Wedding insurance covers the financial loss from cancelling or postponing your wedding due to circumstances beyond your control — venue insolvency, supplier failure, serious illness, bereavement, or severe weather. The average UK wedding cost was £19,184 in 2025 according to Hitched.co.uk, making it the single largest one-day expenditure most couples make. Wedding insurance costs £70–£200 for most weddings and should be purchased as soon as the first deposit is paid — not in the weeks before the wedding. Fewer than 15% of UK couples insure their wedding according to the Wedding Planning Association, despite the financial exposure.

UK wedding insurance is a single-event personal lines policy that reimburses irrecoverable wedding costs across six coverage categories — cancellation and rearrangement, venue failure, supplier failure, attire, rings and gifts, and public liability — when a covered event prevents the wedding proceeding as planned.

What Wedding Insurance Covers — the Complete Breakdown

Wedding insurance is not a single coverage type — it addresses multiple distinct financial risks across six coverage categories. Understanding each category separately prevents both gaps and false expectations.

1. Cancellation and Rearrangement

The core element. Covers the irrecoverable deposits, booking fees, and non-refundable payments if the wedding must be cancelled or postponed due to a covered event.

Covered reasons for cancellation:

- Serious illness or injury to either partner or an immediate family member that prevents the wedding taking place

- Death of the couple or an immediate family member

- Redundancy of either partner (where the wedding budget was primarily funded by employment income)

- Severe weather making the venue inaccessible or dangerous to attend

- FCDO travel advice issued against the wedding destination (for destination weddings)

- Major damage to the couple's home requiring their presence

The cancellation limit must match your irrecoverable costs. The policy cancellation limit is the maximum the insurer will pay. If your wedding has £22,000 of non-refundable deposits and bookings, a policy with a £10,000 cancellation limit leaves £12,000 uninsured. When purchasing, total all irrecoverable costs — venue deposit, catering deposit, photographer booking fee, dress payment, honeymoon deposit — and ensure the cancellation limit covers the full amount.

2. Venue Failure

Covers financial loss when the wedding venue cannot fulfil the booking — due to insolvency, ceasing trading, or being rendered unsuitable through no fault of the couple.

Why this is increasingly relevant: Post-COVID, the UK hospitality and events sector saw a wave of venue closures and insolvencies. A venue that accepts a wedding deposit and then ceases trading before the event leaves the couple with both the lost deposit and the challenge of finding an alternative venue at short notice.

Wedding insurance paying out on venue insolvency covers: the lost deposit or advance payments to the venue, reasonable additional costs of finding and booking an alternative venue at comparable quality, and any difference in cost if the alternative is more expensive.

3. Supplier Failure

Covers financial loss when a supplier fails to provide their service on the wedding day — through insolvency, ceasing trading, or simply not arriving.

Covered suppliers typically include:

- Caterers and catering companies

- Wedding photographers and videographers

- Wedding bands, DJs, and entertainers

- Wedding car and transport providers

- Florists

- Wedding cake suppliers

The coverage applies: the deposit lost if the supplier is insolvent, plus the reasonable additional cost of sourcing a last-minute replacement at equivalent quality.

4. Wedding Attire

Covers loss, theft, or damage to the wedding dress, groom's attire, and bridesmaid dresses. Coverage applies from purchase to the day of the wedding.

Coverage limits: Standard wedding insurance policies typically cover attire up to £2,500–£5,000 for the wedding dress. Individual policies vary — if your dress cost £4,000 and the policy limit is £2,500, there is a £1,500 gap. Check the specific attire limit against the actual cost when purchasing.

What this covers in practice: A dress damaged in transit to the venue, a dress lost by the dry cleaner in the weeks before the wedding, or a dress destroyed in a fire at the bridal boutique before collection.

5. Wedding Rings and Gifts

Rings: Loss, theft, or accidental damage to the wedding rings before and on the wedding day. Standard coverage is £500–£1,500 for the ring category. For rings worth more than the policy limit, specific declaration may be needed — the same principle as single-item limits in home contents insurance.

Gifts: Coverage for wedding gifts damaged, lost, or stolen at the venue. Standard limits are £2,000–£5,000 for the gift category. This covers the physical gifts present at the venue — not cash gifts transferred by bank transfer.

6. Public Liability

Covers the couple's legal liability if their wedding arrangements cause injury to guests or damage to the venue. This is particularly relevant for:

- Couples who hire the venue and have organised their own suppliers (rather than using the venue's own catering and entertainment)

- Weddings with children's entertainment, marquees, or activities with physical risk

- Damage to the venue that the couple are contractually liable for

Most licensed wedding venues require evidence of public liability cover — either from the couple's wedding insurance or from each individual supplier. A wedding insurance policy with £2m of public liability typically satisfies this requirement.

What Wedding Insurance Does Not Cover

Understanding the exclusions prevents the most common post-claim disappointments.

Cold feet / change of mind: Wedding insurance is not purchasable against the risk of either party changing their mind. If the wedding is cancelled because the relationship ends, no valid claim exists. The policy covers circumstances genuinely beyond the couple's control — not a voluntary decision to cancel.

Pre-existing venue or supplier problems: As noted, any problem with a venue or supplier that existed or was known about before the policy was taken out is a known circumstance and is excluded. The policy must be purchased before any difficulties become apparent.

Pandemic and epidemic (most policies): Most wedding insurance policies issued from 2022 onwards explicitly exclude pandemic and epidemic-related cancellation. If a new pandemic forces venue closure, this exclusion typically applies. Some specialist policies have partially reinstated limited COVID coverage — check the specific wording.

Undisclosed pre-existing health conditions: If cancellation is due to a medical condition that existed before the policy was taken out and was not declared, the claim may be excluded. Some policies ask health questions at application; others rely on general non-disclosure rules.

Contractual liability beyond standard: Wedding insurance's public liability covers the couple's standard legal duty of care. If the couple has accepted unlimited liability in a venue contract, the excess above standard legal liability is not automatically insured.

How Much Does Wedding Insurance Cost?

Wedding insurance is one of the most cost-effective insurance products relative to the value it protects. The premium represents a fraction of one percent of the average wedding budget.

| Wedding Budget | Standard Cover | Comprehensive Cover | With Public Liability |

|---|---|---|---|

| Up to £7,500 | £50–£75 | £75–£115 | £80–£130 |

| £7,500–£15,000 | £65–£100 | £100–£155 | £110–£175 |

| £15,000–£25,000 | £85–£135 | £135–£205 | £150–£230 |

| £25,000–£40,000 | £120–£185 | £185–£280 | £205–£315 |

| £40,000–£75,000 | £180–£280 | £280–£430 | £310–£480 |

| Above £75,000 | Specialist placement | Specialist placement | Contact broker |

The financial case for purchasing: At £19,184 average wedding cost and a premium of approximately £120–£170 for standard comprehensive cover, wedding insurance costs less than 1% of the wedding budget and protects 100% of the irrecoverable deposits against the most common risk events.

The average wedding insurance claim paid in the UK is approximately £4,500 — significantly above the typical annual premium. The most common claims are supplier failure and cancellation due to illness.

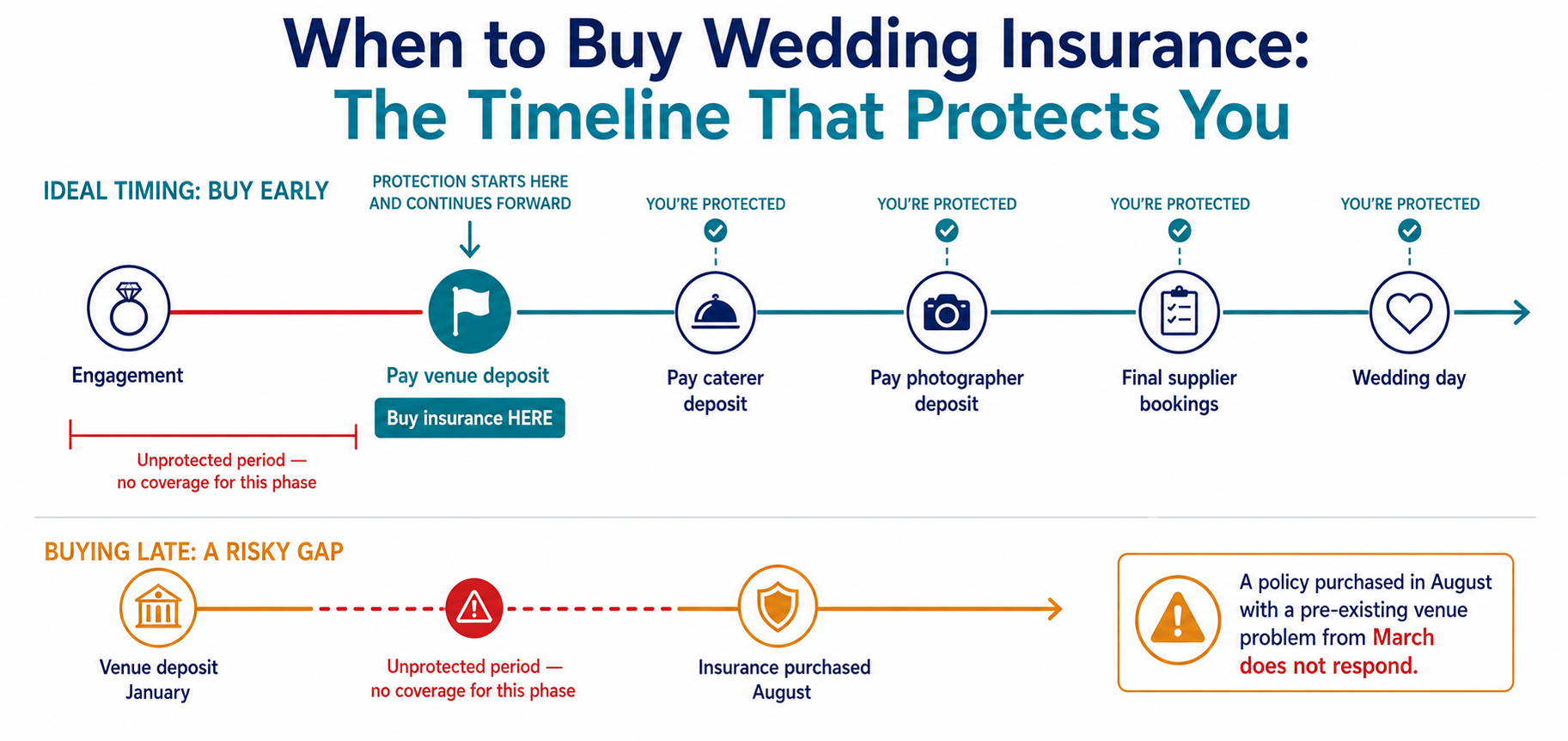

When to Buy — the Most Important Single Decision

Buy as soon as the first deposit is paid.

This is not a recommendation — it is a structural requirement of how wedding insurance works. Cancellation coverage applies from the date the policy starts. If you pay a £3,000 venue deposit in January, plan the wedding for the following October, and purchase insurance in August, any cancellation event that occurs between January and August is entirely uninsured.

The most common scenario that catches couples out: A couple pays a venue deposit in January. In March, one partner's parent becomes seriously ill. In April, the parent's condition worsens and the family decides the wedding cannot proceed in October. The couple had planned to buy insurance 'nearer the time.' The illness — which is now the cause of the cancellation — predates the policy and is a pre-existing known circumstance for the policy purchased in April.

Had they purchased in January, the policy would have been in force from the date of the first payment. The March illness would have been an unexpected event occurring during the policy period, producing a valid claim.

Destination Weddings — the Additional Considerations

Wedding insurance for ceremonies held abroad requires specific attention to several additional factors:

FCDO travel advice: If the FCDO issues 'advise against all travel' to your destination before the wedding, most wedding insurance policies activate the cancellation benefit for irrecoverable UK costs. Additional travel and accommodation costs for guests are generally not covered — guests would need their own travel insurance.

Local venue and supplier failure: Wedding insurance covering supplier failure abroad may require specific evidence of the supplier's failure that can be more difficult to obtain from overseas vendors. Keep all contracts and correspondence.

Currency risk: If your wedding costs are primarily in a foreign currency and the GBP weakens significantly between booking and the wedding, the sterling value of your coverage may not match the cost in local currency. Check whether your policy covers actual costs or uses a fixed sterling equivalent.

Guest travel costs: Standard wedding insurance does not cover the travel and accommodation costs that guests incur — these are each guest's own financial exposure under their personal travel insurance.

The Main UK Wedding Insurance Providers

Dreamsaver: One of the most established UK wedding insurance specialists. Clear coverage tiers, straightforward claims process. Available online and through brokers. Cancellation limits from £5,000 to £50,000+.

Wedinsure: Specialist wedding insurer with flexible coverage options. Competitive for larger budget weddings. Strong supplier failure coverage terms.

Ecclesiastical: Specialist insurer with strong heritage in venue and event coverage. Often the preferred insurer for religious ceremony venues. Also covers marquee weddings.

Emerald Life: LGBTQ+ inclusive wedding specialist. Broad coverage with a specifically inclusive approach to defining covered parties and relationships.

Towergate Wedding Insurance: Broad coverage, competitive premiums for standard UK weddings. Available through comparison sites and direct.

John Lewis Finance Wedding Insurance: Familiar brand, straightforward coverage for mid-budget weddings. Available through John Lewis Financial Services.

Frequently Asked Questions

Key takeaways

- Wedding insurance covers cancellation, venue and supplier failure, attire, rings and gifts, and public liability — at typically under 1% of the wedding budget.

- Buy it the day the first deposit is paid: cancellation cover applies from the policy start date, so any event before purchase is excluded as a known circumstance.

- Match the cancellation limit to your total irrecoverable costs, and read the pandemic, cold-feet, and key-guest exclusions before relying on cover.