High-value home insurance — also called high-net-worth or premier home insurance — is specialist coverage for properties and personal asset portfolios that fall outside the parameters of standard comparison-site home insurance. It typically applies to properties with a rebuild cost above £500,000, contents with a total value above £75,000, or individual items (art, jewellery, wine collections) with values exceeding standard policy limits. Specialist insurers including Hiscox, Chubb, AIG Private Client, and Aviva Private Clients underwrite these risks individually — not through algorithms — which produces meaningfully better coverage and claims service.

High-value home insurance is an individually underwritten residential policy — typically written on an all-risks basis with agreed-value cover for collections — designed for properties with rebuild costs above approximately £500,000 or contents portfolios above £75,000.

Why Standard Home Insurance Fails for High-Value Properties

Standard home insurance is designed for the majority of the residential market — properties with rebuild costs of £100,000–£350,000 and contents of £15,000–£40,000. The products are priced through automated rating engines and have standard coverage structures, single-item limits, and claims processes that are adequate for typical claims.

For high-value properties and personal asset portfolios, these structures create four specific failures:

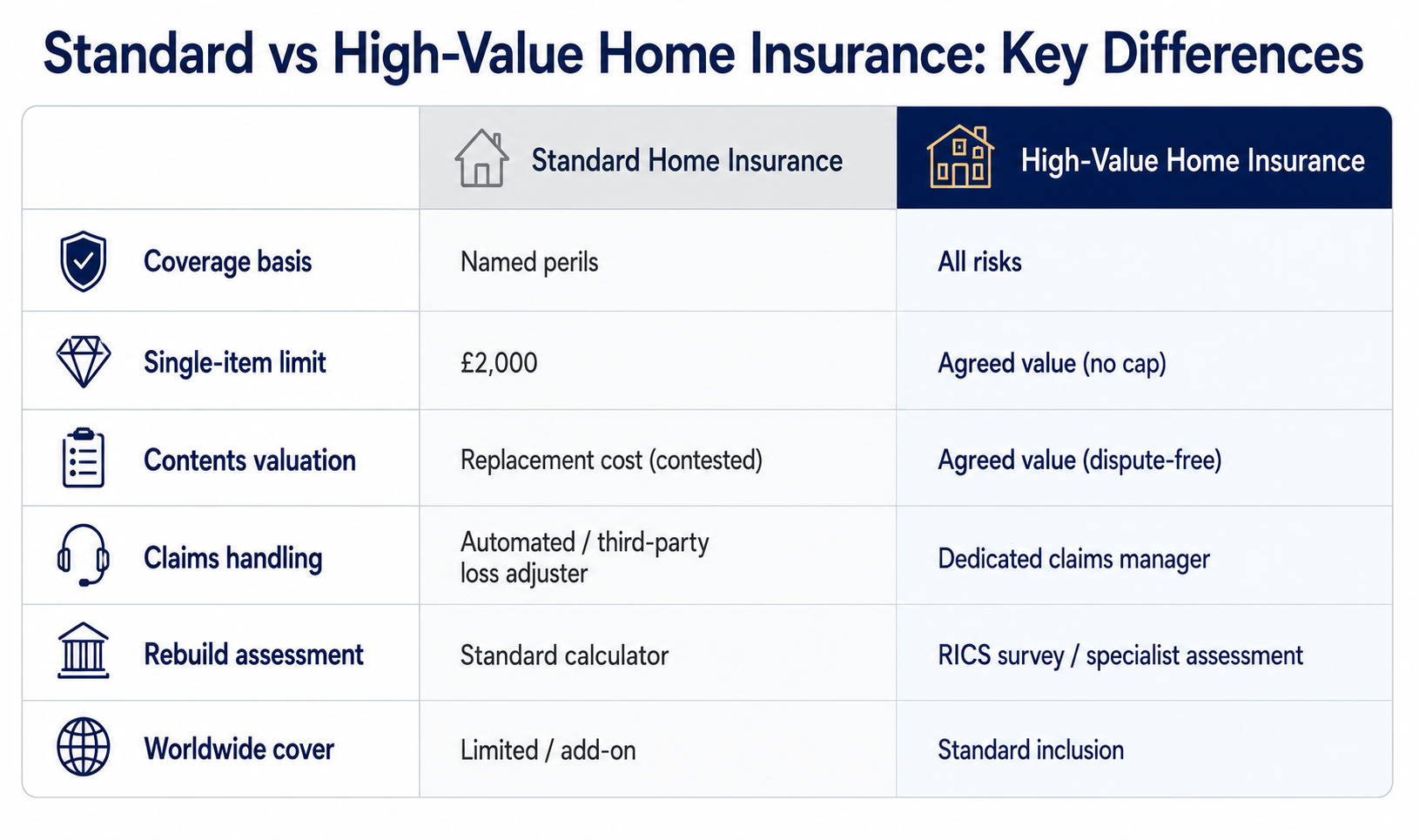

1. Rebuild cost underestimation: Standard policies and automated valuation tools significantly underestimate rebuild costs for period properties, those with specialist architectural features, listed buildings, and homes with premium specifications (limestone floors, bespoke joinery, period plasterwork). A standard tool may calculate £400,000 for a Georgian townhouse that would cost £850,000 to authentically reinstate.

2. Single-item limits: Standard contents policies impose single-item limits of £1,500–£2,500. A high-net-worth household may hold jewellery, art, watches, antiques, and wine collections where individual items routinely exceed this threshold. Without specific declaration, these items are systematically underinsured.

3. Claims handling: Standard insurers manage claims through automated processes and third-party loss adjusters. For a high-value property claim, this produces slow, contentious, and sometimes inadequate settlements. Specialist high-net-worth insurers provide dedicated claims managers who handle the claim from first notification to final settlement — and who have the authority to approve high-value settlements without committee approval.

4. Coverage scope: Standard policies cover named perils. High-value policies are often written on an all-risks basis — all damage is covered unless specifically excluded. This reversal of the coverage logic provides materially broader protection.

Who High-Value Home Insurance Is Designed For

Properties: Any residential property where the rebuild cost exceeds approximately £500,000. This includes Georgian and Victorian period homes, listed buildings, architect-designed contemporary properties, properties with specialist construction or features, and rural estates.

Contents portfolios: Households where the total contents value exceeds £75,000–£100,000, or where individual items of significant value are held — jewellery collections, art collections, antique furniture, vintage wine cellars, high-specification audio-visual equipment, classic motor vehicles.

Lifestyle requirements: Individuals whose coverage needs extend beyond a single primary residence — including second homes in the UK and abroad, portable valuables taken internationally, and personal liability coverage on a worldwide basis.

How High-Value Home Insurance Differs From Standard Cover

All-Risks vs Named Perils

Standard policies cover named perils only — specific events listed in the policy document (fire, flood, theft, escape of water). Anything not named is excluded by default.

High-value policies are typically written on an all-risks basis — all accidental loss or damage is covered unless specifically excluded. The coverage logic is reversed: instead of listing what is covered, the policy lists what is not. This provides significantly broader protection, particularly for accidental damage and unusual loss scenarios.

The practical difference: A standard policy holder who accidentally drops a valuable sculpture, breaking it, has an accidental damage claim. If they did not purchase the accidental damage extension, it is not covered. An all-risks high-value policy holder who drops the same sculpture has a covered claim without any extension needed.

Agreed Value for Contents and Collections

Standard contents policies settle claims at replacement value for standard items and at single-item limits for declared items. High-value policies can be written on an agreed value basis for specific high-value items — art, jewellery, antiques, wine — where both the policyholder and insurer agree the insured value at inception, based on a professional appraisal. In a total loss claim, the agreed value is paid without dispute.

This eliminates the most common source of high-value claim disputes: the insurer's contention that the actual replacement value differs from the claimed amount.

Worldwide Personal Possessions

Standard personal possessions extensions cover items away from home but typically have geographical restrictions (UK and Europe, for example) and annual limits of £2,500–£10,000.

High-value policies provide worldwide personal possessions coverage — jewellery, watches, portable art, and high-specification electronics covered anywhere in the world, for travel duration up to the policy maximum (typically 180 days per trip). Coverage limits match the agreed or declared value of the specific item rather than a general category cap.

The High-Value Home Insurance Market — the Main Specialist Providers

High-value home insurance is not available through standard price comparison websites. These products are placed through specialist brokers with access to the private client insurance market. The main UK underwriters:

Hiscox Private Clients: One of the best-known high-net-worth home insurers in the UK. All-risks basis, agreed value for collections, dedicated claims service, and coverage for international properties. Known for straightforward claims settlement and minimal dispute. Accesses both Lloyd's and their own balance sheet.

Chubb Masterpiece: The global benchmark for high-net-worth insurance. Extended replacement cost guarantee (covers rebuild costs above the sum insured if they increase during reinstatement), guaranteed replacement for listed buildings, worldwide personal articles coverage, family protection (personal liability worldwide). Claims handled by Chubb's own adjusters with authority to settle without committee approval.

AIG Private Client: Comprehensive high-value home coverage with strong art and collections expertise. AIG has a specialist fine art and valuable articles team. Worldwide coverage with strong presence for international property portfolios.

Aviva Private Clients: Standard insurer with a dedicated private clients division offering enhanced coverage terms. More accessible price point than Hiscox or Chubb for properties at the lower end of the high-value threshold.

Covea Insurance Private Clients: Underwriters for several major private client brokers. Competitive for rural properties, country houses, and estates.

Insuring Specific High-Value Asset Categories

Art and Antiques

Art insurance — the specific coverage of paintings, sculpture, and other works of art — is the most specialist category within high-value home insurance.

The valuation requirement: Fine art must be professionally appraised to establish insured value. Appraisals should be conducted by RICS-registered or RICS-affiliated valuers for furniture and antiques, and by specialist auction house appraisers or professional art valuers (BVAA-registered) for paintings and sculpture. Appraisals should be updated every three to five years — art values fluctuate significantly.

Agreed value is essential: Art settled at replacement value creates a dispute-prone claims process. High-value art must be insured on an agreed value basis — the appraisal forms the basis of the insured value, and a total loss claim is settled at that figure.

Climate and storage conditions: Some specialist art insurers provide coverage for damage caused by climate failure — an air-conditioning breakdown that damages a collection, or humidity damage during transport. This is not available in standard policies and is one of the most valuable specialist art coverage elements.

Jewellery and Watches

Jewellery is the most frequently claimed category in high-value home insurance.

Professional valuation: All items above £2,000 in value should have a current professional appraisal from a NAJ (National Association of Jewellers) registered valuer. Appraisals lose currency over time — diamond and precious metal prices have increased significantly since 2020, and a 2019 appraisal may understate the 2026 replacement cost.

Worldwide coverage: Jewellery worn while travelling internationally is at highest risk. Standard personal possessions policies may restrict coverage to the UK and Europe. High-value policies should provide worldwide coverage for jewellery without geographical restriction.

Bank vault credit: Some policies provide a premium reduction if high-value jewellery is stored in a bank-approved safe deposit facility when not in use.

Wine Collections

Wine collection insurance is a specialist sub-category with specific risk characteristics: temperature and humidity risk (cellar temperature failure damages the collection); label damage (a collection is typically valued as a complete unit — damaged labels reduce trading value even without damage to the wine); and trading value vs replacement value (a mature wine collection cannot be replaced like-for-like — the insurance should reflect the current market value of the collection, updated annually).

Specialist wine insurers include Willis Towers Watson and a small number of Lloyd's syndicates with fine wine expertise.

2026 High-Value Home Insurance Indicative Premiums

Unlike standard home insurance, high-value policies are individually underwritten. Premiums are not rate-calculated from tables — they are assessed based on the specific property survey, contents appraisal, security, and claims history. The following are illustrative ranges only:

| Scenario | Indicative Annual Premium |

|---|---|

| Georgian townhouse, rebuild £600k, contents £120k (art and jewellery declared) | £3,500–£6,500 |

| Country house, rebuild £1.2m, contents £250k, 10 acres | £6,500–£12,000 |

| London penthouse, rebuild £800k, contents £200k (jewellery and electronics) | £4,500–£8,500 |

| Listed farmhouse, rebuild £900k, contents £180k | £5,000–£10,000 |

| Portfolio: primary + secondary home, combined rebuild £1.5m | £8,000–£18,000 |