Buildings insurance covers the physical structure of your home against fire, storm, flood, escape of water, subsidence, and other specified perils. Mortgage lenders require it as a condition of any home loan. The average UK buildings insurance premium is £175–£230 per year for a standard three-bedroom semi-detached. The most significant risk most homeowners face is underinsurance — insuring the property at its market value rather than its rebuild cost. These figures differ substantially, and insuring at the wrong figure reduces every claim proportionally.

What Buildings Insurance Covers — the Definitive List

Buildings insurance covers the structure of the property and anything permanently fixed to it. This boundary determines whether a claim falls to buildings or contents insurance, and getting it right prevents coverage gaps.

What buildings insurance covers

The physical structure: External walls, internal load-bearing walls, roof structure and covering, floors and ceilings, foundations, chimney stacks.

Permanent fixtures and fittings: Fitted kitchens (units, worktops, built-in appliances), fitted bathrooms (bath, shower enclosure, WC, washbasin, fitted storage), built-in wardrobes, fixed flooring (tiles, carpets fixed to the floor with gripper rods), fireplace surrounds, and fitted bedroom furniture.

Domestic installations: Plumbing pipes and drainage within the property, electrical wiring and consumer unit, central heating system (boiler, radiators, pipework), solar panels and heat pumps permanently installed.

Outbuildings: Garages, garden sheds, greenhouses, boundary walls, gates, and fences. Check policy limits — some policies cap outbuilding coverage at 10% of the buildings sum insured.

The covered perils — what events trigger a claim

- Fire, explosion, smoke, and lightning strike

- Storm and flood damage

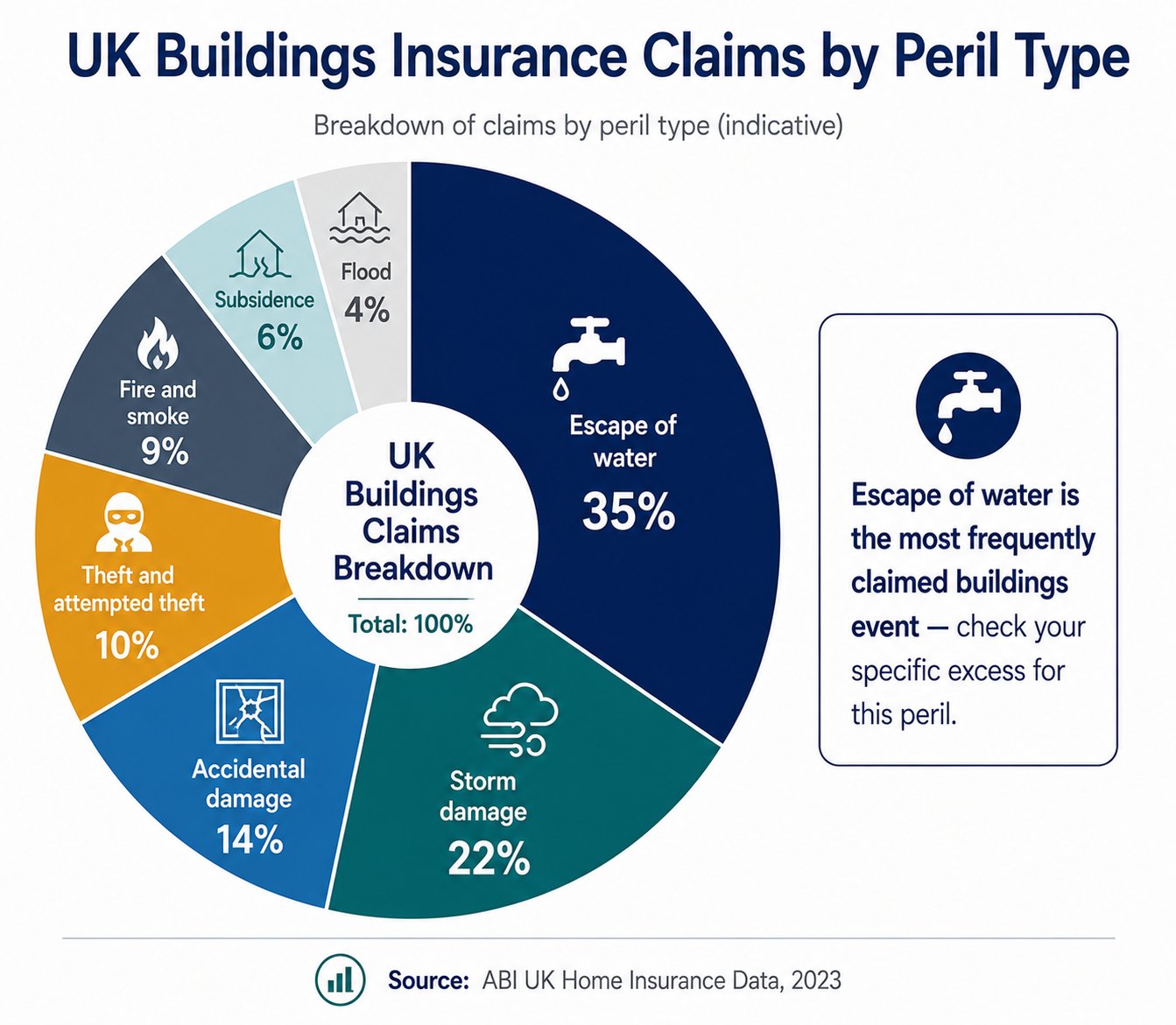

- Escape of water from fixed plumbing, tanks, or appliances — the most frequently claimed buildings event in the UK

- Subsidence, heave, and landslip

- Theft and malicious damage

- Impact from vehicles, falling trees, or aircraft

- Riot and civil commotion

- Oil leaks from central heating systems

What buildings insurance does not cover

Wear and tear, gradual deterioration, and maintenance failures are the most commonly cited reasons for claim rejection. A roof that fails after 40 years of service is a maintenance failure, not an insurable event. Rising damp, dry rot, and wet rot developing gradually are maintenance issues, not sudden events — they are excluded by all standard buildings policies.

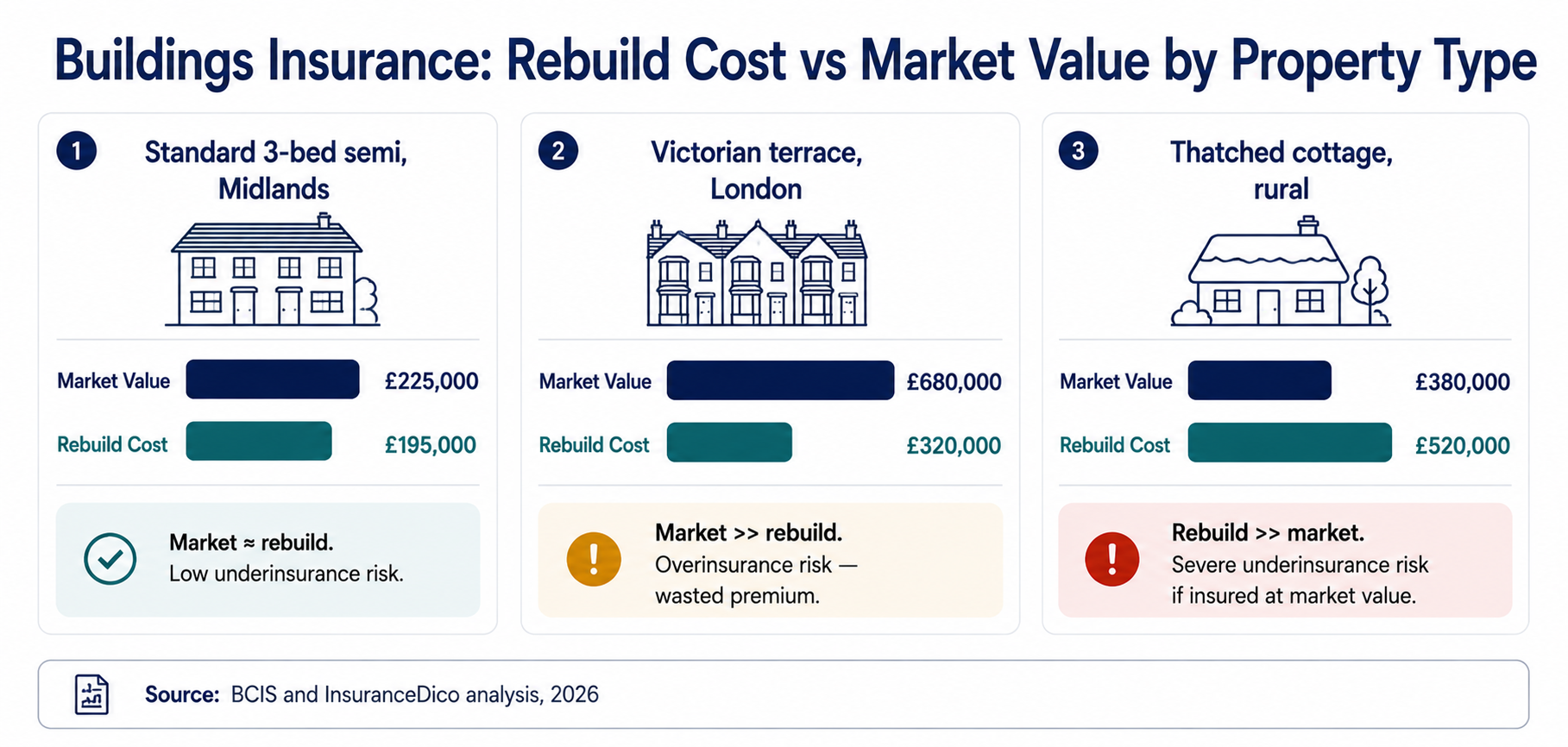

The Rebuild Cost vs Market Value Problem — Why Getting This Right Matters

This is the single most consequential variable in buildings insurance and the one most commonly set incorrectly.

Market value is what the property would sell for today. It includes the land value, the location premium, and current housing market conditions.

Rebuild cost is what it would cost to demolish the existing structure and rebuild it from scratch on the same site — including demolition, site clearance, labour, materials, professional fees, and compliance with current Building Regulations. It does not include land value.

Why these figures differ — and in both directions

For a detached property in a high-demand location (London, Surrey, Berkshire), the market value typically far exceeds the rebuild cost. A London townhouse worth £950,000 on the market may cost £480,000–£650,000 to rebuild. Insuring at market value appears to provide generous coverage but wastes premium on £300,000–£470,000 of land value that is never at risk.

For a property with specialist construction (timber frame, stone walls, thatched roof) or period features (Victorian cornicing, sash windows, original parquet flooring), the rebuild cost often exceeds what a buyer would pay — because authentic period reinstatement costs significantly more than modern construction.

For a flat in a purpose-built block, the leaseholder's buildings insurance responsibility is typically for the internal structure only — or there is no buildings insurance obligation at all, because the freeholder insures the whole block.

The average clause and its consequences

If your buildings insurance sum insured is below the true rebuild cost, insurers apply the average clause at any claim. This proportionally reduces the claim settlement:

“Settlement = (Sum Insured ÷ True Rebuild Cost) × Claim Value”

A property with a true rebuild cost of £280,000 insured at £200,000 (71.4%) suffers a £40,000 escape of water claim. The settlement is: (£200,000 ÷ £280,000) × £40,000 = £28,571. The policyholder receives £28,571 and funds the remaining £11,429 personally.

How to establish the correct rebuild cost

The BCIS (Building Cost Information Service), operated by RICS, publishes a free rebuild cost calculator for standard residential properties. Input the floor area, construction type, and location to generate a current rebuild cost estimate. This takes approximately five minutes and should be done before arranging buildings insurance and at every subsequent renewal.

For properties with non-standard construction (timber frame, stone or flint walls, thatched roof, steel frame, pre-cast reinforced concrete), or listed buildings, a professional rebuild cost survey by a RICS-accredited chartered surveyor is the appropriate approach. Standard calculators significantly underestimate rebuild costs for atypical constructions.

2026 Buildings Insurance Premiums — What You Should Expect to Pay

Buildings insurance premiums are driven by: the rebuild cost (sum insured), property type and construction, location (postcode, flood zone, subsidence risk, local crime), claims history at the address (insurers check CUE), and the policy excess.

| Property Type | Average Annual Premium | Sum Insured Range |

|---|---|---|

| 2-bed terraced | £125–£185 | £120,000–£180,000 |

| 3-bed semi-detached | £155–£230 | £160,000–£240,000 |

| 3-bed detached | £185–£275 | £190,000–£280,000 |

| 4-bed detached | £220–£330 | £230,000–£350,000 |

| Purpose-built flat (leaseholder) | £60–£110 | Freeholder arranges buildings — interior only if applicable |

| Converted flat (Victorian house) | £95–£165 | £80,000–£140,000 interior structure |

| Listed building (Grade II) | £280–£650+ | Specialist assessment required |

| Thatched property | £380–£850+ | Specialist insurer required |

The factors that significantly increase premiums

Flood zone location: Properties in Environment Agency high flood-risk zones attract significant loading. Flood Re — the government-backed reinsurance scheme — makes cover available for most residential properties built before January 2009 at capped rates. For properties built after 2009 or in exceptional risk zones, flood insurance may require specialist placement.

Subsidence history: A property with subsidence in its claims history is more expensive to insure — subsidence is a recurring risk once present in a particular soil type. Properties on shrinkable clay soils in London and the South-East face higher base rates.

Non-standard construction: Timber frame, prefabricated concrete (PRC), steel frame, and properties with unusual roofing materials attract loadings or require specialist insurers.

Claims history at the address: The Claims and Underwriting Exchange (CUE) records claims by property address, not only by the current owner. A property with a serious flood or fire claim in the past five years may face higher premiums for a new owner who was not involved in the original claim.

The Most Important Buildings Insurance Policy Terms to Check

The escape of water excess: Many policies apply a higher specific excess for escape of water claims — the most frequently claimed buildings event. A standard excess of £250 may rise to £500 or £1,000 for escape of water claims. This is disclosed in the policy schedule, not the summary. Check before purchasing.

The trace and access clause: When an escape of water occurs within a wall, floor, or ceiling, finding the source requires cutting through the structure. The trace and access clause covers the cost of this investigation — the cutting, making good, and decorating around the repair point. Some budget policies cap this at £2,500; comprehensive policies provide unlimited trace and access. On a serious leak in a party wall, trace and access costs can exceed £10,000.

The matching clause: If one section of a floor, wall, or roof covering is damaged and the undamaged sections are discontinued patterns, the matching clause determines whether the insurer replaces the undamaged sections to create a uniform appearance. Some policies offer matching; others replace only the damaged section.

The subsidence excess: Subsidence claims carry a specific elevated excess — typically £1,000 — separate from the standard policy excess. This is standard across most UK buildings policies and cannot be waived.

Flood Risk and the Flood Re Scheme — What Homeowners Need to Know

Approximately 5.2 million properties in England are in a flood risk zone according to the Environment Agency. For properties with a history of flooding or in zones with high flood probability, standard insurers historically declined to insure or applied prohibitive premiums.

Flood Re is the government-backed reinsurance scheme established in 2016 to make flood insurance available and affordable for high-risk residential properties. Insurers can cede the flood element of a residential policy to the Flood Re pool at a price capped by council tax band.

Flood Re eligibility

- Residential properties built before 1 January 2009

- Properties in England, Scotland, Wales, and Northern Ireland

- Properties with council tax banding

Not eligible for Flood Re

- Properties built after 1 January 2009 (expected to meet modern flood resilience standards)

- Commercial properties

- Properties with three or more flood claims in ten years (insurer discretion)

What Flood Re does not guarantee: Flood Re caps the reinsurance rate that insurers pay — it does not cap the retail premium charged to policyholders. Insurers add their own margin to the Flood Re ceded cost. Policyholders in high-risk zones should compare multiple insurers and consider BIBA-referred specialist flood brokers to find the most competitive retail price.

The 2039 sunset clause: Flood Re is designed to run until 2039, after which flood-risk properties will return to open market pricing. This has significant long-term implications for property values in high-flood-risk areas and for the insurance costs that future owners will face.