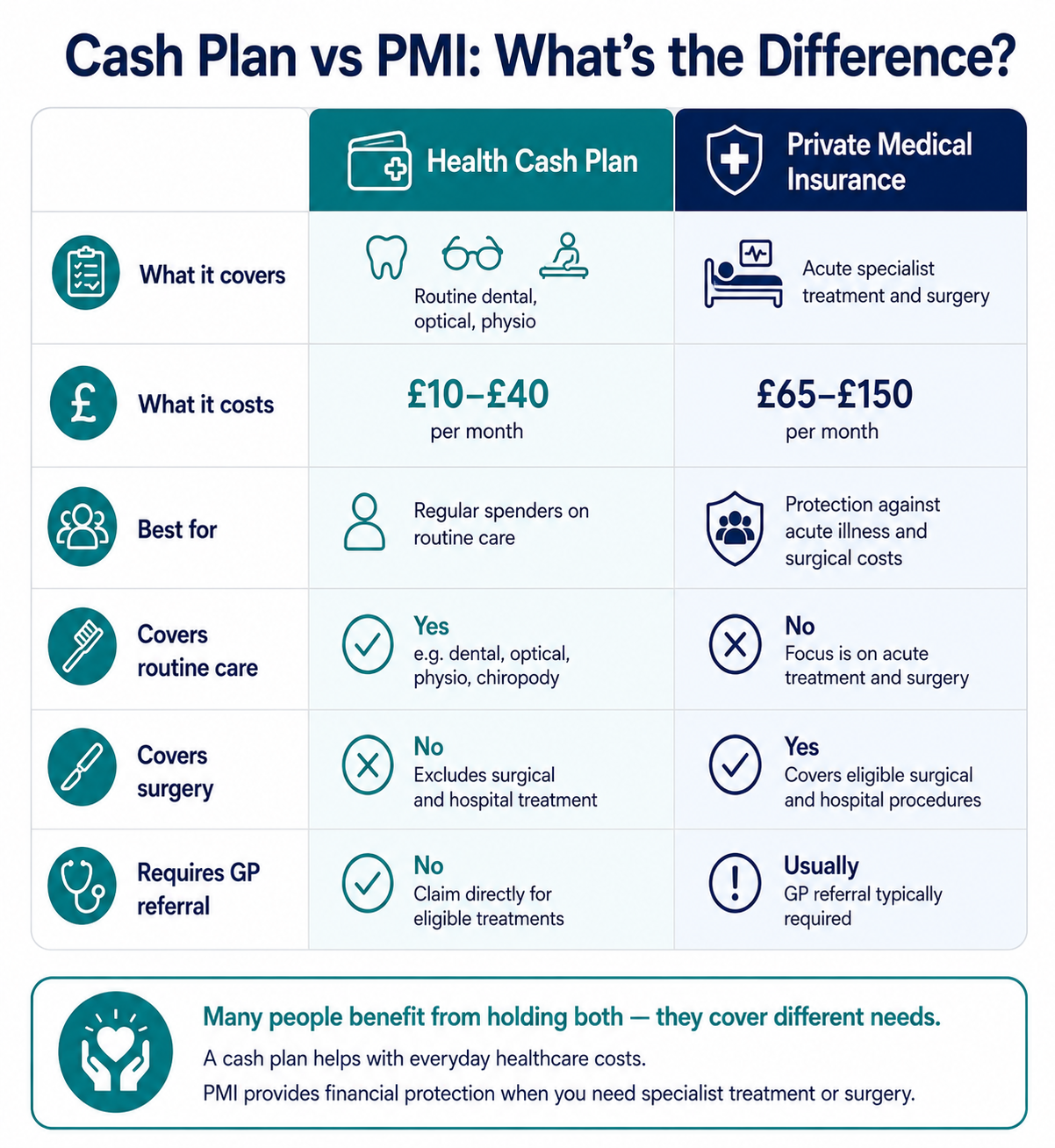

A health cash plan pays a fixed cash benefit when you access eligible healthcare, dental checkups, optical tests, physiotherapy, specialist consultations and hospital stays. It is not the same as private medical insurance, it does not cover surgery or emergency treatment. Cash plans reimburse a defined amount per claim (e.g. £60 toward a dental checkup that costs £85) rather than the full cost. They cost £10–£40 per month and are most valuable for individuals who spend regularly on routine dental, optical and physiotherapy, costs that PMI explicitly excludes.

A health cash plan is a low-cost health benefit product that reimburses defined cash amounts toward the routine healthcare costs, dental, optical, physiotherapy and other everyday treatment, that private medical insurance does not cover, in exchange for a monthly premium.

What a Health Cash Plan Is, and How It Differs From PMI

The term "health insurance" in the UK spans two fundamentally different products that are frequently confused.

Private medical insurance (PMI) covers the cost of private specialist consultations, diagnostics, and surgery for acute conditions. Premiums are £65–£150/month for a standard adult policy. It does not cover routine dental, optical, or physiotherapy, these are explicitly excluded.

Health cash plans reimburse a fixed amount toward the everyday healthcare costs that PMI excludes, dental checkups, eye tests, glasses, physiotherapy, chiropody, complementary therapies, and in some plans specialist consultations and hospital overnight stays. Premiums are £10–£40/month.

The relationship between the two: Some individuals hold both products. PMI covers the acute, surgical, and high-cost risks. A health cash plan covers the routine costs PMI ignores. The combined cost of a standard PMI policy plus a mid-tier cash plan (approximately £85–£130/month total for a 40-year-old) provides broader coverage than either alone.

Others use a cash plan as a standalone product, particularly individuals in good health who want support with routine costs without paying full PMI premiums. For younger, healthy individuals, a cash plan at £15/month may provide more tangible day-to-day value than PMI at £65/month.

How Health Cash Plans Work, the Mechanics

The Claims Process

Cash plans operate on a reimbursement model:

- You receive healthcare treatment (dental checkup, physiotherapy session, eye test)

- You pay the full cost at the point of care

- You submit a claim to the cash plan provider, typically online via an app or portal, with the receipt and treatment details

- The cash plan pays the agreed benefit amount (not necessarily the full cost) into your bank account within 3–5 working days

No pre-authorisation required: Unlike PMI, which requires a GP referral for most claims, cash plans do not need pre-authorisation. You attend any eligible provider and claim afterward.

No network restriction: Cash plans pay the benefit regardless of which provider you attend, you can use any NHS or private dentist, optician, physiotherapist or hospital. The benefit amount is fixed in the policy; the provider's actual charge is not the determining factor.

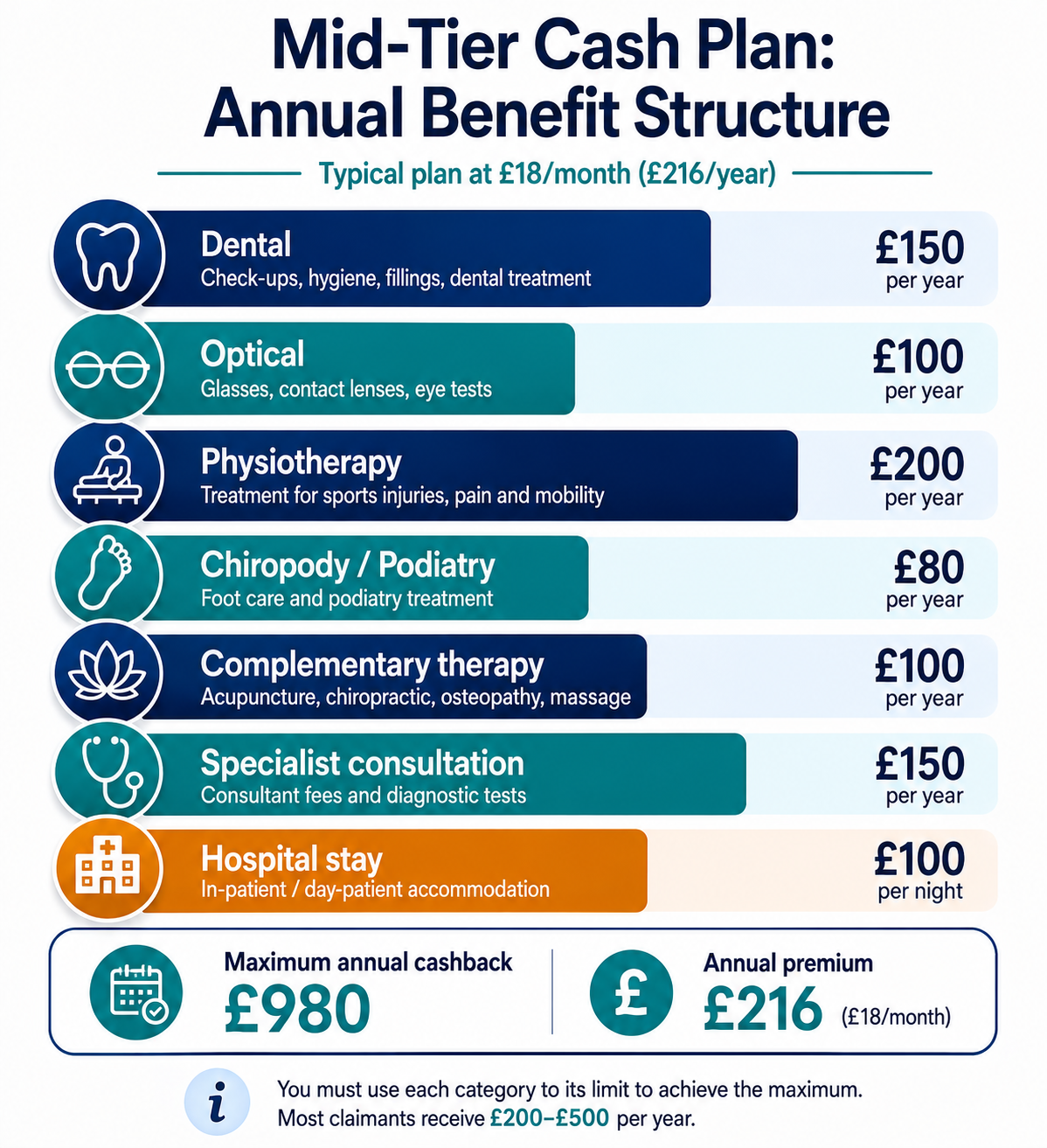

The Annual Limits Structure

Cash plans set annual limits per treatment category. These limits determine the maximum cashback available per policy year, not the cost per individual claim.

| Treatment Category | Annual Limit |

|---|---|

| Dental treatment | £150 |

| Optical (glasses/contact lenses) | £100 |

| Physiotherapy | £200 |

| Chiropody | £80 |

| Complementary therapies | £100 |

| Specialist consultation | £150 |

| Hospital stay (inpatient) | £100 per night, max 10 nights |

| Maternity | £100 |

Total annual cashback available: Approximately £980 per year at the limits above. Annual premium cost: £216. Net maximum benefit: £764, but only if you use each category to its limit, which most policyholders do not.

The realistic annual claim depends on actual healthcare use. A person who visits the dentist twice, has an eye test and new glasses, and has four physiotherapy sessions might realistically claim £320–£450 against a £216 annual premium, a meaningful but modest net benefit.

What Health Cash Plans Cover, Category by Category

Dental

Most cash plans cover NHS and private dental treatment, checkups, x-rays, fillings, extractions, and hygienist appointments. Annual limits typically range from £100 to £500 depending on the plan tier.

The NHS dental cashback element deserves attention: many cash plan holders use the dental benefit to reclaim NHS dental charges (Band 1: £26.80, Band 2: £73.50). Even if you use an NHS dentist, a cash plan can reclaim all or part of your NHS charge, partially offsetting a cost you would have incurred anyway.

Optical

Covers eye tests and the cost of glasses or contact lenses up to the annual limit. Most standard plans offer £80–£150 per year for optical costs. Given that an eye test costs £20–£40 and a pair of single-vision glasses costs £80–£250, this benefit is usable annually for anyone who wears glasses or contact lenses.

Physiotherapy

One of the most valuable cash plan categories for active individuals, those with musculoskeletal conditions, or those recovering from injury. NHS physiotherapy has long waiting lists in most areas; private physiotherapy costs £50–£100 per session. A cash plan covering £200 in physiotherapy per year funds 2–4 private sessions.

Complementary Therapies

Osteopathy, chiropractic, acupuncture, reflexology, and in some policies homeopathy and massage therapy. Annual limits of £80–£200. Coverage of complementary therapies is more variable than core medical categories, check the specific plan's eligible therapy list.

Specialist Consultations

Some mid-tier and comprehensive cash plans include a benefit for private specialist consultations, typically £100–£200 toward a consultation fee. Private specialist consultations cost £150–£350 for an initial appointment. The cash plan benefit reduces but does not eliminate the self-pay cost.

Hospital Cash

An inpatient hospital benefit pays a fixed amount per night during a hospital stay, typically £50–£150 per night up to a maximum of 10–20 nights. This applies to both NHS and private hospital stays. It is not designed to cover treatment costs (PMI or the NHS handles those), it covers the incidental costs of a hospital stay (transport, childcare, lost earnings not covered by employer sick pay).

Health Cash Plans as an Employee Benefit

Health cash plans are widely used as an employer-funded employee benefit, often described as part of a "benefits package" alongside pension contributions and life insurance. They are popular with employers because:

Low cost per employee: Mid-tier group cash plans cost employers £12–£25 per employee per month, significantly cheaper than group PMI (£40–£80/month per employee).

High perceived value: Employees use cash plans regularly, dental, optical, and physiotherapy claims are made by most policyholders annually. This produces high engagement compared to insurance products that many employees never claim on.

Tax treatment: Employer-funded group cash plans are a taxable P11D benefit, the employee pays income tax on the value. However, at £15–£25/month, the tax cost (approximately £3–£5/month for a basic rate taxpayer) is modest relative to the benefit value.

The employer health cash plan market: Major providers include Simplyhealth, Westfield Health, HSF Health Plan, and Bupa Cash Plan. All offer group pricing at lower per-head rates than individual plans, with customisable benefit structures for different employer needs.

2026 Health Cash Plan Costs, Individual Plans

| Plan Tier | Monthly Premium | Key Benefits | Annual Premium |

|---|---|---|---|

| Entry (dental + optical only) | £8–£12 | £100 dental, £80 optical | £96–£144 |

| Standard (core benefits) | £13–£20 | £150 dental, £100 optical, £150 physio | £156–£240 |

| Mid-tier (broad coverage) | £20–£28 | £250 dental, £150 optical, £200 physio, complementary | £240–£336 |

| Comprehensive | £28–£40 | £500 dental, £250 optical, £300 physio, specialist consultations | £336–£480 |

Main UK Providers at a Glance

Simplyhealth: Largest health cash plan provider in the UK. Individual and group plans. Strong digital claims process via app. Wellbeing platform included. Annual limits from £500 to £1,800+ depending on tier.

Westfield Health: Strong in the corporate market. Individual plans also available. Competitive annual limits for physiotherapy and specialist consultations. 24/7 GP access helpline included.

HSF Health Plan: Provides cash plans through employers and directly. Lower premiums at entry level. Strong dental and optical benefits.

Medicash: Corporate and individual plans. Broad therapy coverage. Employee Assistance Programme (EAP) included.

Healthshield: Specialist corporate cash plan provider. Highly customisable benefit structures for employer requirements.