International health insurance provides private medical coverage outside your home country — for expats living abroad, employees on international assignments, remote workers, and frequent long-stay travellers. It is distinct from travel insurance (which covers short-term trips) and from UK private medical insurance (which covers treatment in the UK only). Annual premiums range from £1,200 to £4,500 for a comprehensive individual plan depending on age, coverage zone, and benefit level. US coverage adds approximately 30–50% to global premiums due to the US healthcare cost structure.

International health insurance is an annual private medical policy that covers inpatient, outpatient and specialist healthcare in your country of residence and across a defined global coverage zone, designed for long-term overseas living rather than short trips.

International Health Insurance vs Travel Insurance — the Distinction

The confusion between international health insurance and travel insurance is the most common error in this market. The two products serve fundamentally different needs and should not be substituted for each other.

| Dimension | International Health Insurance | Travel Insurance |

|---|---|---|

| Duration | Annual, ongoing — designed for long-term overseas residency | Per trip — typically days to 8 weeks |

| Coverage scope | Comprehensive: inpatient, outpatient, specialist, maternity, chronic conditions | Emergency medical only — acute events, not ongoing care |

| Chronic conditions | Covered (subject to underwriting) after policy start | Excluded — travel insurance never covers pre-existing chronic conditions |

| Outpatient care | Included in most plans | Not covered — travel insurance is emergency only |

| Intended user | Expats, assignees, long-stay remote workers | Short-term travellers, holiday-makers |

| UK coverage | Usually excludable or optional | N/A — designed for travel away from home |

| Annual premium | £1,200–£4,500+ | £25–£200 per trip |

The consequence of using travel insurance instead of international health: A British expat in Dubai who maintains travel insurance rather than international health insurance has emergency medical coverage that will trigger for an acute event — a broken bone, acute appendicitis. They do not have coverage for outpatient consultations, ongoing medication for managed conditions, preventive care, or any condition requiring more than short-term emergency treatment. In most countries outside the UK, long-term healthcare without insurance generates costs that are not manageable as self-pay expenses.

Who Needs International Health Insurance

British expats living abroad: UK nationals who relocate to another country lose access to NHS care as their primary healthcare system. The NHS treats non-residents as overseas visitors — charges apply for treatment. International health insurance provides a comprehensive healthcare safety net in the country of residence.

Company assignees on international postings: Employers sending employees on extended international assignments have a duty of care obligation to ensure adequate healthcare access. Most reputable employers provide international health insurance as a standard component of an expatriate package. Employees on assignment should verify coverage scope — some corporate plans have limitations that individual international policies do not.

Remote workers and digital nomads: The growth of location-independent working has created a large cohort of individuals working from countries where they are not resident for tax purposes and may not be entitled to state healthcare. International health insurance designed for remote workers provides flexible coverage across multiple countries.

Frequent long-stay travellers: Individuals spending more than 3 months per year outside the UK across multiple destinations may find international health insurance more appropriate and cost-effective than annual travel insurance — particularly if they have managed health conditions that travel insurance excludes.

How International Health Insurance Works — Structure and Coverage

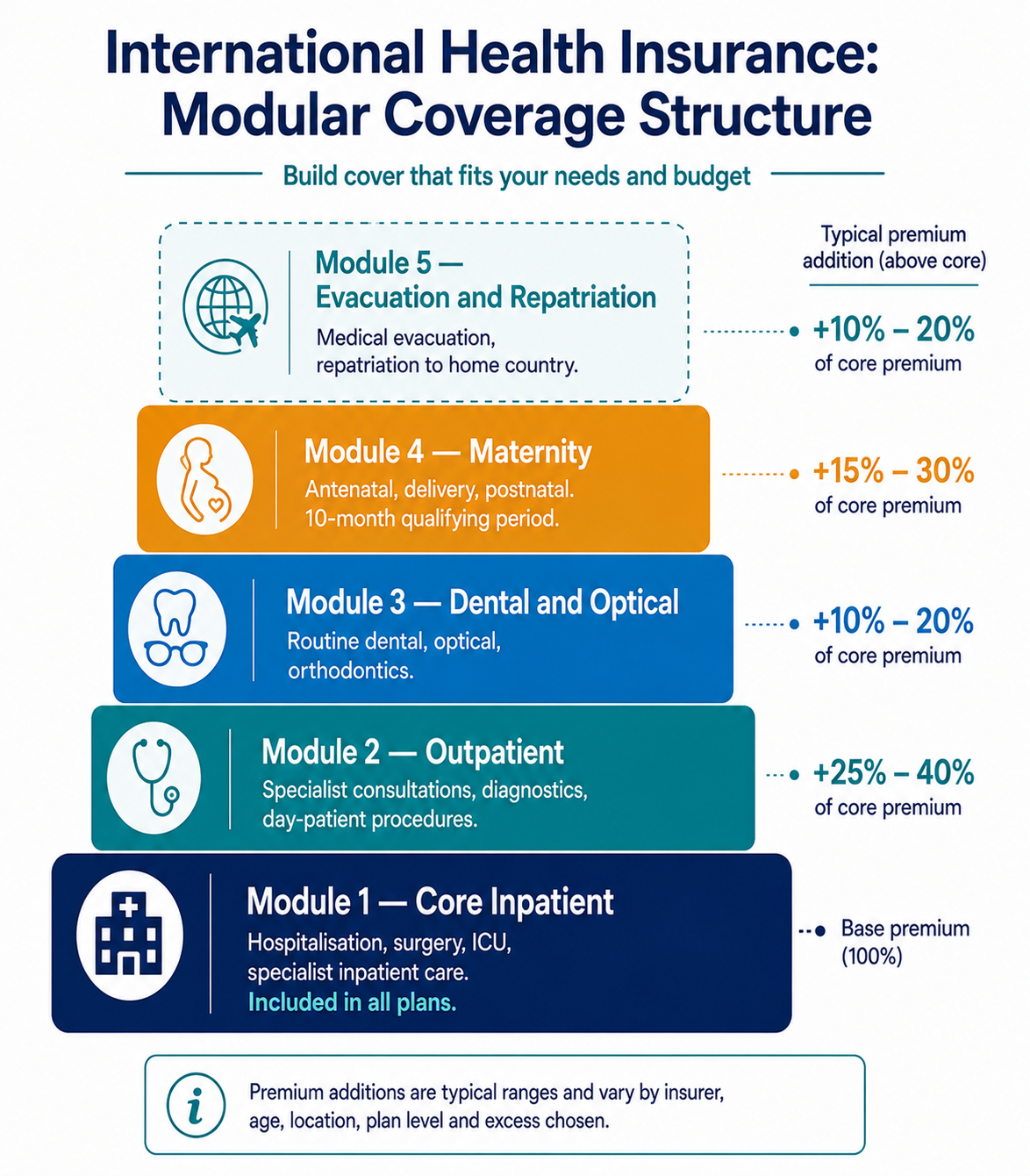

The Modular Coverage Architecture

Most international health insurance plans use a modular structure. Core coverage — inpatient hospitalisation — is the foundation. Additional modules are added depending on budget and need:

Module 1 — Core Inpatient (all plans): Covers hospitalisation for surgical and medical inpatient treatment. Includes accommodation, theatre fees, surgeon and anaesthetist fees, intensive care, and specialist inpatient consultations. Annual limits range from £250,000 to unlimited, depending on the plan.

Module 2 — Outpatient (most standard and comprehensive plans): Specialist consultations, diagnostic tests (MRI, CT, blood panels), and outpatient procedures without hospitalisation. Annual limits are typically £5,000–£25,000 depending on the plan tier. Without outpatient coverage, you must self-fund all consultations and diagnostics — in many countries, these costs accumulate rapidly.

Module 3 — Dental and Optical (optional, added to core or outpatient): Covers dental treatment and optical costs at defined annual limits. Dental and optical modules are typically not included in core plans and add £200–£600 per year to premiums. Cosmetic dental procedures are excluded.

Module 4 — Maternity (optional, strict qualifying period): Covers antenatal care, delivery, and postnatal care. Maternity coverage typically requires a 10–12 month qualifying period before any maternity claims are paid — this prevents policy-taking specifically due to a known pregnancy. The qualifying period applies even for planned pregnancies.

Module 5 — Evacuation and Repatriation (standard on most plans): Medical evacuation to the nearest appropriate medical facility and repatriation to your home country if medically necessary. This is one of the most valuable components of international health insurance in locations with limited local medical facilities.

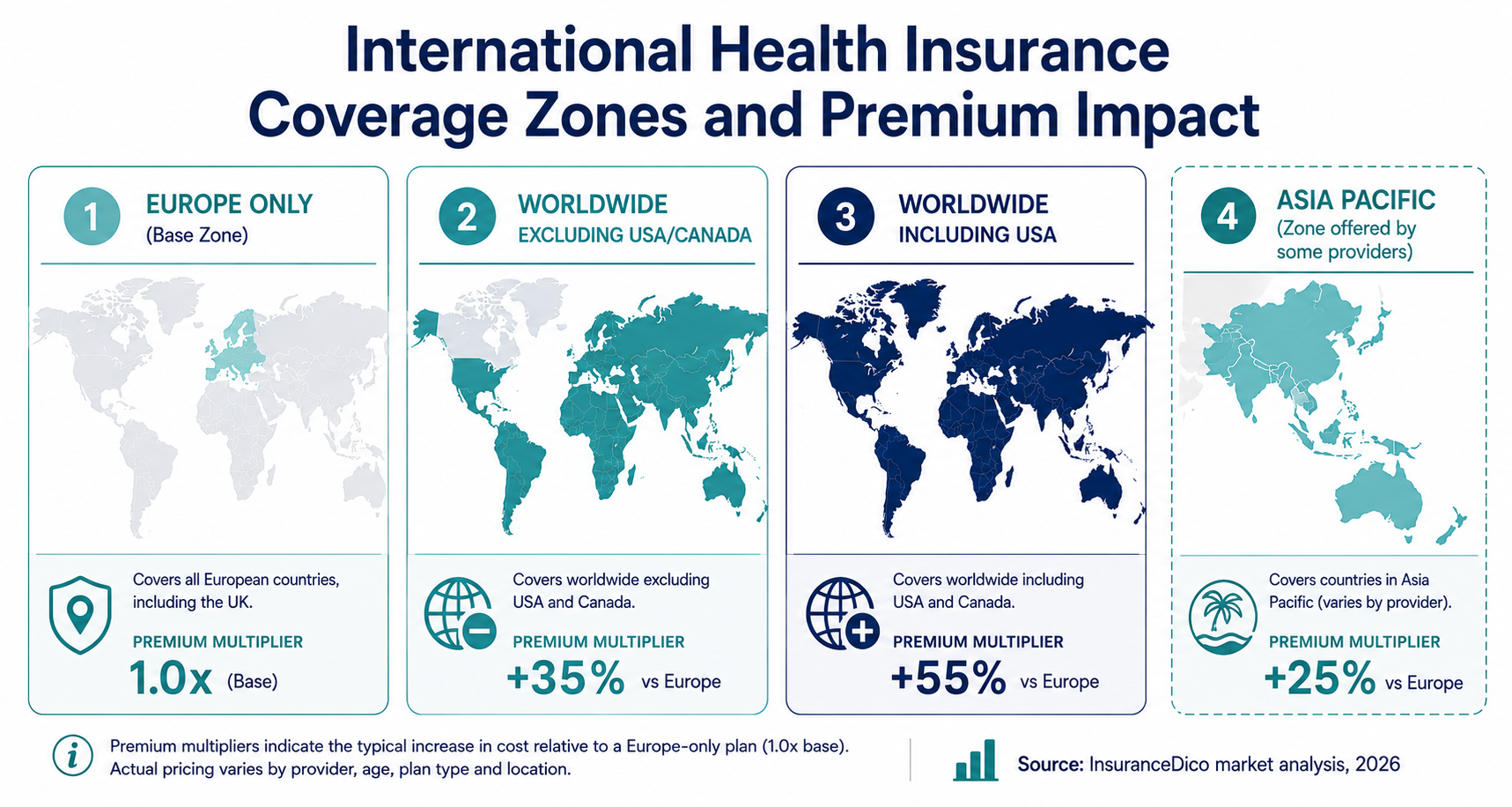

Coverage Zones and Their Premium Impact

International health insurance premiums are heavily influenced by the geographic coverage zone selected. The US healthcare market is the primary cost driver — medical costs in the United States are among the highest in the world and directly inflate global plan premiums for those who require US coverage.

Europe only: Covers treatment in European countries. Most cost-effective zone — European healthcare costs are broadly comparable to UK private healthcare.

Worldwide excluding USA and Canada: The most popular zone for non-US expats. Covers global treatment except in North America. Excludes the US cost exposure that drives premiums upward.

Worldwide including USA: The comprehensive global option. Includes the US cost structure in the underwriting. Typically 40–60% more expensive than worldwide excluding US for equivalent benefit levels.

Asia Pacific: Some providers offer a specific Asia Pacific zone at pricing between Europe-only and worldwide ex-US — useful for expats based in Southeast Asia, Japan, Australia, or New Zealand.

2026 International Health Insurance Costs

Premiums vary substantially by age, coverage zone, benefit level, and insurer. The following table reflects standard comprehensive coverage (inpatient plus outpatient) with a £1,500 annual deductible.

| Age | Europe Only | Worldwide ex USA | Worldwide inc USA |

|---|---|---|---|

| 25–35 | £820–£1,380 | £1,150–£1,940 | £1,680–£2,830 |

| 36–45 | £1,100–£1,850 | £1,540–£2,590 | £2,250–£3,790 |

| 46–55 | £1,580–£2,660 | £2,210–£3,720 | £3,230–£5,440 |

| 56–65 | £2,290–£3,850 | £3,200–£5,390 | £4,680–£7,880 |

Key Premium Levers

Annual deductible: The excess you pay toward claims before the insurer pays. Increasing from £0 (nil excess) to £1,500 per year typically reduces premiums by 20–30%. Increasing to £5,000 can reduce premiums by 40–50%. Set the deductible at the amount you can absorb from readily accessible savings.

Coverage zone: Moving from worldwide-including-US to worldwide-excluding-US saves 35–50% for most age bands. If you do not need US coverage, excluding it is the most significant single premium lever.

Benefit ceiling: Plans with annual benefit limits (£1m–£2m) cost significantly less than unlimited benefit plans. For most expats, a £2m annual limit is functionally equivalent to unlimited — few legitimate medical events approach this ceiling.

Pre-Existing Conditions in International Health Insurance

International health insurance approaches pre-existing condition underwriting in broadly the same way as UK PMI — but with some important differences in the market structure.

Moratorium Underwriting

The most common approach for individual international health plans. Conditions treated or investigated in the five years before the policy start date are excluded for the first two years of the plan. After two consecutive years symptom-free and treatment-free, the condition may be reviewed for coverage.

Full Medical Underwriting

Provides complete transparency — all exclusions are disclosed before the policy starts. Preferable for expats with complex medical histories who want certainty about their coverage position before living in a country where self-funding unexpected costs is prohibitive.

Corporate Group Plans

Employees on company-arranged international health plans are often covered on a medical history disregarded (MHD) basis — meaning all conditions, including pre-existing ones, are covered from day one without underwriting. This is one of the most significant benefits of employer-arranged international health insurance versus individual plans. Employees moving from a company plan to an individual plan on return should seek CPME (Continued Personal Medical Exclusions) continuity terms to protect conditions covered under the corporate plan.

The Main International Health Insurance Providers

Cigna Global: One of the largest international health insurers globally. Strong network of hospitals and clinics in 160+ countries. Modular product structure with flexible deductible options. Particularly strong in Asia Pacific and the Americas.

AXA Global Healthcare: Comprehensive individual and corporate plans. Strong digital claims management. Wide hospital network. Good maternity coverage terms.

Bupa Global: Well-known brand with strong customer service reputation. Unlimited benefit option available. Strong coverage for serious conditions including cancer. Higher premiums than some competitors at equivalent benefit levels.

Allianz Care: Strong corporate international health plans. Also offers individual expat plans. Competitive pricing for Europe-only and worldwide-excluding-US zones.

Now Health International: Newer entrant with competitive pricing. Strong digital platform for claims management. Particularly competitive for remote workers and digital nomads.

William Russell: Specialist expat insurer with straightforward product structure and competitive pricing. Good customer service for individual policyholders.