Landlord insurance covers buy-to-let and rental properties against property damage, loss of rental income, legal expenses, and liability claims from tenants or their visitors. Standard home insurance explicitly excludes tenanted properties — a landlord who uses home insurance for a rented property has no valid cover. Most buy-to-let mortgage lenders require landlord buildings insurance as a condition of the mortgage. The average landlord insurance premium for a standard two-bedroom buy-to-let flat is £200–£380 per year for buildings-only cover.

Landlord insurance is a specialist UK property insurance product that covers buildings, property owners' liability, loss of rental income, and (optionally) contents, legal expenses and rent guarantee for residential properties let to tenants under an assured shorthold tenancy or equivalent.

Why Standard Home Insurance Does Not Work for Rental Properties

Standard residential home insurance is underwritten on the basis that the named policyholder occupies the property as their primary residence. The risk profile of an owner-occupied property and a tenanted property differ materially:

Higher claim frequency in tenanted properties: Research published by the Association of British Insurers consistently shows that tenanted properties generate higher claims frequency than owner-occupied equivalents — particularly for escape of water, accidental damage, malicious damage, and theft.

Legal liability to tenants: Landlords have a duty of care to tenants and their visitors under the Landlord and Tenant Act 1985, the Housing Act 2004, and related legislation. Standard home insurance does not include the property owners' liability coverage that protects landlords against injury claims from tenants.

Loss of rental income: If the property becomes uninhabitable following an insured event, standard home insurance covers reinstatement but not the rental income lost during the period of repairs. A landlord without loss of rent cover has uninsured income exposure that can last months.

What Landlord Insurance Covers — the Full Breakdown

Buildings Cover

The core element of all landlord insurance policies. Covers the structure of the property against the standard perils — fire, storm, flood, escape of water, subsidence, impact, and malicious damage — as in standard buildings insurance.

The landlord-specific consideration: Rebuild cost must reflect the current reinstatement cost of the property, not its market value. The same average clause risk applies to landlord insurance as to residential buildings insurance. Landlords with multiple properties should review the rebuild cost of each individually — portfolio policies may apply blanket sums that underinsure some properties.

Property Owners' Liability

Covers the landlord against claims from tenants, their visitors, or members of the public who are injured or whose property is damaged as a result of a defect in the property for which the landlord is responsible.

Why this matters: The Landlord and Tenant Act 1985 requires landlords to maintain the structure, exterior, and installations of the property. A tenant who slips on a broken step the landlord was notified about and failed to repair has a valid personal injury claim against the landlord. Without property owners' liability insurance, this claim is entirely uninsured.

Standard coverage limit: £2m–£5m. Given the severity of serious personal injury claims — spinal injury, severe burns, long-term disability — £2m is the practical minimum. Properties with multiple tenants (HMOs) or those in higher-liability settings should carry £5m.

Loss of Rent / Loss of Rental Income

Covers the rental income lost when the property becomes uninhabitable following an insured event. If a fire makes the property unlettable for four months during repairs, loss of rent insurance covers the rental income that would have been received during that period.

The indemnity period: Most loss of rent policies specify a maximum indemnity period — typically 12 or 24 months. Given that serious property damage (structural fire, severe flood damage) can take 12–18 months to reinstate, a 12-month indemnity period may be inadequate. A 24-month period is recommended for most landlord policies.

What it does not cover: Loss of rental income from a void period (tenant having left, property empty between lets) is not a loss of rent claim — that is a commercial risk, not an insured event. Loss of rent covers only income lost because the property is uninhabitable following an insured physical event.

Malicious Damage by Tenants

Standard buildings and contents insurance excludes deliberate damage by residents — on the basis that deliberate acts are not insurable events. Landlord insurance typically includes malicious damage by tenants as a specific covered extension, recognising that this is a real and recurring risk in the rental market.

The practical threshold: Most malicious damage claims by tenants involve damaged fixtures, fittings, and decoration rather than structural damage. Claims up to £5,000–£10,000 are the most common. Policies vary in whether they cover malicious damage without a police report — check the specific evidence requirements before purchasing.

Contents Cover for Landlord's Fixtures and Fittings

Where the landlord provides furniture, white goods, or other contents in a furnished or part-furnished let, the landlord's own contents insurance covers these items. This does not cover the tenant's personal belongings — tenants are responsible for their own contents insurance.

For unfurnished lets, landlord contents cover addresses only the fixtures and fittings provided by the landlord — carpets, curtain rails, and light fittings are the most common items.

Legal Expenses Insurance

Covers the legal costs of pursuing a tenant for unpaid rent, eviction proceedings, and tenancy dispute resolution. Legal expenses cover is available as a standalone add-on and as a bundled element of some comprehensive landlord policies.

What it typically covers: Solicitor costs for pursuing rent arrears, eviction proceedings under Section 8 or Section 21 of the Housing Act, and attendance at court for possession orders. Average legal costs for a defended eviction: £2,000–£5,000.

2026 Landlord Insurance Cost

Landlord insurance premiums are driven by: property type and rebuild cost, location (flood risk, subsidence, crime rate), number of tenants and tenancy type (single let, multi-let, HMO, student), claims history, and the specific coverage elements included.

| Property Type | Buildings Only | Buildings + Liability + Loss of Rent | Comprehensive |

|---|---|---|---|

| 1-bed flat (rebuild £120k) | £135–£210 | £190–£295 | £240–£380 |

| 2-bed flat (rebuild £150k) | £165–£255 | £232–£360 | £295–£455 |

| 2-bed terraced (rebuild £160k) | £170–£265 | £238–£372 | £302–£468 |

| 3-bed semi (rebuild £200k) | £200–£315 | £280–£440 | £355–£555 |

| 3-bed detached (rebuild £230k) | £230–£365 | £322–£510 | £408–£640 |

HMO Insurance — Why It Costs More

Houses in Multiple Occupation — properties let to three or more unrelated tenants sharing facilities — are classified as higher risk by insurers for three reasons:

- Higher claim frequency: More occupants means more potential for accidental damage, escape of water, and malicious damage incidents.

- HMO licensing: Properties requiring an HMO licence (mandatory for properties with five or more tenants in two or more households) must comply with specific fire safety, safety assessment, and amenity standards. Failure to maintain these standards affects both the insurer's risk assessment and the landlord's liability.

- Standard landlord policies exclude HMOs: Most standard landlord policies are written for standard residential lets. An HMO requires a specific HMO insurance product or explicit HMO endorsement on a standard landlord policy.

HMO insurance premiums typically run 40–80% above equivalent standard single-let premiums.

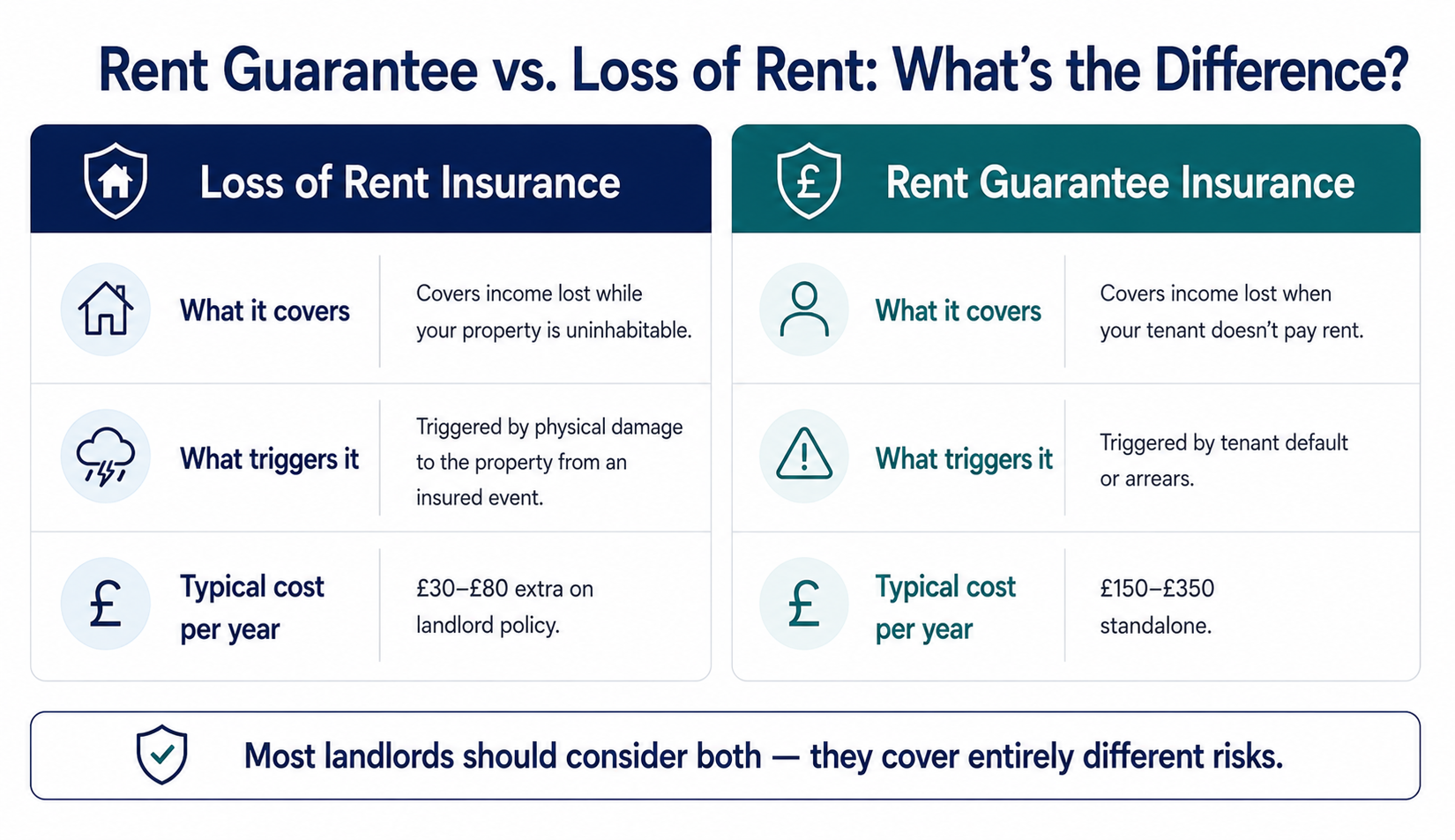

Rent Guarantee Insurance — Protecting Against Non-Payment

Rent guarantee insurance (also called rent protection insurance) is a distinct product from loss of rent insurance. The two cover different risks:

| Product | What It Covers | What Triggers It |

|---|---|---|

| Loss of Rent Insurance | Rental income lost when property is uninhabitable | Physical damage from an insured event |

| Rent Guarantee Insurance | Rental income lost when tenant doesn't pay | Tenant default, rent arrears |

Rent guarantee insurance is typically purchased as a standalone policy or bundled with legal expenses cover. It pays the monthly rent when a tenant defaults, for a defined maximum period (typically 6–12 months) while eviction proceedings take place.

Cost: £150–£350 per year for a standard single-let property.

Referencing requirement: Most rent guarantee policies require the tenant to have been fully referenced (credit check, income verification, previous landlord reference) before the policy will pay a subsequent default claim. Rent guarantee insurance does not cover tenants who were taken on without adequate referencing.

What Landlord Insurance Does Not Cover

Vacant property beyond the unoccupied clause: Most landlord policies specify a maximum unoccupied period — typically 30–60 days. If the property is empty for longer (between tenancies, during renovation, or while the landlord searches for a new tenant), standard coverage is reduced or suspended entirely. Extended unoccupied property insurance provides specific coverage for periods beyond this threshold.

Fair wear and tear: The gradual deterioration of the property and its fixtures over the tenancy period is not an insured event. Worn carpets, faded decoration, and normal use damage are the tenant's fair use of the property — landlords address these through the deposit deduction process, not insurance.

The tenant's belongings: Landlord insurance covers the landlord's property and interests. Tenants' personal possessions are their own responsibility. Landlords should advise tenants to arrange their own contents insurance — some local authority private rented sector schemes require tenants to hold contents cover as a tenancy condition.

Deliberate damage without evidence: Malicious damage claims typically require a police crime reference number and documentary evidence of the damage. Claims for alleged tenant damage discovered after a tenancy has ended — where no police report exists and the cause cannot be verified — are more difficult to substantiate.