Pet insurance pays vet bills when your pet is ill or injured. There are four policy types in the UK — lifetime, annual maximum benefit, time-limited, and accident-only — and only lifetime cover is genuinely adequate for pets that develop chronic conditions such as diabetes, arthritis, or allergies. The PDSA estimates that only 4.1 million of the UK's 25 million pets are insured. The average vet bill for a single serious condition exceeds £1,500 — and conditions like cruciate ligament rupture (£2,800–£5,500) or cancer (£3,500–£10,000) represent costs most households cannot absorb without insurance.

UK pet insurance is a personal lines policy that reimburses veterinary costs for accidents and illnesses, structured in four cover types — lifetime, annual maximum benefit, time-limited and accident-only — that differ fundamentally in how they handle ongoing conditions.

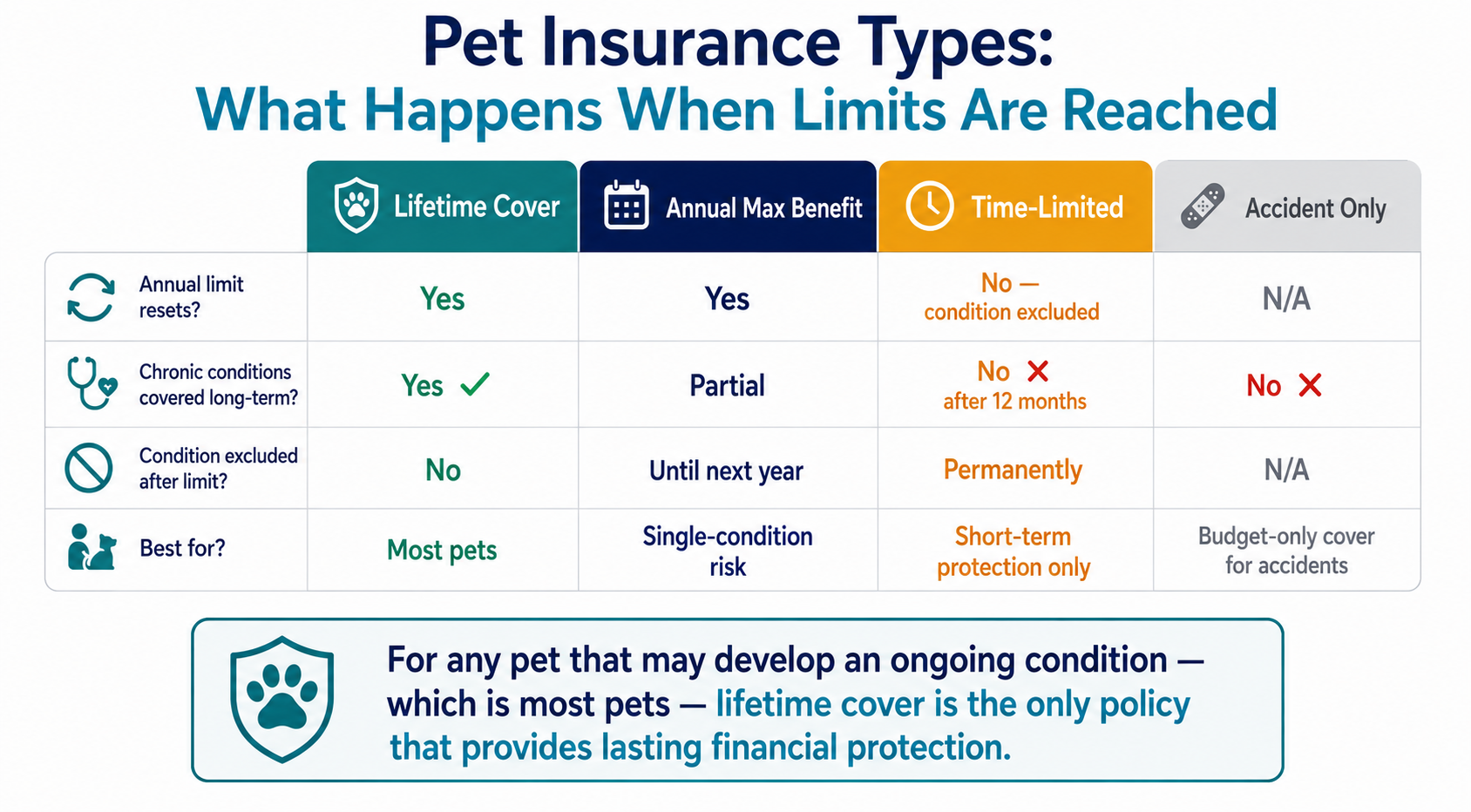

The Four Types of Pet Insurance — Why the Distinction Is Critical

Most buyers compare pet insurance on price. The more important comparison is coverage type — because the type of policy determines whether the insurance pays when it matters most.

Type 1 — Lifetime Cover (the Correct Choice for Most Pet Owners)

Lifetime cover provides a defined annual vet fee limit per policy year which resets at every annual renewal. A policy offering £8,000 per year of lifetime cover replenishes to £8,000 at each anniversary — regardless of what was claimed in the previous year.

Why this matters: When a pet develops a condition that requires ongoing management — diabetes, epilepsy, arthritis, allergies, heart disease — a lifetime policy continues to fund that condition indefinitely, year after year, as long as the policy is renewed without a break.

The one critical rule with lifetime cover: Never allow the policy to lapse or switch insurer once a chronic condition is diagnosed. A condition that has been treated under your current policy becomes pre-existing for any new insurer — and is permanently excluded from the new policy. Renew without interruption.

Type 2 — Annual Maximum Benefit (Frequently Misunderstood)

Annual maximum benefit policies provide a fixed limit per condition per year. Once that limit is reached, the condition is excluded for the remainder of that policy year. At renewal, the limit resets — and the condition is covered again for the new year.

How this differs from lifetime: Annual maximum benefit resets per condition per year. Lifetime cover resets as a total pool per year. For pets with multiple ongoing conditions, lifetime cover is generally more valuable.

Where this type works well: Pets in good health where the risk of multiple simultaneous conditions is low, and where a per-condition annual limit is sufficient for most realistic claim scenarios.

Type 3 — Time-Limited Cover (the Most Commonly Misunderstood Type)

Time-limited policies cover each new condition for 12 months from the date of first treatment, and up to a defined financial limit for that condition. Once either the 12-month period or the financial limit is reached — whichever comes first — the condition is permanently excluded from the policy.

The consequence most buyers miss: If your dog develops arthritis at age four and you hold a time-limited policy, the arthritis is covered for 12 months. After that, it is excluded permanently — for the rest of the dog's life. Future treatment costs for that condition, which may run for 10 years, are entirely your expense.

Time-limited policies are significantly cheaper than lifetime cover. They appear superficially similar at the point of sale. They are not comparable when a pet develops a condition requiring ongoing management.

Type 4 — Accident Only (the Minimum Level of Cover)

Accident-only policies cover veterinary treatment following accidents — injuries from road traffic accidents, falls, bites, and foreign body ingestion — but not illness of any kind. A pet that develops cancer, diabetes, a heart condition, or an infection is not covered.

Who this is appropriate for: Owners who genuinely cannot afford lifetime or annual cover but want protection against the catastrophic accident costs (a road traffic accident involving a dog can cost £4,000–£8,000 in surgery alone). It provides limited but real financial protection where budget is severely constrained.

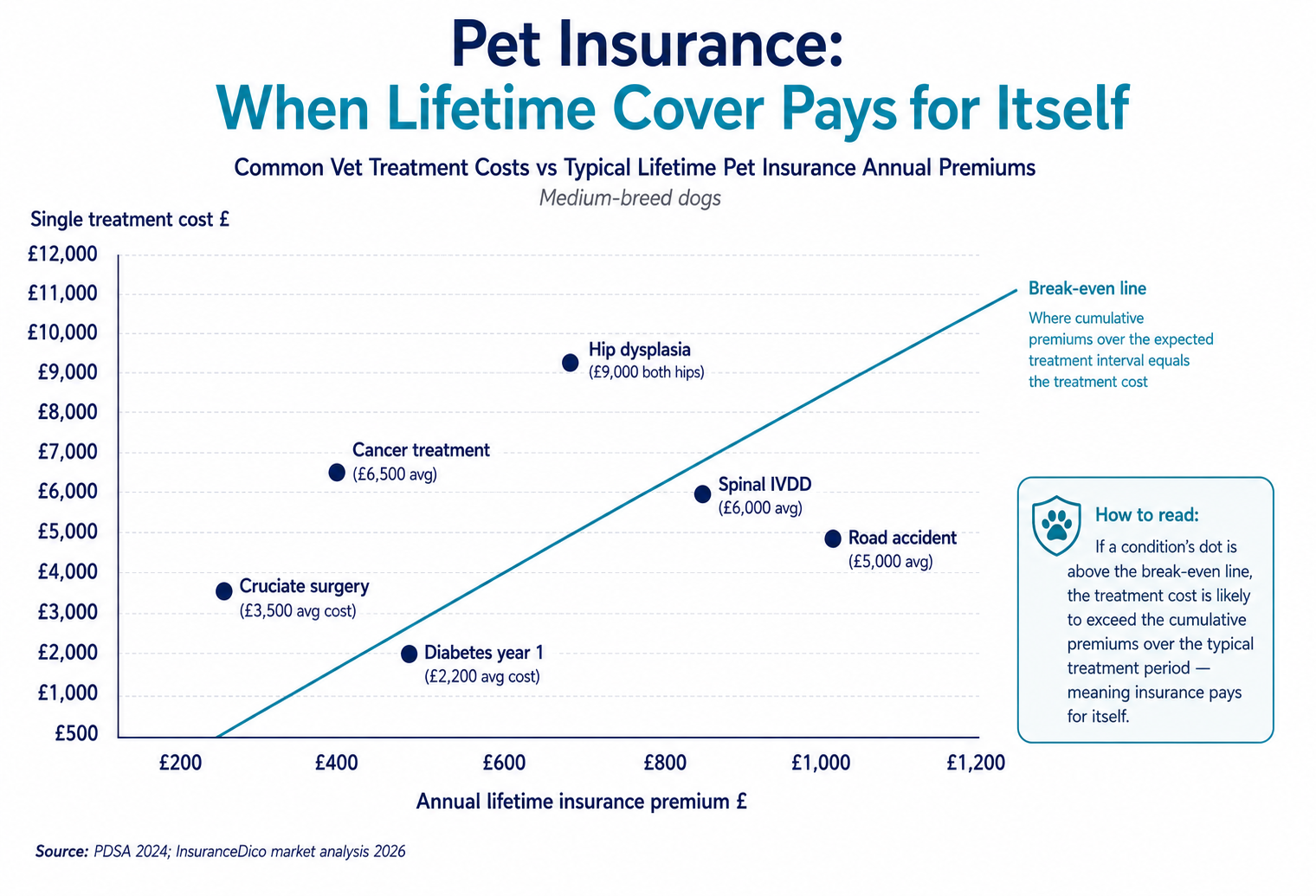

The Real Cost of Veterinary Treatment — What Pet Insurance Actually Protects

The case for pet insurance is primarily financial. These are not worst-case scenarios — they are common presentations at UK veterinary practices:

| Condition | Pet Type | Average Treatment Cost |

|---|---|---|

| Cruciate ligament rupture | Dog (medium-large breed) | £2,800–£5,500 per leg |

| Cancer diagnosis and treatment | Dog or cat | £3,500–£10,000+ |

| Hip dysplasia (both hips) | Dog (large breed) | £7,000–£16,000 |

| Diabetes — diagnosis and first year | Dog or cat | £1,500–£3,000 |

| Diabetes — annual ongoing management | Dog or cat | £800–£1,500/year |

| Spinal disc disease (IVDD) | Dog | £4,000–£8,000 |

| Road traffic accident surgery | Dog or cat | £3,000–£8,000 |

| Pyometra (emergency surgery) | Female dog | £1,200–£3,500 |

| Obstructive urinary tract | Cat (male) | £1,000–£2,500 |

| Skin allergies — ongoing management | Dog | £600–£1,500/year |

The lifetime cost context: A Labrador Retriever with a 12-year lifespan faces statistically significant risk of hip or elbow dysplasia (high prevalence in the breed), cruciate ligament problems (moderate prevalence), and age-related conditions in later years. Insuring a Labrador from puppyhood on a lifetime policy and maintaining it throughout produces a total premium cost of approximately £8,000–£14,000 over 12 years. A single cruciate surgery plus hip treatment could cost £10,000+ in a single year.

2026 Pet Insurance Premiums — What to Expect

Pet insurance premiums depend on: species (dog typically costs more than cat), breed, age at first policy, where you live (London and South-East attract higher premiums), and the level of cover selected.

Dog Insurance — Monthly Premium Ranges by Breed Group (Lifetime Cover)

| Breed Group | Age 0–2 | Age 3–5 | Age 6–8 | Age 8+ |

|---|---|---|---|---|

| Small breed, low risk (Chihuahua, Miniature Schnauzer) | £18–£32 | £22–£42 | £35–£65 | £55–£110 |

| Medium breed, average risk (Labrador, Spaniel) | £25–£45 | £32–£58 | £50–£90 | £80–£155 |

| Large breed, higher risk (German Shepherd, Golden Retriever) | £32–£58 | £42–£75 | £65–£115 | £105–£195 |

| Brachycephalic breeds (French Bulldog, Pug, English Bulldog) | £65–£130 | £85–£170 | £130–£260 | £195–£395 |

Cat Insurance — Monthly Premium Ranges (Lifetime Cover)

| Cat Type | Age 0–3 | Age 4–7 | Age 8–10 | Age 10+ |

|---|---|---|---|---|

| Mixed breed (moggy) | £11–£20 | £14–£26 | £22–£42 | £38–£72 |

| Pedigree (British Shorthair, Siamese) | £16–£30 | £20–£38 | £32–£60 | £55–£105 |

Why Brachycephalic Breeds Cost So Much More to Insure

French Bulldogs, English Bulldogs, Pugs, Boston Terriers, and Shih Tzus are brachycephalic — characterised by shortened skull anatomy that causes compressed airways, overlong soft palates, and narrow nostrils. The conditions that result from this anatomy are structural, predictable, and expensive:

- Brachycephalic Obstructive Airway Syndrome (BOAS): Surgery to widen the nostrils and shorten the soft palate costs £1,500–£3,500 per procedure and is required in a significant proportion of affected dogs.

- Spinal conditions: French Bulldogs have elevated rates of spinal disc problems (IVDD) — surgery costs £4,000–£8,000.

- Eye problems: Prominent eyes in brachycephalic breeds are prone to ulcers and injuries requiring treatment.

Insurers price this known risk into premiums. Some specialist insurers apply loading on top of standard brachycephalic pricing for individual dogs assessed as higher risk.

Pre-Existing Conditions in Pet Insurance — the Permanent Exclusion Rule

Unlike human health insurance, where pre-existing conditions can sometimes be covered after a period of stability, pet insurance permanently excludes conditions that existed before the policy started.

The practical implication:

- A dog purchased at 8 weeks with a congenital hip condition will have that condition excluded for life from any insurance policy.

- A cat treated for urinary tract infections before the policy starts will have urinary conditions excluded permanently.

- A dog that developed skin allergies while uninsured will have allergy treatment permanently excluded from any policy taken out after the diagnosis.

This is the most important reason to insure your pet while it is young and healthy. The longer you wait, the higher the premium — and the greater the probability that a condition has already developed that will be permanently excluded.

What Pet Insurance Does Not Cover

Preventative and routine care: Vaccinations, flea and worm treatments, routine dental cleaning, and health check-ups are not insurable events under standard pet insurance. They are routine maintenance costs. Some pet care plans (offered by veterinary practices) cover routine preventative care on a subscription basis — these are not insurance but a payment plan for scheduled care.

Elective procedures: Neutering, microchipping, tail docking (illegal in most circumstances under the Animal Welfare Act 2006), and cosmetic procedures are not covered.

Pre-existing conditions: As described — permanently excluded.

Dental disease: Most pet insurance policies exclude dental disease arising from lack of dental care — a condition covered by the routine maintenance exclusion. Dental accidents (tooth fracture from biting something hard) may be covered under some policies. Check the specific dental terms carefully.

Cremation and burial costs: Third-party pet death and cremation costs are not covered under standard pet insurance. Some specialist providers offer a death and cremation benefit as an optional add-on.

Frequently Asked Questions

Key takeaways

- Lifetime cover is the only UK pet insurance type that funds chronic conditions year after year — time-limited and accident-only do not.

- Insure pets while young and healthy: pre-existing conditions are permanently excluded by every UK insurer and cannot be transferred between policies.

- Premiums vary sharply by breed and age — brachycephalic dogs cost 2–3× standard breeds and a single serious vet bill (£3,000–£10,000+) typically exceeds years of premiums.