Dental insurance pays for private dental treatment — checkups, fillings, extractions, crowns, and in some policies root canal treatment and orthodontics. It is not the same as NHS dental care, which uses a fixed Band 1/2/3 charge structure. NHS England reported in 2023 that 40% of UK adults had been unable to access NHS dental care when they needed it. Dental insurance costs £8–£40 per month and typically breaks even if you need one checkup and one treatment per year at private rates. It is most valuable for individuals who require regular dental treatment or who live in areas with severe NHS dentist shortages.

Dental insurance UK is a health protection product that reimburses a proportion of the cost of private dental treatment — preventive care, restorative work and, on comprehensive tiers, complex procedures — up to defined annual limits, in exchange for a monthly premium.

The NHS Dental Crisis — Why Dental Insurance Has Become More Relevant

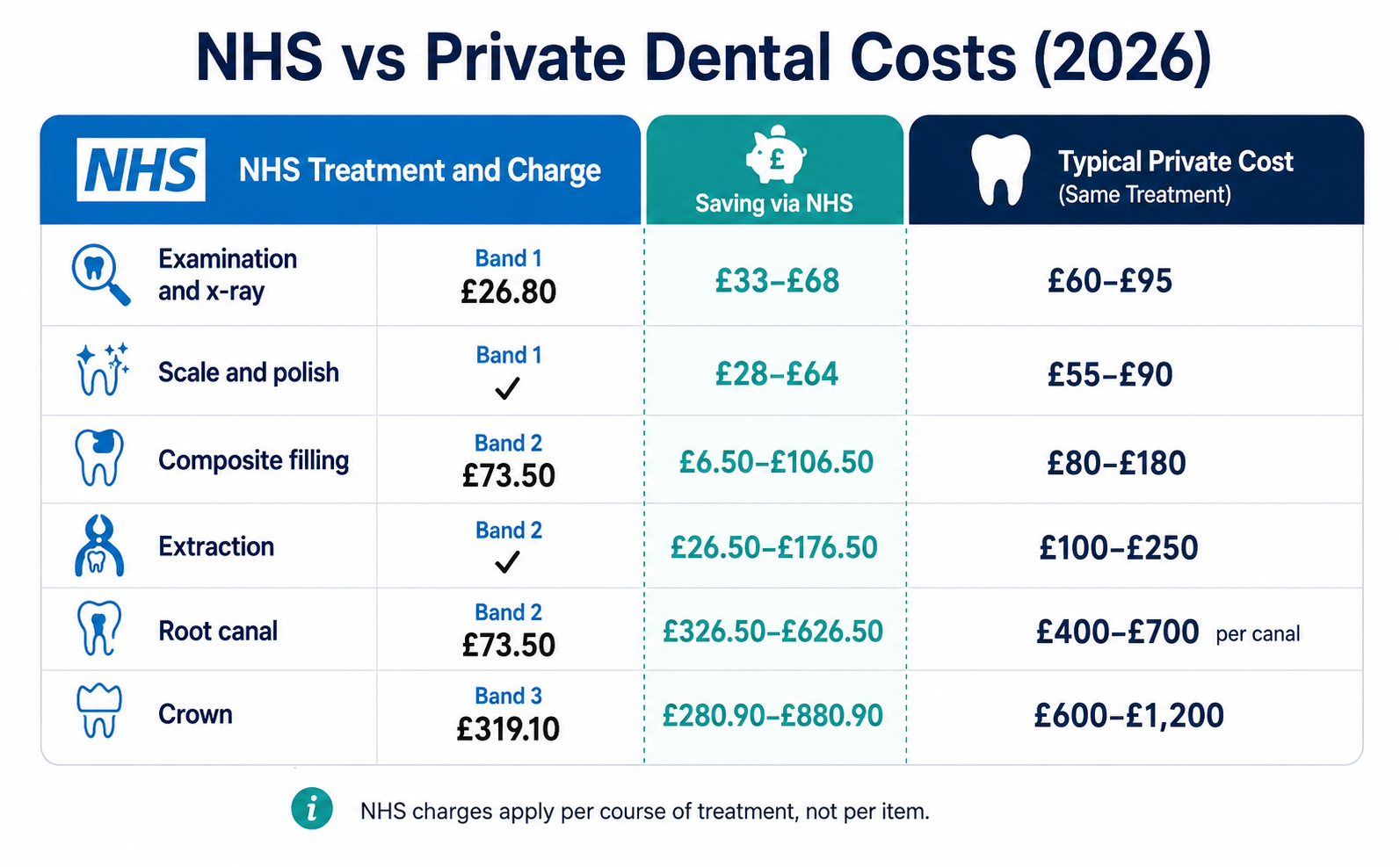

NHS dental care in the UK operates on a Band charge system that charges patients fixed amounts regardless of the complexity or cost of treatment:

| Band | 2026 NHS Charge | What It Covers |

|---|---|---|

| Band 1 | £26.80 | Examination, diagnosis, x-rays, scale and polish |

| Band 2 | £73.50 | All Band 1 treatments plus fillings, extractions, root canal treatment |

| Band 3 | £319.10 | All Band 1 and 2 treatments plus crowns, dentures, bridges |

The NHS charge system makes NHS dental care substantially cheaper than private for most treatments. An NHS crown (Band 3) costs £319.10. The same crown privately costs £600–£1,200.

The access problem: The critical issue is not cost — it is availability. NHS England's 2023 survey found that 40% of adults reported being unable to access NHS dental care when they needed it. In some areas — rural England, coastal towns, parts of the Midlands and North West — NHS dentist availability has deteriorated to the point where patients are travelling 30–50 miles or waiting 18+ months for an NHS appointment.

In this environment, dental insurance is not primarily about cost — it is about access. Private dental practices have shorter appointment waiting times, more appointment slots, and continuity of care with a named dentist.

Two Types of UK Dental Product — the Distinction Most Buyers Miss

Before comparing dental insurance products, understand that two fundamentally different products are sold under the "dental insurance" umbrella.

Dental Insurance (Indemnity Model)

Pays a proportion of the actual cost of each treatment up to defined annual limits. You pay the treatment cost and the insurer reimburses you — either 100% or a defined percentage.

Example: A filling costs £120 at your private dentist. Your policy covers 80% of fillings up to an annual limit of £600. The insurer pays £96. You pay £24.

Key feature: You can use any dental practice — not restricted to a network.

Annual limits matter: Most dental insurance policies impose annual limits per treatment category (e.g. £250 for checkups, £500 for routine treatment, £1,500 for major treatment such as crowns). Once the annual limit is reached, you pay the full cost of further treatment in that category until the policy year resets.

Dental Plans / Capitation Plans (Denplan Model)

A different structure entirely. You register with a specific dentist who has joined the plan network. A monthly fee covers preventive care (regular checkups, hygienist appointments) and provides a discount on treatment. The dentist assesses your mouth and sets your monthly fee based on the level of care they anticipate you will need.

The dominant provider: Denplan (now part of Simplyhealth) is the largest UK dental plan with over 6,000 participating dentists and 1.6 million patients. Monthly fees range from £12 to £50+ depending on dental health status at assessment, geographic area, and dentist pricing.

Key distinction: Denplan is a patient-dentist contract — the dentist provides care. Dental insurance is an insurer-patient contract — the insurer reimburses costs. Both are described as "dental insurance" but they work very differently.

What Dental Insurance Covers — and the Exclusions That Limit Its Value

Typically Covered

Routine / preventive care: Dental examinations, x-rays, scale and polish, and hygienist appointments. These are the treatments most people use annually regardless of dental health status.

Restorative treatment: Fillings (amalgam and composite), extractions, and inlays. The most commonly claimed treatment category after checkups.

Complex restorative treatment: Root canal treatment, crowns, and bridges. Typically covered under comprehensive dental insurance policies at higher annual limits. Most budget policies cap complex treatment at £500–£1,000 per year.

Emergency dental treatment: Most policies cover emergency treatment when away from home or when your usual dentist is unavailable — pain relief, temporary dressings, emergency extractions.

Typically Excluded

Pre-existing dental conditions: Any treatment required for a condition present at the time the policy starts. A tooth that needs a crown before the policy inception will not have that crown covered. Most policies include a waiting period of 2–6 months during which treatment costs are not covered.

Cosmetic dental procedures: Teeth whitening, veneers, cosmetic bonding, and aesthetic reshaping are excluded from all standard dental insurance policies. Cosmetic dental work has no clinical indication and is categorically excluded.

Dental implants: The majority of standard dental insurance policies exclude implants entirely or apply such low annual limits (£500–£1,000) that they cover only a small proportion of implant costs (typically £2,000–£4,000 per tooth). If implant cover is a priority, specialist dental insurance with specific implant coverage is required — at significantly higher premiums.

Orthodontics for adults: Most dental insurance policies exclude adult orthodontics (braces, aligners) or apply strict limits. Children's orthodontics may be covered under family policies at defined limits.

2026 Dental Insurance Cost — What You Pay vs What You Get

Individual Dental Insurance — Monthly Premium Ranges

| Coverage Level | Monthly Premium | Annual Checkup Limit | Annual Treatment Limit | Major Treatment Limit |

|---|---|---|---|---|

| Budget (checkups + basic treatment) | £8–£14 | £100–£150 | £250–£400 | Not covered |

| Standard (routine + restorative) | £14–£22 | £150–£250 | £400–£700 | £500–£800 |

| Comprehensive (includes complex work) | £22–£38 | £200–£350 | £600–£1,000 | £1,000–£2,000 |

| Premium (near-full private cover) | £38–£55 | £300+ | £1,000+ | £2,000+ |

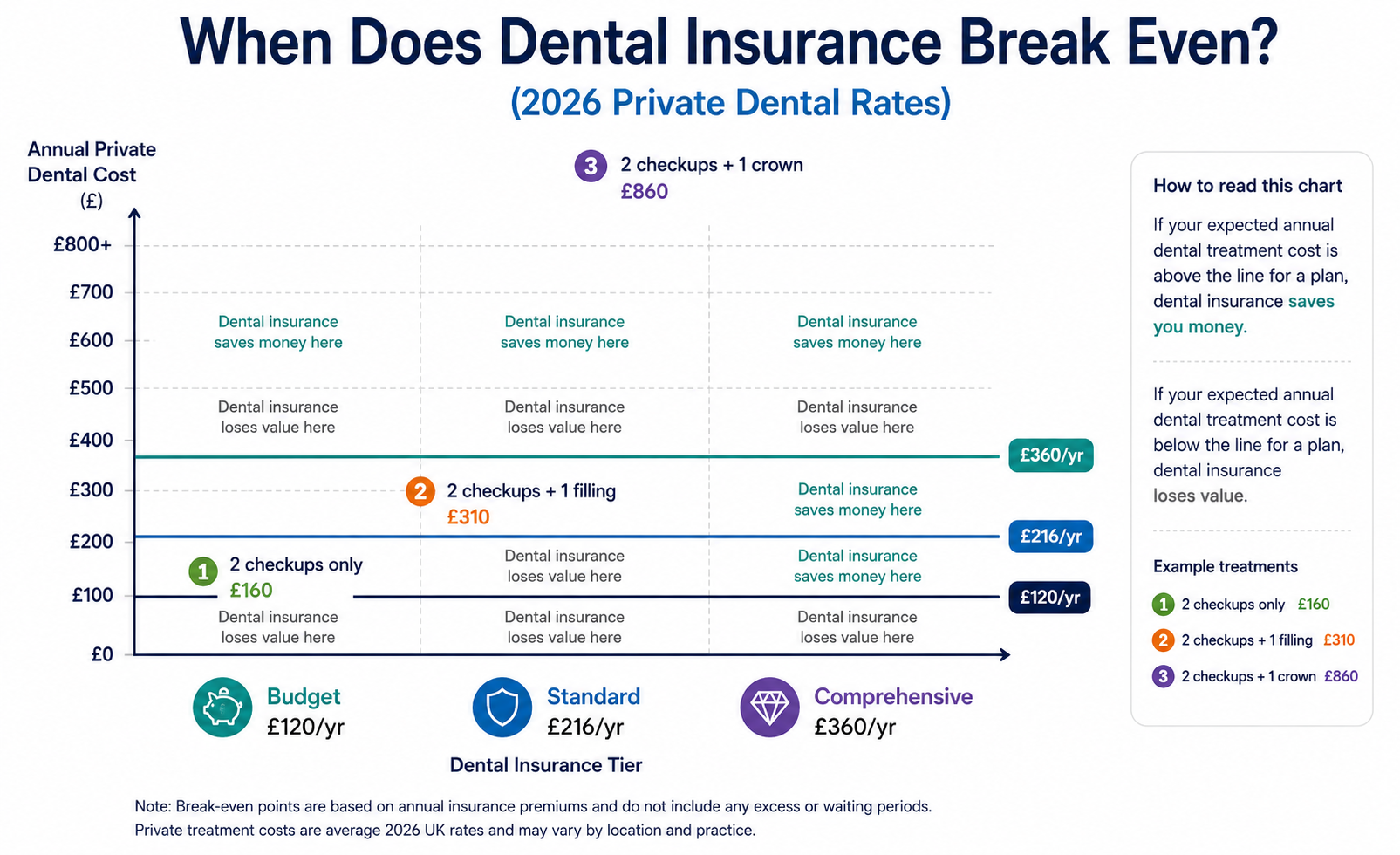

The Break-Even Calculation

The practical question for every buyer: does the cost of dental insurance exceed the cost of the dental treatment you are likely to need?

At standard tier (£18/month, £216/year): If you attend two checkups per year (NHS Band 1: £26.80 × 2 = £53.60, or private checkup: £60–£100 × 2 = £120–£200) and one filling per year (private filling: £80–£180), the uninsured private cost is approximately £200–£380. Dental insurance at £216/year covers this with modest margin — the break-even is approximately one checkup and one treatment per year at private rates.

The value increases when:

- You require crowns, root canal, or bridges (private: £600–£1,200 per crown)

- You have children on a family policy (children's dental costs add to the household total)

- Your access to NHS dental care is effectively zero (the private costs replace the NHS Band structure entirely)

The value is limited when:

- You are in good dental health requiring only biennial checkups

- You have access to an NHS dentist and choose to use it for routine care

- You have significant pre-existing dental needs that the waiting period excludes

The Main UK Dental Insurance Providers — What Each Offers

Denplan (Simplyhealth): Largest capitation plan. Registered dentist model. Monthly fee from £12–£50+ depending on dental health assessment. Covers routine care and provides 24/7 dental helpline and emergency treatment worldwide. 6,000+ participating dentists.

Bupa Dental Insurance: Indemnity model. No network restriction. Annual limits from £1,000–£5,000 depending on tier. Waiting period applies for complex treatment. Strong brand recognition and claims handling.

Simplyhealth Dental: Both cash plan and full dental insurance products. Cash plan pays fixed amounts per treatment; insurance product covers a percentage of actual costs. Flexible product range at competitive premiums.

AXA Dental: Indemnity model. Covers routine, restorative, and major treatment with graduated annual limits. Competitive premiums for standard tiers.

Dencover: Specialist dental insurer with strong major treatment limits. Covers implants under some tiers — one of few providers to do so. Higher premium reflects broader coverage scope.

CIGNA Dental: Often available as a workplace benefit. Flexible network options and strong clinical governance.