaged in a collision — cracked cells, compromised cooling system, structural deformation — may require full replacement even if the vehicle's bodywork damage appears modest. This disproportionate repair cost relative to apparent damage is the primary driver of higher total loss decisions on EVs.

Reason 3 — Vehicle value

EVs carry a purchase price premium over equivalent ICE models. Higher vehicle values produce higher comprehensive claim payouts in theft, fire, or total loss scenarios — all of which load the insurer's expected claims cost and flow directly into higher premiums.

What EV Insurance Covers — and the EV-Specific Elements to Check

Standard comprehensive EV insurance covers the same risks as comprehensive ICE insurance: third-party claims, own vehicle damage, theft, fire, windscreen. The following EV-specific elements require specific attention.

Battery coverage — damage vs degradation

Damage to the battery (insurable): Mechanical damage to the battery pack caused by a collision, fire, flood, or other insured event is covered under comprehensive insurance. A battery pack that is cracked, punctured, or thermally damaged in a road incident is an insurable claim.

Battery degradation (not insurable): All lithium-ion batteries gradually lose capacity over time and charge cycles. A battery that has degraded from 100% to 82% capacity after 60,000 miles of use is functioning as designed — this is normal wear and tear, not an insured event. No insurance product covers gradual capacity degradation.

The warranty vs insurance distinction: Most new EVs carry a manufacturer battery warranty — typically 8 years or 100,000 miles at 70% capacity retention. Battery failure covered by the manufacturer warranty is a warranty claim, not an insurance claim. Battery damage from an accident is an insurance claim.

Home charging equipment

The coverage gap: Standard home insurance policies cover home electrical installations as part of buildings coverage. An EV wall box (home charging unit) is permanently installed — it is buildings, not contents. Most home insurance policies cover the wall box under buildings insurance for the standard perils.

The EV insurance connection: Some comprehensive EV insurance policies explicitly extend coverage to include home charging equipment — covering the wall box for accidental damage, theft, and fire as part of the motor insurance rather than requiring a buildings claim. Check both your EV insurance and home insurance for this coverage to avoid both a gap and duplication.

Public charging cable: The charging cable carried in the vehicle is covered as contents/personal possessions rather than as motor insurance in most standard policies. If your charging cable is stolen from the car, this is typically a contents claim (if you have personal possessions cover) rather than a motor claim.

Public charging liability

If your EV charging cable damages a public charging station — a connection fault, an overheating event, physical damage — your motor insurance's third-party property damage coverage responds. This is a standard element of comprehensive motor insurance that applies to EVs as to ICE vehicles. No additional EV-specific coverage is required.

2026 EV Insurance Premium Data by Model Category

EV insurance premiums vary significantly by vehicle model. Insurance group ratings for EVs take into account: vehicle value, battery replacement cost, repair network availability, vehicle performance, and theft risk.

| EV Model Category | Insurance Group (Approx.) | Indicative Annual Premium |

|---|---|---|

| Small city EV (MG4, BYD Dolphin, Vauxhall Corsa Electric) | 18–28 | £650–£1,050 |

| Family hatchback EV (VW ID.3, BMW i3, Renault Zoe) | 25–35 | £820–£1,350 |

| Family SUV EV (Tesla Model Y, Kia EV6, Hyundai Ioniq 5) | 30–42 | £980–£1,580 |

| Executive saloon EV (Tesla Model 3, BMW i4, Polestar 2) | 32–45 | £1,050–£1,720 |

| Premium SUV EV (BMW iX, Mercedes EQS, Audi e-tron GT) | 42–50 | £1,650–£2,800 |

How to Reduce Your EV Insurance Premium

Compare specifically for EVs — not just generally

EV insurance pricing varies more between insurers than ICE insurance. Some insurers have substantial EV claims data and price accurately; others are still calibrating to EV risk and price either too high (cautiously) or too low (to win market share). Running a full market comparison specifically for your EV model produces meaningfully different results than assuming the insurer who was cheapest for your previous ICE vehicle will also be cheapest for your EV.

The insurers with the strongest 2026 EV proposition include: LV= (Liverpool Victoria), Direct Line, Aviva, and Admiral — all of whom have invested in HV repair network partnerships and EV underwriting expertise. Tesla Insurance launched in the UK in limited form in 2024 — where available, it uses vehicle telematics data from the Tesla app to price the policy.

Increase your voluntary excess

The principle is the same as for ICE vehicles — increasing from the standard excess to a higher voluntary excess reduces the premium. On an EV where the risk profile is higher, the premium saving from a £500 excess increase is proportionally larger than on equivalent ICE insurance.

Choose your charging tariff strategically for insurance purposes

Some insurers are beginning to offer discounts for EVs charged predominantly on off-peak tariffs (overnight charging between 11pm and 7am) — the rationale being that drivers on time-of-use tariffs are more engaged, predictable users. This is an emerging trend rather than universal practice in 2026 — check at comparison.

Consider a mileage-based policy

For EV owners using their vehicle primarily for local commuting and covering fewer than 7,000 miles per year, a pay-per-mile policy (available from By Miles and a small number of other providers) may produce significantly lower annual costs than a fixed premium. EVs tend to be lower-mileage for many households because they are the primary commuting vehicle with a longer-range ICE kept for trips. Mileage-based pricing rewards this pattern.

“Mechanical damage to an EV battery is insurable; gradual capacity degradation is not. Know which side of that line your battery issue falls on before you call your insurer or the manufacturer.”