UK car insurance is offered at three levels — third party only (TPO), third party fire and theft (TPFT), and comprehensive. TPO is the legal minimum. Comprehensive covers your own vehicle damage in addition to third-party claims. The counterintuitive finding: comprehensive is sometimes cheaper than TPFT for higher-risk drivers, because riskier drivers disproportionately choose TPFT, making that pool more expensive to insure. For most drivers with a vehicle worth more than £3,000, comprehensive cover delivers more protection at comparable or lower cost than TPFT.

The Three Levels of UK Car Insurance — What Each Covers

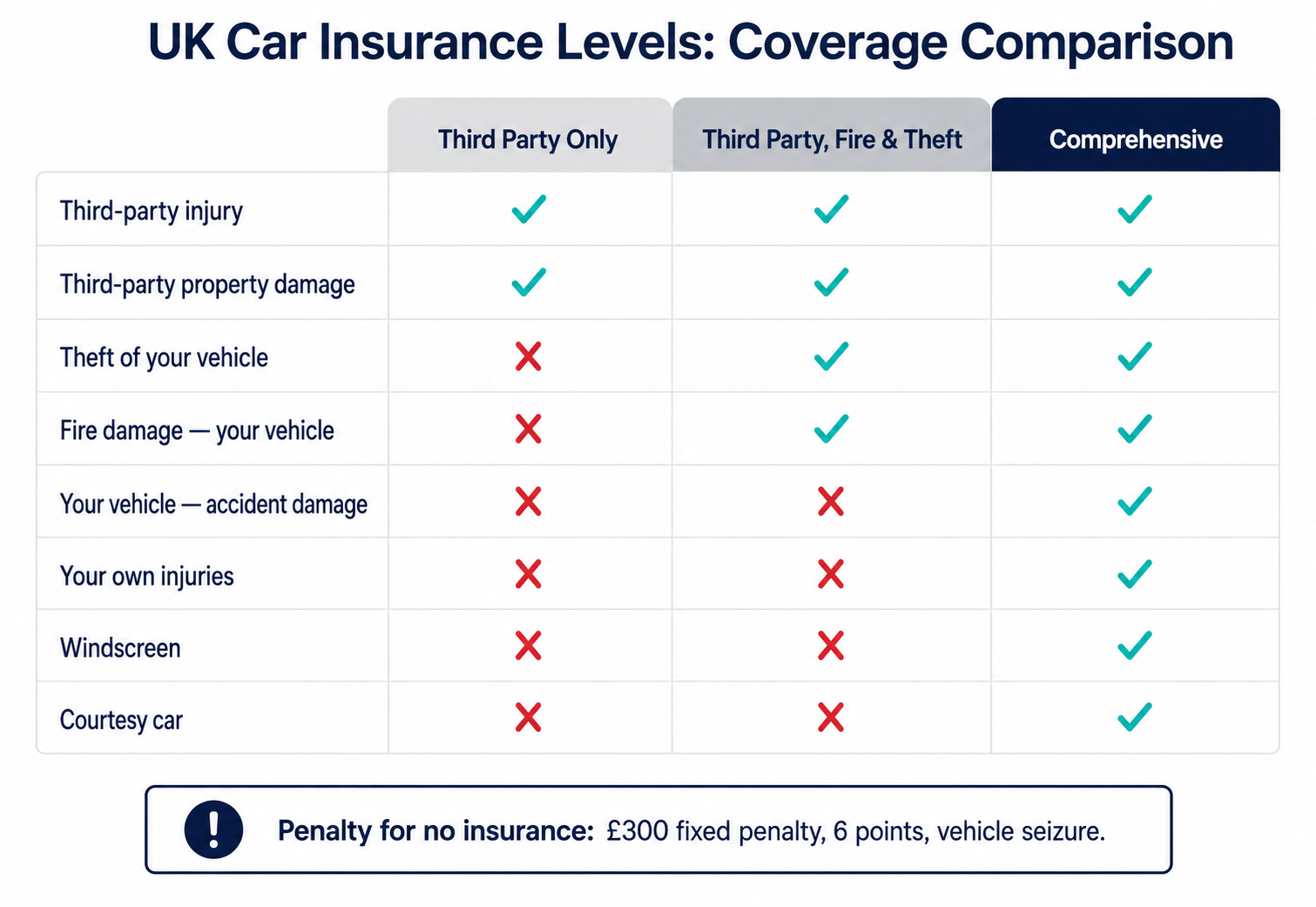

UK motor insurance law requires a minimum of third-party cover for any vehicle on a public road. Beyond this, drivers choose their level based on the value of their vehicle, their financial exposure, and their premium budget.

Third Party Only (TPO) — the legal minimum

TPO covers claims made against you by other parties. If you cause an accident that injures someone or damages their vehicle or property, your TPO insurer pays those third-party costs.

What TPO covers:

- Injury to other people (including passengers in the other vehicle)

- Damage to other vehicles

- Damage to third-party property (walls, gates, parked cars)

- Legal costs for defending third-party claims

What TPO does not cover:

- Damage to your own vehicle — regardless of fault

- Theft of your vehicle

- Fire damage to your vehicle

- Your own injuries (unless another party's insurer is liable)

- Windscreen damage

Who TPO is genuinely appropriate for: Vehicles with a market value below approximately £1,000–£1,500 where the cost of comprehensive or TPFT premiums approaches or exceeds the vehicle's value. In these cases, self-insuring your own vehicle risk is economically rational because the maximum you could recover is less than the additional premium you would pay.

Third Party, Fire and Theft (TPFT)

TPFT covers everything TPO covers, plus theft of your vehicle or attempted theft, and fire damage to your vehicle (including arson).

What TPFT still does not cover: damage to your own vehicle in an accident you cause, your own injuries, windscreen damage, or accidental damage of any kind to your vehicle. TPFT's additional coverage over TPO is relevant only if your vehicle is stolen or catches fire. It adds no protection for the most common type of own-vehicle loss: accident damage.

Comprehensive

Comprehensive covers all of the above plus:

- Damage to your own vehicle regardless of fault — if you cause an accident, hit a pothole, or are the victim of a hit-and-run

- Your own injuries as driver (personal accident cover, typically up to £5,000–£100,000 depending on the policy)

- Windscreen repair and replacement

- Driving other cars (some policies — TPO basis only while driving another car)

- Courtesy car while your vehicle is repaired

What comprehensive does not cover: mechanical or electrical breakdown (separate warranty or breakdown cover), wear and tear, damage to your vehicle by someone else who is uninsured (you claim on your own comprehensive policy and your insurer pursues the Motor Insurers' Bureau), and deliberate damage by you.

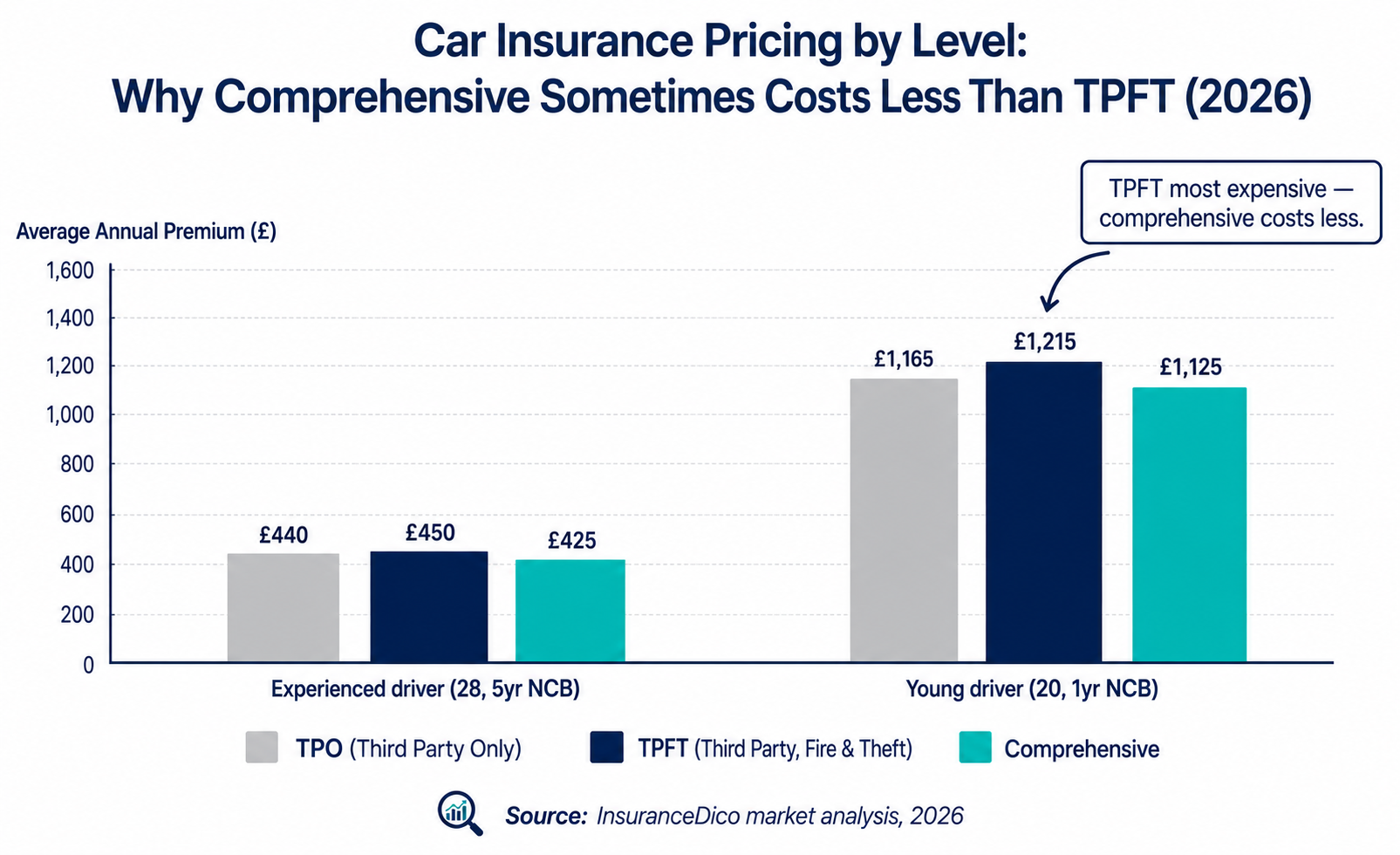

The Counterintuitive Pricing Reality — Why Comprehensive Is Sometimes Cheaper Than TPFT

This is the most important, most actionable, and least discussed finding in UK motor insurance pricing.

The expectation: A higher coverage level should cost more. Comprehensive provides more coverage than TPFT, so it should cost more.

The reality: For certain driver profiles — particularly younger and higher-risk drivers — comprehensive car insurance is frequently priced lower than TPFT.

The actuarial explanation

Insurers price policies based on the statistical claims experience of the pool of drivers choosing that product. Drivers who choose TPFT tend to be higher-risk for two reasons:

- Self-selection: Drivers who cannot afford or who choose not to pay for comprehensive cover disproportionately represent higher-risk profiles — younger drivers, those with recent claims, those with modified vehicles.

- Vehicle profile: TPFT is chosen predominantly for older, lower-value vehicles. These vehicles are disproportionately driven by younger drivers or those with shorter driving experience.

The claims experience of the TPFT pool reflects this higher-risk profile. Premiums for TPFT are therefore higher per unit of coverage than comprehensive — because you are being rated in a pool that statistically claims more.

The practical consequence: A 22-year-old driver may be quoted £1,020 per year for TPFT and £980 for comprehensive on the same vehicle. The comprehensive policy provides substantially more coverage at a lower price. The correct decision — always — is to accept the comprehensive quote.

When Each Level of Cover Is the Right Choice

When TPO is appropriate

Scenario: The vehicle is worth less than £1,000. You are a young driver paying high premiums. The annual comprehensive premium approaches or exceeds the vehicle's value.

Example: A 19-year-old insuring a 2009 Vauxhall Corsa valued at £850. Comprehensive premium: £1,200. TPFT premium: £1,050. TPO premium: £950. The vehicle is worth less than any of the three annual premiums. The maximum own-vehicle claim is £850. Paying £250 more per year for TPFT to protect an £850 vehicle is economically irrational. TPO at £950 transfers the third-party liability risk — the one that is legally required and potentially unlimited — at the lowest available cost.

The one caveat with TPO: If the vehicle is financed, the finance provider almost certainly requires comprehensive coverage. TPO on a financed vehicle is a breach of the finance agreement.

When TPFT is the right level

Scenario: The vehicle is worth £2,000–£6,000 and the theft or fire risk is genuine (older vehicles without modern immobilisers in higher-theft areas). The TPFT premium is meaningfully below comprehensive.

When this genuinely occurs: Less common than buyers assume, because of the pricing paradox described above. TPFT is most appropriate for mid-value vehicles in circumstances where the theft risk is the primary concern and the accident damage risk is lower (low-mileage older drivers, vehicles used only seasonally).

When comprehensive is almost always the right choice

Scenario: Your vehicle is worth more than £3,000. You drive regularly. You cannot comfortably self-fund a repair bill of £2,000–£8,000 if you cause an accident.

The logic: The most common own-vehicle loss event is collision damage — not theft, not fire. TPFT provides no protection against collision damage to your own vehicle. If your car is worth £12,000 and you rear-end another vehicle at a roundabout, TPFT pays the other driver's claim. Your £12,000 car is your problem.

The data point: The average comprehensive own-vehicle damage claim in the UK is £3,200 (ABI 2023 Motor Statistics). For most drivers, self-funding this figure from reserves is uncomfortable. Comprehensive insurance transfers this risk for a marginal additional premium in most cases.

The Real Cost Comparison — 2026 Market Data

The following tables show indicative 2026 quotes for the same driver and vehicle at each coverage level, demonstrating the pricing relationships.

Scenario: 28-year-old driver, clean licence, 5-year NCB, 2021 Ford Focus, 8,000 miles per year, standard postcode.

| Coverage Level | Indicative Annual Premium | What You Gain vs Previous Tier |

|---|---|---|

| Third Party Only | £385–£495 | Legal minimum only |

| Third Party Fire & Theft | £395–£510 | Theft and fire protection for own vehicle |

| Comprehensive | £365–£490 | Own vehicle damage, windscreen, personal accident |

In this example, comprehensive is cheaper than TPFT — illustrating the counterintuitive pricing dynamic. The incremental cost of comprehensive over TPO is effectively zero.

Scenario: 20-year-old driver, 1-year NCB, 2019 Volkswagen Polo, 6,000 miles per year, urban postcode.

| Coverage Level | Indicative Annual Premium | Notes |

|---|---|---|

| Third Party Only | £980–£1,280 | Legal minimum only |

| Third Party Fire & Theft | £1,050–£1,380 | TPFT more expensive than comprehensive |

| Comprehensive | £980–£1,270 | Comprehensive ≈ TPO; provides far more coverage |

“Comprehensive car insurance is sometimes priced lower than third party fire and theft for higher-risk driver profiles — because drivers who choose TPFT disproportionately represent higher-risk demographics, making the TPFT pool more expensive per unit of coverage.”