Contents insurance covers the belongings inside your home — furniture, clothing, electronics, jewellery, and kitchen appliances — against theft, fire, flood, and accidental damage (if the accidental damage extension is included). The average UK household underestimates its contents by 40%, insuring at £15,000–£20,000 when the true replacement value is £35,000–£50,000. The most consequential policy decisions are: setting the sum insured accurately, checking the single-item limit, and deciding whether a personal possessions extension is needed for items taken outside the home.

Contents insurance is a UK residential policy that covers moveable belongings inside your home — everything you would take with you if you moved — against named perils such as fire, flood, theft, and (optionally) accidental damage, settled on either a new-for-old or indemnity basis.

What Contents Insurance Covers — and the Boundary With Buildings

Contents insurance covers everything in your home that is not permanently fixed to the structure. The practical test: if you were moving house, contents are everything you would take with you. Buildings are everything you would leave behind.

What contents insurance covers

- Furniture: sofas, beds, wardrobes, dining tables, office furniture

- Soft furnishings: curtains, rugs (not fixed carpets — see buildings boundary)

- Clothing and personal items: all clothing, shoes, bags, jewellery (up to single-item limits)

- Electronics: TVs, laptops, desktop computers, gaming consoles, tablets, smartphones

- Kitchen appliances not permanently built-in: freestanding dishwasher, microwave, kettle

- Garden contents: garden furniture, barbecue, tools, lawnmower (check outdoor limits)

- Business equipment at home: up to defined limits — check if separate business cover is needed

- Money and credit cards: up to sub-limits typically £500–£1,000 in cash

The perils covered by a standard contents policy

- Fire, smoke, and explosion

- Theft and attempted theft

- Flood and storm damage

- Escape of water from plumbing (damage to contents caused by flooding)

- Malicious damage

- Impact from vehicles or falling objects

What standard contents insurance does not cover

- Accidental damage (unless the extension is purchased)

- Items taken outside the home (requires personal possessions extension)

- Wear and tear, mechanical or electrical breakdown

- Items in unoccupied property beyond the policy's unoccupied period (typically 30–60 days)

- Business stock or trade equipment above the policy's business limit

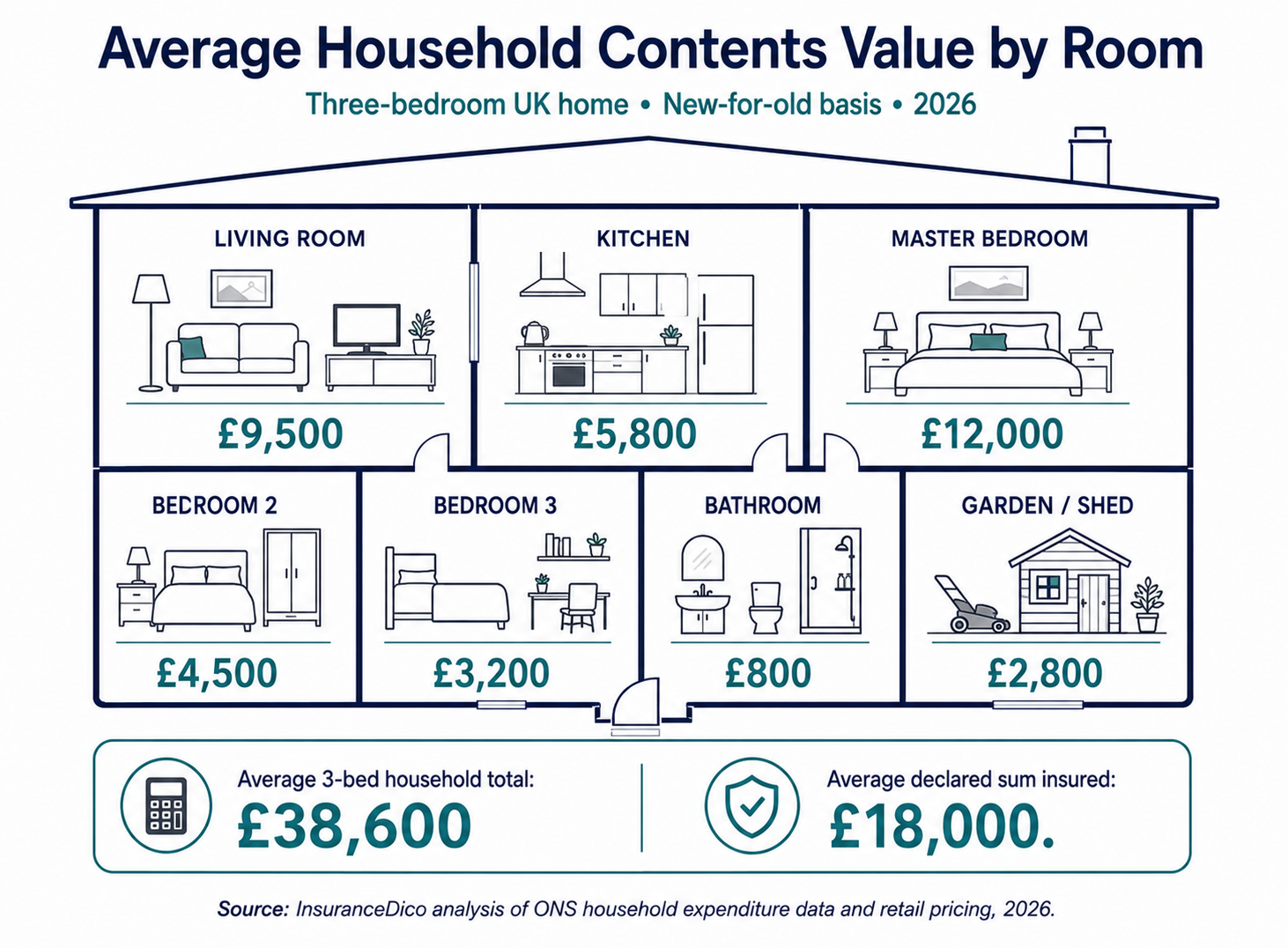

The Underinsurance Problem — Why 40% Is the Wrong Number

Research consistently shows that the average UK household underestimates the value of its contents by approximately 40%. The Building Societies Association found the average household insures at £15,000–£20,000 when the replacement cost on a new-for-old basis is typically £35,000–£55,000 for a three-bedroom family home.

The categories most commonly undervalued

Clothing: Most people estimate their wardrobe at £2,000–£4,000. The new-for-old replacement cost — buying equivalent items at today's retail prices — is typically £8,000–£18,000 for an adult wardrobe including footwear, outerwear, and accessories.

Technology: A household with two adults and two children may hold £9,000–£15,000 in electronics: two smartphones (£800–£1,200 each), two laptops (£600–£1,500 each), a gaming console (£400–£550), smart TV (£400–£1,200), tablets (£200–£600 each), and associated accessories.

Jewellery: Engagement rings, watches, inherited pieces, and accumulated gifts over years are frequently omitted entirely or significantly undervalued. A modest but quality engagement ring at £3,000–£5,000 alone exceeds many people's entire declared jewellery value.

Garden contents: Often omitted entirely. A lawnmower (£150–£800), power tools (£200–£600), garden furniture set (£300–£1,500), and shed contents collectively represent £1,000–£4,000 of replaceable value.

Kitchen appliances: The kitchen contents of a modern household — all freestanding appliances, cookware, food processor, coffee machine, and utensils — typically total £3,000–£8,000 at new-for-old replacement prices.

New for Old vs Indemnity — the Most Consequential Policy Choice

New for old cover replaces damaged or stolen items with brand new equivalents at today's retail prices, regardless of the age or condition of the original item. A five-year-old laptop is replaced with an equivalent current model. A fifteen-year-old sofa is replaced with a comparable new sofa at current prices.

Indemnity cover reduces the claim settlement to account for the age, wear, and depreciation of the original item. A five-year-old laptop that cost £900 new might be settled at £200–£350 under an indemnity basis — reflecting its second-hand value rather than replacement cost.

The practical difference in a claim

A house fire destroys a three-year-old 65" television (original cost £800, current equivalent: £750), a two-year-old washing machine (original cost £500, current equivalent: £480), and a seven-year-old sofa (original cost £1,200, current equivalent new: £1,100).

- New for old settlement: £750 + £480 + £1,100 = £2,330

- Indemnity settlement: £520 + £320 + £250 = £1,090 (approximate depreciated values)

The difference is £1,240 on a relatively modest claim. On a comprehensive contents claim after a serious fire or flood, the difference can run to thousands.

New for old is standard on most mid-tier and above policies. Budget policies at the lower end of the market may use an indemnity basis without making this prominent in their marketing. Confirm the basis before purchasing — the summary documents use the terms "new for old" or "replacement as new" for the better product and "indemnity" or "like for like allowing for depreciation" for the weaker one.

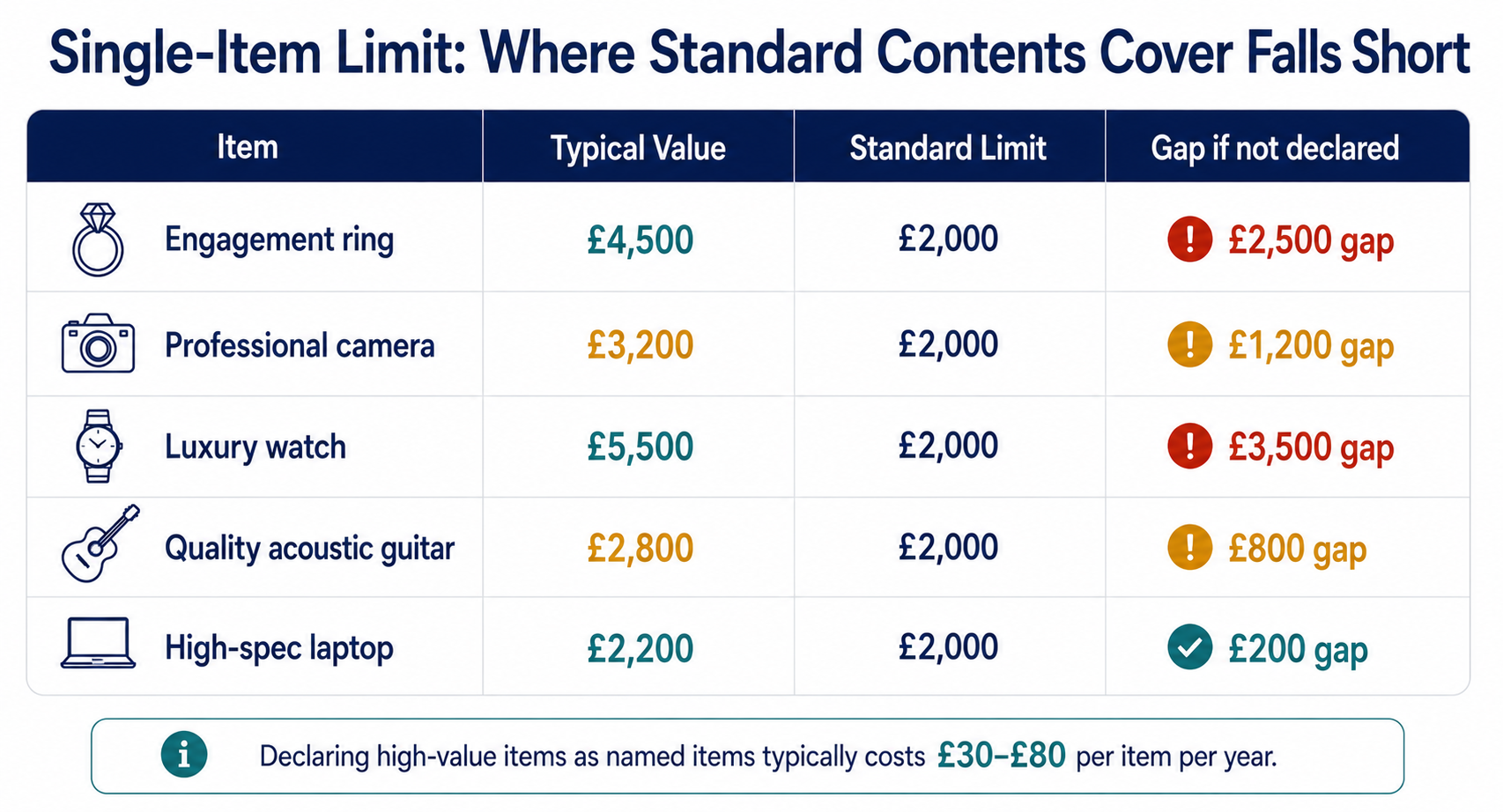

Single-Item Limits — the Coverage Gap That Affects High-Value Possessions

Standard contents insurance policies impose a single-item limit — the maximum payable for any individual item without specific declaration. This is one of the most significant and underappreciated limitations in standard contents coverage.

Typical single-item limits range from £1,500 to £2,500 depending on the insurer and policy tier. Items worth more than this limit are underinsured unless they are specifically declared on the policy as named items, or a valuables extension with a higher limit is added.

| Item | Typical Value | Standard Single-Item Limit | Gap |

|---|---|---|---|

| Quality engagement ring | £3,500–£8,000 | £2,000 | £1,500–£6,000 |

| Professional camera with lenses | £2,500–£6,000 | £2,000 | £500–£4,000 |

| High-end laptop | £1,800–£3,500 | £2,000 | Up to £1,500 |

| Luxury watch | £3,000–£15,000+ | £2,000 | £1,000–£13,000+ |

| Artwork | Varies widely | £2,000 | Variable |

| Musical instrument (quality) | £2,000–£10,000+ | £2,000 | Up to £8,000+ |

Most insurers allow specific named items to be added to the policy at a small additional premium. A £5,000 engagement ring declared as a named item is typically insured for an additional £30–£80 per year. Without this declaration, a claim for the full ring value would be capped at the standard single-item limit.

Personal Possessions Extension — Covering Items Away From Home

Standard contents insurance covers your belongings inside the insured property only. The moment an item leaves the front door — a phone taken to work, a laptop carried on a train, jewellery worn to an event, a bicycle ridden to the shops — it is no longer covered by your standard contents policy.

A personal possessions (or "all-risks") extension covers specified categories of items anywhere in the UK (and optionally worldwide). This extension typically adds £20–£50 per year to the premium for cover up to the specified limit.

What personal possessions covers

- Mobile phones (theft, accidental damage, loss — check whether loss is included or only theft and accidental damage)

- Laptops and tablets carried outside the home

- Jewellery and watches worn away from home

- Cameras and equipment taken on shoots

- Bicycles (check: some policies require a separate bicycle extension at a defined value)

What personal possessions typically does not cover

- Items left unattended in a vehicle (a very common exclusion — a phone or laptop left in a parked car is typically not covered regardless of whether the car was locked)

- Items forgotten and not actively stolen (loss without evidence of theft or accidental damage is frequently excluded)

2026 Contents Insurance Premium Data

| Property Type | Sum Insured | Annual Premium (Excl. Accidental Damage) | With Accidental Damage |

|---|---|---|---|

| 1-bed flat | £15,000–£25,000 | £60–£110 | £80–£145 |

| 2-bed terraced | £20,000–£35,000 | £80–£145 | £108–£195 |

| 3-bed semi | £30,000–£50,000 | £105–£185 | £142–£250 |

| 3-bed detached | £35,000–£60,000 | £120–£215 | £162–£290 |

| 4-bed detached | £45,000–£80,000 | £145–£265 | £196–£358 |

What Significantly Affects Your Contents Premium

Sum insured: The most direct lever. Insuring at accurate replacement value costs more than underinsuring — but paying a lower premium for inadequate coverage is not a saving.

Postcode: High-theft postcodes (urban centres, areas near transport hubs) attract higher contents premiums. The impact of postcode on contents premiums is larger than its impact on buildings premiums, reflecting the theft risk component.

Security features: An alarm to EN50131 standard, window locks on all accessible windows, and deadbolts on external doors reduce premiums by 5–15%.

Claims history: A theft or accidental damage claim in the past five years typically produces a 20–40% loading for three to five years.